Deere & Co (NYSE:DE), once known purely as a manufacturer of tractors and farm equipment, has reinvented itself as a global leader in AI-enabled precision agriculture. In a span of just five years, the company has pivoted from its traditional hardware-centric model to a technology-first approach, embedding artificial intelligence, machine learning, and cloud connectivity into its machinery and services. While farm incomes in the U.S. have declined from record highs, Deere has continued to deliver strong operating margins, driven by its growing tech-enabled revenue streams, rising adoption of subscription services, and expanding footprint in emerging agricultural powerhouses like Brazil. However, with tariffs mounting and equipment valuations already high, the road ahead demands careful execution. Let us dive deeper to try and explain Deere’s leadership in smart agriculture and what it is doing to stay ahead.

Precision Ag & Subscription-Based Business Models

Deere’s most significant evolution has been its transition into precision agriculture, anchored by its digital platform—the John Deere Operations Center. This cloud-based hub now connects more than 475 million acres globally, allowing farmers to monitor, manage, and optimize their equipment and field operations in real time. On top of this, Deere has layered a suite of digital tools, including GPS-based guidance, real-time diagnostics, and autonomous controls. These tools are increasingly being offered under subscription-based models, such as the Precision Essentials package and the G5 license suite. In fiscal 2025 alone, Deere recorded nearly 10,000 Precision Essentials orders globally, surpassing the prior year’s volume in just six months. Additionally, usage-based pricing has been introduced for technologies like See & Spray, where farmers pay based on herbicide savings achieved through AI-powered spot spraying. While these services add recurring revenue streams and strengthen customer loyalty, they also bring new operational challenges. Deere must ensure high renewal rates, seamless connectivity (especially in underdeveloped regions), and continuous tech support through its dealer network to maintain momentum. The success of these services will ultimately shape how Deere navigates the shift from hardware sales to long-term software-driven relationships.

Brazil: Deere’s Strategic Growth Engine

As global demand for food and biofuels rises, Deere has found its most promising growth market in Brazil—a country poised to lead the next phase of agricultural expansion. Brazil is already the world’s top exporter of soybeans, sugar, and cotton, and it ranks second in corn. What sets the region apart is its ability to produce multiple crops annually through double-cropping systems, particularly in the Cerrado region. Deere has spent the last 25 years building an integrated presence in Brazil, with eight manufacturing facilities, a sprawling dealership network of over 275 outlets, and a newly inaugurated R&D center in Indaiatuba. These local operations allow Deere to customize products for Brazil’s tropical conditions and large-scale operations. The company is also introducing connectivity solutions like JDLink Boost—satellite-based services that bring real-time data to remote farms. Deere has already sold more than 4,000 JDLink Boost units in Brazil this year. As part of its longer-term goals, Deere plans to grow its connected machines in the region by 2.5 times and expand engaged acres by 50% by 2030. Yet, Brazil isn’t without risks. High interest rates and commodity price fluctuations could restrain equipment purchases in the short term, and expanding crop acreage may face environmental regulatory scrutiny. Still, Brazil provides Deere with a key hedge against cyclical slowdowns in North America and opens the door to rapid technology adoption in a high-growth market.

U.S. Manufacturing & Cross-Segment Tech Integration

Another core strength of Deere’s strategy is its vertically integrated manufacturing model, anchored in the United States. Approximately 80% of Deere’s U.S. sales are fulfilled by domestically produced machinery, with more than 75% of components sourced from within the country. This footprint has become even more strategic as global trade becomes more volatile and customers place a premium on supply chain resilience. Deere has committed over $20 billion in U.S. capital investment over the next decade to bolster its advanced manufacturing capabilities and new product development. This investment supports the deployment of AI-enabled technologies like autonomous tillage and ExactShot planters. Additionally, Deere is extending its digital tech stack beyond agriculture. At the 2025 Bauma construction trade show in Munich, Deere showcased roadbuilding machinery equipped with the same Operations Center platform used in farming. The ability to scale technology across segments like construction, forestry, and commercial mowing creates economies of scale, enhances capital efficiency, and opens up new revenue streams. However, this integration also increases the company’s exposure to global tariffs—particularly for its roadbuilding and construction segments—which are expected to cut into fiscal 2025 earnings by over $500 million. Deere’s mitigation plans include sourcing diversification and reshoring select production lines, but execution risks remain.

