[ad_1]

Tetraphase Pharmaceuticals (NASDAQ:TTPH) just lately grew to become a business stage biotech firm. We ought to see the primary income from business gross sales when This fall 2018 outcomes are reported, most probably in February 2019.

Despite a little bit of restoration on the finish of the week, the market as a complete, biotechnology, and small-cap biotechs specifically have been in a droop. That has been amplified for small cap biotechs. I see that as a discount basement, the place a discerning eye can choose up long term winners at very low cost costs proper now. There are many corporations on this class.

Tetraphase acquired FDA approval for Xerava for classy intra-belly infections, or cIAI, in late August 2018. It acquired European approval in September. Xerava is a broad-spectrum, intravenous therapy for antibiotic-resistant micro organism.

Xerava (Eravacycline) molecular construction

Post approval, Tetraphase stock has dropped from a excessive of $6.90 in January 2018 to $1.13 on the shut on December 31. That represents a market capitalization of simply $61 million.

The case towards Tetraphase

Since Xerava, a subsequent-era antibiotic, was authorised in Q3 and will have started producing income in This fall, in a traditional market, we’d assume that the low worth of Tetraphase is as a result of gross sales are anticipated (by market individuals) to be minimal. A $61 million market cap, utilizing a rule-of-thumb P/E ratio of 20, would wish solely about $3 million in annual earnings to justify it.

Tetraphase had a Q4 expense of near $20 million. Treating that as a run price, annual bills in 2019 might be round $80 million. Xerava income would have to be about $83 million in 2019 to lead to $3 million in earnings.

Is the market sending a sign that Xerava will generate $83 million or much less in income in 2019?

It often takes new drug income time to ramp. Doctors and hospitals that deal with cIAI have to be educated about some great benefits of utilizing Xerava as a substitute of the present commonplace of care. A greater marker could be income expectations for This fall 2019. Indeed, market capitalizations for biotechs usually are primarily based on earnings expectations years additional sooner or later.

I feel the true caveat for potential Tetraphase traders is how thinly it and different small cap biotechs are traded. Despite its small market cap, a poor This fall displaying may ship the stock even decrease.

The case for Tetraphase

I wouldn’t have an impartial evaluation of how a lot Xerava bought in This fall 2018 or will promote in 2019 or past. However, Tetraphase administration has finished their analysis. Slide 4 from the November corporate presentation summarizes their view:

The important issue is the “Significant Market Opportunity” beneath the present label of 2 million affected person days of remedy per 12 months. Combine that with the estimated $175 per day wholesale value talked about within the Q3 analyst conference, and the annual income run price could be $350 million.

I’d anticipate that bills would additionally improve considerably if that run price might be achieved. (Chosen for roundness of numbers) if bills elevated to $150 million, that may be $200 million per 12 months in earnings. Justifying a $4 billion market cap. Or $74.63 per share if the share depend stays the identical. That could be a really-finest-case state of affairs with Xerava as the one supply of business income.

The worst-case state of affairs is that Xerava won’t promote sufficient to cowl bills, and the pipeline will fail, and the stock will finally fall to $0.00 per share.

What is an inexpensive quantity, to me? I’d be more than happy if, after ramping in 2019, Xerava captured 50% of its projected addressable market in 2020, or $175 million. Using (my guesswork) bills of $125 million for that state of affairs, annual earnings could be $50 million, giving a market capitalization estimate of $1.0 billion. With present share depend, that may lead to shares at $18.65.

There shouldn’t be essentially a correlation between the velocity of ramp and the market saturation level. A speedy ramp would encourage traders, however the extra necessary concern is the accuracy of the market alternative estimate.

Cash runway

Tetraphase had about $97 million in money with no debt on the finish of Q3. In November, it borrowed $30 million, and its facility has one other $45 million obtainable. That would take the runway effectively into 2020 and longer if business income ramps shortly sufficient.

What to search for

The subsequent quantity to come back out will probably be This fall income, together with This fall Xerava income. We are prone to get that in February. I’ve low expectations for the launch. There are nonetheless possible insurance coverage reimbursement points and physician studying curves. If $1 million or extra is available in, I’ll contemplate the product launched. I’ll wish to hear any nuance about how administration presents expectations for additional ramping. If there are usually not a minimum of 1,000 daily doses bought, or $175 thousand in income, I’d wish to know why.

By the tip of Q2, I’d fear if Xerava has not achieved $5 million in income, which is about quarter-method to the tough break-even level of $20 million per quarter.

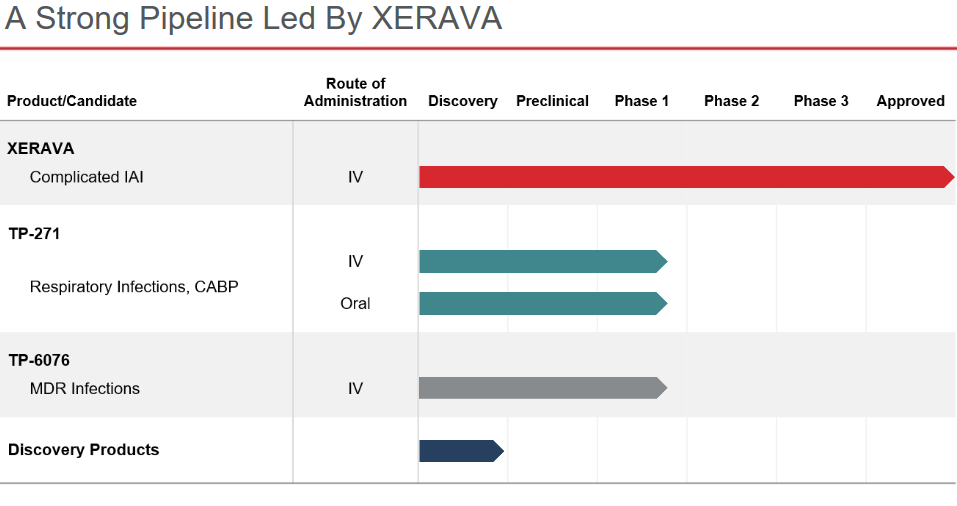

The growth of the pipeline may additionally impression the worth of Tetraphase over time. The emergence of latest antibiotic resistant illnesses, whether or not or not Xerava works for them, may be influential.

Here is the pipeline slide:

Conclusion

I feel on the present value Tetraphase is an excellent wager with little or no threat. The threat could be primarily from a potential additional meltdown of the market usually or biotech specifically.

I feel $3.00 per share is an effective value goal for now. That would correspond to a market capitalization of simply $161 million. It could be far decrease than the excessive achieved in 2018. How shortly we get there may be possible depending on each investor sentiment within the biotech sector and on precise Xerava gross sales studies.

Disclosure: I’m/we’re lengthy TTPH. I wrote this text myself, and it expresses my very own opinions. I’m not receiving compensation for it (aside from from Seeking Alpha). I’ve no enterprise relationship with any firm whose stock is talked about on this article.

Additional disclosure: When writing this text TTPH represented 1.4% of my portfolio.

[ad_2]