Cantaloupe Inc. (NASDAQ:CTLP), a small-cap play within the self-service commerce and unattended retail solutions domain, recently found itself in the regulatory spotlight after receiving a second request for information from the Federal Trade Commission (FTC) regarding its proposed $848 million acquisition by 365 Retail Markets. Initially announced in June 2025, the all-cash transaction, priced at $11.20 per share, was expected to close in the second half of the year. However, this latest FTC development has raised questions about deal timing and scrutiny, causing Cantaloupe’s stock to dip. Despite the regulatory hurdle, the strategic logic behind the deal remains intact. For 365 Retail Markets—a private equity-backed player in unattended retail—Cantaloupe offers a complementary and scalable platform with strong product momentum, a growing international footprint, and significant traction in SMB and enterprise channels. But is that all there is to the deal? Let us find out!

Robust Recurring Revenue Engine With High Margin Mix

Cantaloupe has engineered a strong foundation of recurring revenue through its subscription and transaction segments, which collectively grew 10% year-over-year in Q3 FY2025, reaching $65.2 million. Subscriptions alone contributed $21.2 million, supported by a 90.7% gross margin, while transaction services brought in $44 million at a 24.8% margin, both showing steady improvement. These high-margin, recurring streams now represent the bulk of Cantaloupe’s revenue, providing predictability and resilience—qualities that are critical in a rising rate and volatile macro environment. Furthermore, ARPU (average revenue per unit) increased 11% year-over-year to $206, reflecting better monetization per device. For 365 Retail Markets, acquiring a small-cap company with a mature software-led revenue engine opens up opportunities for further operational leverage. Given the high overlap in end-markets, integrating Cantaloupe’s subscription platforms such as Seed Analytics and Remote Price Change modules can drive immediate cost and revenue synergies. With adjusted EBITDA margin already improving—up 37% YoY to $13.9 million in Q3—Cantaloupe demonstrates scalability and margin upside potential that fits well with private equity value-creation strategies. Moreover, the strategic release of a $42.2 million deferred tax valuation allowance indicates long-term earnings confidence, which further reinforces the durability of the business model.

Smart Store Momentum Unlocks Next-Gen Retail Format Synergies

Cantaloupe’s most compelling growth narrative lies in its Smart Store platform, which addresses critical pain points in unattended retail—namely theft prevention, modern consumer experience, and SKU flexibility. In Q3 FY2025, Smart Store sales topped $2 million, with management noting it as the “hottest selling product” and highlighting strong visibility for Q4 demand. Unlike legacy vending machines and micro markets, Smart Stores are theft-resistant, high-capacity, and support items like fresh salads and sandwiches—unlocking new verticals such as airports, residential buildings, and sports venues. This aligns perfectly with 365 Retail Markets’ broader push into unattended convenience, offering synergy in form factor innovation, shared channel distribution, and customer expansion. Ravi Venkatesan, Cantaloupe’s CEO, explicitly noted the product’s outsized revenue potential—estimating Smart Stores could account for 25% to 30% of all new deployments within 12–18 months. Given that 365 Retail has focused on self-checkout and kiosk technologies, adding Smart Stores allows it to accelerate into higher-margin, high-growth areas with minimal R&D investment. The ability to cross-sell Smart Store infrastructure into 365’s base, and vice versa, supports rapid post-deal scale. This is particularly attractive in a segment that management expects to grow 100–200% annually, compared to 5–6% for traditional vending. Ultimately, this product-led synergy underpins the acquisition’s strategic value proposition.