Navigating Tariff Pressures & Inventory Challenges

Despite facing considerable macroeconomic headwinds, Deere delivered an 18.8% margin in its equipment operations for Q2 FY2025. Still, the company is bracing for the impact of more than $500 million in full-year tariff-related costs, primarily affecting its Construction & Forestry and Small Ag segments. Deere is countering these challenges through supply chain reconfiguration, pricing flexibility in early-order programs, and selective sourcing from USMCA countries. At the same time, Deere is managing through a glut of late-model used equipment in North America, especially in high-horsepower tractors. The company has made progress: new inventories for large tractors are down 40% year-over-year, while combine inventories are down nearly 25%. Used combine inventories are also normalizing thanks to dealer-led resale and financing strategies. On the demand side, stabilization in crop prices and lower global grain inventories suggest that commodity fundamentals may support a gradual recovery. However, subdued consumer confidence and elevated interest rates are dampening turf equipment and compact tractor sales. These dynamics are likely to weigh on earnings in the second half of the year, especially as Deere’s premium equipment valuation could limit pricing flexibility. Nonetheless, Deere’s product breadth, regional diversification, and long-term technology investments offer a level of structural resilience that most industrial peers cannot match.

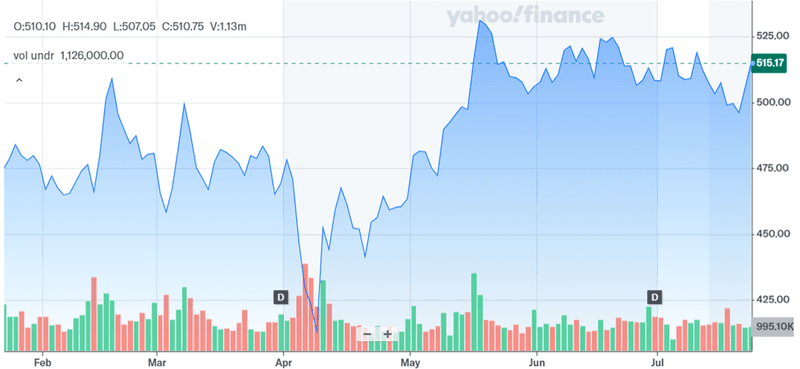

Conclusion: A Solid Transformation But A Pricey Stock?

Source: Yahoo Finance

Deere’s evolution into a digitally integrated agriculture company has given it an edge in an industry on the cusp of transformation. However, this strategic positioning now comes with a steep valuation as shown in the above chart. Over the past 12 months, Deere’s key forward and trailing multiples have expanded significantly. Its forward P/E has risen from 16.49x in July 2024 to 25.91x as of July 23, 2025, while the forward EV/EBIT multiple surged from 20.55x to 30.94x. Even trailing figures reflect this shift: LTM EV/EBIT has climbed from 13.83x to 27.23x, and LTM P/E has nearly doubled from 11.61x to 24.92x. These valuation expansions have far outpaced revenue and earnings growth, driven largely by investor enthusiasm around Deere’s AI-enabled technologies and its dominance in Brazil. While this premium may be justified by Deere’s long-term growth prospects and operational resilience, it also leaves little margin for error. Elevated valuations in a cyclical business—especially one exposed to tariffs, interest rate sensitivity, and fluctuating commodity prices—could compress quickly if the farm cycle does not turn favorably. Hence, we believe that Deere’s stock, despite its solid positioning, may be a bit too pricey for the average, risk-averse investor.