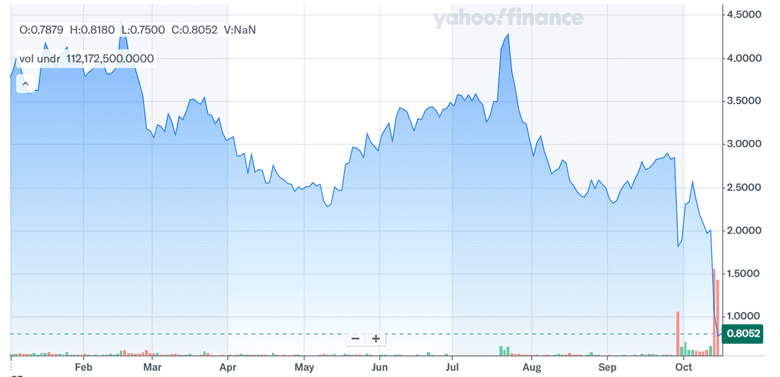

Remember when Beyond Meat (NASDAQ: BYND) was the toast of Wall Street? Those days are long gone. On October 14, 2025, the stock dipped below $1 for the first time ever, touching an intraday low of $0.85—down a jaw-dropping 99% from its peak above $230. Let that sink in. Once the poster child of food tech disruption, Beyond Meat is now a cautionary tale in what happens when hype, debt, and dilution collide. This year alone, the stock is down 77%. The latest chapter? A controversial debt-for-equity swap that shaved $800 million off the books—but ballooned the share count by over 400%. That’s right. More shares, less value. Add to that collapsing sales, mounting losses, and a plant-based meat category that’s fast losing its sizzle, and you’ve got a company in freefall. TD Cowen recently slapped a $0.80 price target on the stock and stuck with a “Sell” rating. Here’s a breakdown of how things unraveled so fast.

Massive Share Dilution & Equity Value Destruction

Let’s start with the elephant in the (refrigerated) aisle: the dilution bomb. Beyond Meat’s latest debt swap may have relieved some pressure—exchanging $202.5 million in new 2030 notes for older 2027 ones—but it came at a brutal cost. In return, the company handed over up to 326 million new shares, taking the total count from 77 million to over 400 million. That’s a 400% dilution—an almost unheard-of number for a small-cap company. Technically, this sliced Beyond’s debt by 83%. Practically, it wiped out shareholder equity. Investors ran for the exits, and who could blame them? The company’s Price/Sales ratio is now just 0.22x, while the P/E sits at a dismal -0.52x. Essentially, the market has decided Beyond Meat’s equity is worth close to nothing. While the deal buys some breathing room, it also resets the cap table in a way that permanently alters ownership—and expectations. Yes, the debt is lighter. But the damage to shareholder trust? That’s going to take a lot longer to fix.

Persistent Profitability & Cash Flow Weakness

Even before this dilution fiasco, Beyond Meat was leaking cash like a sieve. In the first half of 2025, the company burned through $59.4 million in operating cash—worse than the $47.8 million outflow a year prior. Adjusted EBITDA in Q2? A loss of $26 million, or negative 34.7% of revenue. Operating costs? Still stuck at $47.4 million despite restructuring efforts. It’s a grim financial picture: LTM EV/EBITDA at -9.19x, levered free cash flow yield at -148%, and a Market Cap/Free Cash Flow multiple of just 0.68x. Translation: this business continues to consume capital without any clear line to profit. Sure, they’ve brought on a Chief Transformation Officer and are cutting costs. But the math still doesn’t work. Turning EBITDA-positive by late 2026 would require a magical mix of margin expansion and revenue growth—both of which look wildly optimistic right now. There’s just not enough operational leverage in the system to swing from red to black without a major turnaround in volumes, pricing, and consumer appetite.

Structural Demand Decline In Plant-Based Meat

Beyond Meat’s biggest problem might not even be financial—it’s cultural. People just aren’t buying plant-based meat like they used to. Q2 revenues were down nearly 20% year-over-year. U.S. retail sales fell 26.7%, international foodservice dropped 25.8%, and overall volume slipped 18.9%. This isn’t just a blip—it’s a trend. The price gap with real meat remains too wide. Consumers are drifting back to beef, chicken, and even premium cuts. And let’s face it—processed plant patties don’t have the cool factor they did back in 2019. Beyond’s attempts to revamp—like rebranding products, simplifying ingredients, and experimenting with frozen aisle distribution—have yielded little so far. In-store visibility is down. Shelf space is shrinking. And while Beyond Chicken and Steak have earned decent reviews, they haven’t sparked a revival. The flexitarian wave that lifted all boats early on? It's receding. And Beyond, without a blockbuster innovation or clear brand revival plan, is stuck trying to paddle against the tide.

Temporary Debt Relief, But No Strategic Turnaround

The October debt deal gave Beyond a temporary win—maturities are pushed to 2030 and $800 million in principal is off the books. But here’s the rub: this isn’t a turnaround strategy, it’s a delay tactic. The company still holds over $1.2 billion in debt, and only $117 million in cash. That’s not a comfy cushion, especially when your revenue is in freefall. Gross margins dropped to 11.5% in Q2, down from 14.7% the year before. Operational efficiency remains elusive, and even with AlixPartners’ John Boken stepping in as interim Chief Transformation Officer, there’s no clear roadmap to profitable growth. Beyond is trying—slashing SKUs, streamlining supply chains, tightening marketing spend—but none of it moves the needle fast enough. And meanwhile, confidence is eroding. Without a compelling narrative to reignite demand or reassure investors, the company’s stock has entered penny-stock territory. The brand still has recognition, but at this point, it feels like Beyond Meat is a turnaround story in search of a turnaround.

Final Thoughts

Source: Yahoo Finance

Beyond Meat’s collapse below $1 per share marks a dramatic fall from grace for a company once hailed as the future of food innovation. The small-cap’s trailing valuation multiples—LTM EV/Revenue of 4.05x and LTM EV/Gross Profit of 38.34x—are difficult to justify amid shrinking revenue and negative EBITDA. Price/Sales ratios have fallen to just 0.20x, reflecting deep investor skepticism. This looks more like a case study in what happens when big vision meets bad execution. The company shed a huge chunk of debt, yes. But the cost—massive dilution, shrinking demand, and broken investor trust—has been steep. Financially, the picture is bleak: negative earnings, negative cash flow, and valuation multiples that are tough to justify unless you believe in a full-blown comeback. For a small-cap stock that was once a market darling, this is a sobering reversal. Can Beyond turn it around? Maybe. But they’ll need more than clever SKUs and margin trimming to win back the market’s trust. For now, it’s a stark reminder: growth stories are great—until they aren’t.