[ad_1]

2018 is shortly coming to an in depth. For these of us concerned within the Chinese market, this cannot come quick sufficient! That being stated, the tough yr has offered some engaging shopping for alternatives and beneath are only a few that I’m considering.

iQiyi (IQ)

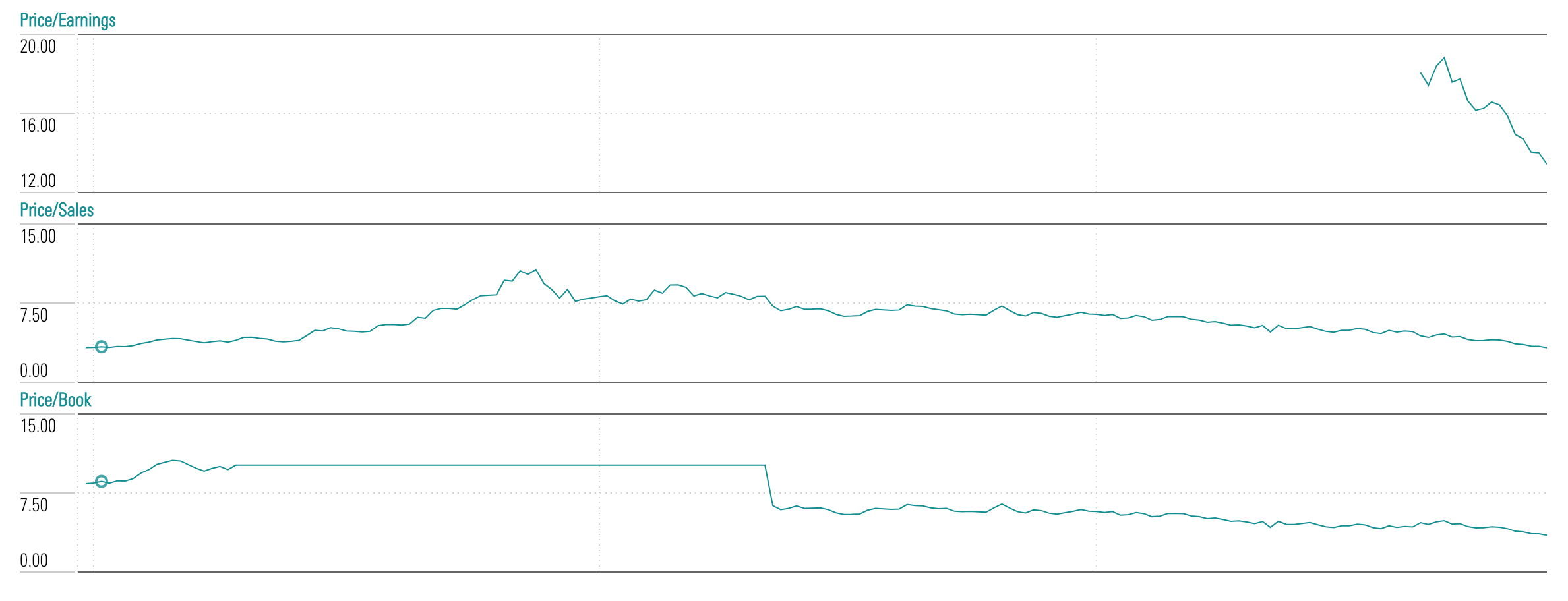

iQiyi had a powerful run after its IPO earlier this yr. After hitting markets at $18, the stock reached greater than $40 lower than 4 months later. However, the stock has been on the decline ever since and now sits at $15 per ADR.

Just as a result of the stock has declined doesn’t by itself imply that the stock is now low cost. However, wanting nearer we see that the stock is definitely at its most cost-effective degree based mostly on valuation ratios. The present P/E sits round 13x however P/S (which I concentrate on extra for progress) is lower than 5x.