Strategic Penetration Across SMB & Enterprise Channels

Cantaloupe has developed a dual-channel go-to-market strategy that spans small-to-mid-sized businesses (SMBs) as well as enterprise customers, creating a balanced customer base of over 34,000 active clients and 1.26 million active devices as of March 2025. The SMB channel continues to exhibit robust expansion, with recent wins such as ACE Vending, Variety Vendors, and Best Vending—many of whom adopted full-stack solutions including Seed software and cashless devices. Meanwhile, on the enterprise side, clients like DC Vending are replacing over 1,200 devices and adopting Cantaloupe’s analytics and remote pricing modules—signaling competitive displacement and strong product-market fit. This wide market aperture offers 365 Retail Markets a ready-made channel ecosystem that complements its existing footprint and customer relationships. Notably, Cantaloupe has invested in channel partnerships with AVS, CPI, and CandyMachines.com, allowing downstream scale without significant sales force expansion. The ecosystem includes amusement, transportation, education, and sports verticals, creating room for upsell and wallet-share growth. This diversified reach mitigates sector concentration risks and enhances cross-platform integration potential. A strategic buyer can tap into both segments simultaneously and apply differentiated bundling, pricing, or vertical-focused go-to-market motions. From a valuation perspective, this level of customer diversity helps justify premium acquisition multiples when compared to narrow-focused SaaS players in the small-cap retail automation sector.

Improving Cash Flow Profile & International Scalability

Despite its small-cap status, Cantaloupe is now a net cash generator, with $22.4 million in cash from operations in Q3 FY2025 and free cash flow of $18.6 million, representing a meaningful sequential improvement. With year-end cash balances reaching $46.3 million, the company has established financial flexibility without incurring leverage—an attractive trait for a buyer seeking a bolt-on that won't strain capital deployment. Importantly, the company released its long-standing deferred tax asset valuation allowance in Q3, adding $42.2 million in non-recurring tax benefits and signaling confidence in sustained GAAP profitability. On the geographic front, Cantaloupe’s international expansion strategy—particularly in Europe and Latin America—is underway, with management signaling imminent announcements. While still small (3–4% of revenues), these regions offer leverageable opportunities for 365 Retail, particularly given their existing international presence. Moreover, with the newly launched Cantaloupe Capital, offering equipment financing through Fundbox, Cantaloupe has built adjacent financial infrastructure that can unlock capex cycles, drive customer stickiness, and potentially boost average order sizes. For a private equity-backed buyer, such self-funded growth enablers make the company a capital-efficient bet in a sector where hardware-linked SaaS models often require external funding for growth. These factors collectively support both vertical and horizontal scalability in the hands of a well-capitalized acquirer.

Final Thoughts

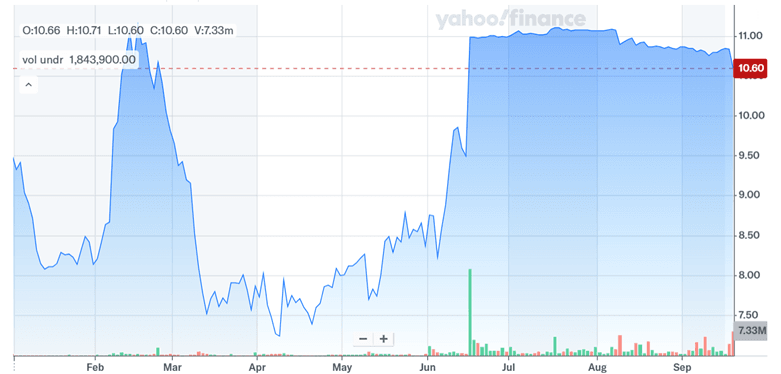

Source: Yahoo Finance

From a synergy perspective,

Cantaloupe’s trajectory has been more or less flat over the past 3-4 months and its LTM valuation multiples—2.57x EV/Sales, 18.90x EV/EBITDA, and 33.32x EV/EBIT—are elevated relative to small-cap peers. These indicate premium expectations that may not account for cyclical risks in vending hardware, regulatory delays, and international execution complexities. The second FTC request adds further uncertainty to deal timing and approval odds. While the strategic fit is evident, valuation discipline and regulatory navigation will likely determine whether 365 Retail Markets proceeds or pulls back. For now, Cantaloupe remains a credible and synergistic acquisition target—but not without its share of dealmaking friction.