Source: Morningstar

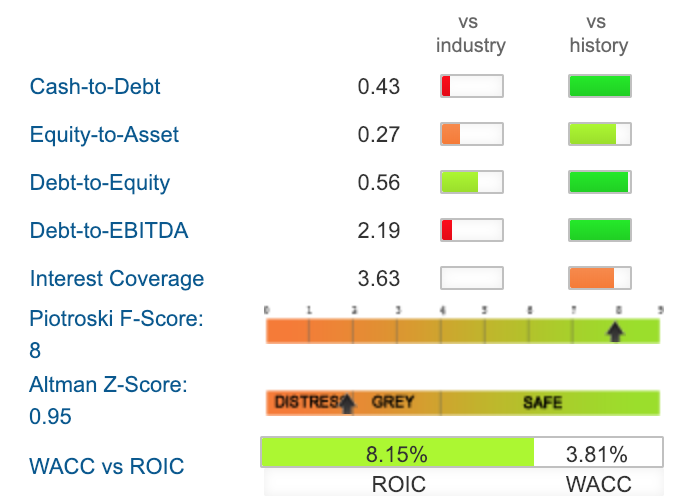

The firm is anticipated to proceed to increase and develop within the foreseeable future. Revenue is projected to just about attain $6 billion year-end of 2020 however profitability will nonetheless be out of attain. iQiyi is the market share chief with 37% and is investing closely into authentic content material, it is a confirmed mannequin due to Netflix (NFLX).

Source: GuruFocus

Alibaba (BABA)

BABA stock has had a tough second half of 2018 however the enterprise itself has remained robust. The stock has continued to be punished because the US-China commerce battle has escalated. There can be issues over the slowing of the Chinese economic system however Alibaba is diversified, each in segments and international locations.

Most not too long ago Single’s Day broke information once more, persevering with the occasions multi-year streak. This yr complete GMV surpassed 2017 GMV with simply over 8 hours remaining. Revenues for the occasion had been slightly below $31 billion, up 24% from 2017 (the bottom progress within the occasions historical past).

Source: Twitter

The stock has been punished as of late due to issues over the financial slowdown occurring inside China. This is warranted within the short-term as the corporate posted its lowest progress for Single’s Day and reduce income forecasts for the following yr. That being stated, the corporate is pushing robust into the cloud enterprise which is younger and rising throughout the nation. Along with that is the expansion of the middle-class which can proceed to spice up gross sales within the long-term as extra Chinese residents enter this socioeconomic class. There can be an aggressive plan to undertake rising applied sciences equivalent to voice and AI, coupled with the emergence of bodily areas.

Margins have been compressed currently however that’s principally due to elevated funding exercise. There can be strain from the diversification of the enterprise into higher-cost segments such because the cloud enterprise which requires heavy infrastructure prices in comparison with Alibaba’s standard asset-light mannequin. That being stated, FCF continues to develop and money/debt nonetheless sits at about 1.3x.

China Southern Airlines (ZNH)

Airlines are a gorgeous guess for China’s future. Travel is rising due to the rise within the middle-class together with bettering infrastructure. ZNH is down greater than 50% since March and this dip has been seen earlier than. Over the previous three- to 4 years, the stock has appeared to stay above the $25 degree and financials have grown since.

The firm has been investing closely into its fleet with the acquisition of recent planes bringing the common age of the fleet to 6.9 years, one of many youngest within the business. What attracts me is the advance in financials. Even although their has been hefty funding into new planes, debt ratios are at a few of their greatest ranges. ROIC is greater than 2x WACC indicating robust efficiency and use of capital. Couple this with a P/S of 0.3x, a PEG of 0.6, and a P/FE of 8x and ZNH is value a glance.

Source: GuruFocus

Conclusion

These are only a few of the shares which can be on my potential record. Given the current turmoil we’ve got seen in Chinese equities and the present geopolitical/economics standing of the nation, it’s not a shock that some could also be considerably undervalued based mostly on long-term potential. Even although there may be financial slowing, there are nonetheless segments throughout the economic system which can be rising due to general progress in revenue and the middle-class.

Once we see commerce battle tensions ease there ought to be a rally in costs. Given that China is slowly overtaking world operations (fueled by their growth into Africa) there may be extra potential than most would care to confess. As at all times, the overhanging concern is the need of the federal government. For instance, earlier within the yr we noticed video video games stall as the federal government withheld titles publication, solely to renew throughout the final week. Overall, there may be sufficient potential to warrant the danger, however there may be danger.

If you have an interest in China and need to be taught extra concerning the economic system and the alternatives inside, give Corporate China a shot. Subscribers acquire entry to:

- Reviews of financial stories

- In-depth firm evaluation

- Price targets and the fashions used

- Daily information headlines and the way they have an effect on the market

This is an thrilling time to be monitoring the Chinese economic system. Geopolitical occasions such because the on-going commerce battle and a slowing economic system are creating a troublesome surroundings stuffed with emotion. I type by the emotion to seek out the chance. If you have an interest, start at this time with a free trial!

Disclosure: I’m/we’re lengthy IQ, BABA, ZNH. I wrote this text myself, and it expresses my very own opinions. I’m not receiving compensation for it (apart from from Seeking Alpha). I’ve no enterprise relationship with any firm whose stock is talked about on this article.

[ad_2]