Denny’s Corporation (NASDAQ: DENN), the iconic American diner chain, is now the subject of private equity interest as a consortium led by TriArtisan Capital Advisors has announced a deal to take the company private at a $620 million valuation, including debt. This acquisition group includes TriArtisan—already a known player in the restaurant space with holdings in TGI Fridays and P.F. Chang’s—alongside Treville Capital and Yadav Enterprises, one of Denny’s largest franchisees. The transaction terms offer Denny’s shareholders $6.25 per share in cash, a premium of 52% over its closing price the day before the announcement. While this development represents a major turning point for the small-cap restaurant chain, it also reflects the culmination of various strategic, financial, and operational trends. Let us dive deeper and try to identify the reasons that could explain why TriArtisan Capital Advisors sees value in acquiring Denny’s and what strategic synergies could emerge from this potential deal.

Strong Off-Premise Growth & Digital Loyalty Rollout Could Scale With Synergistic Investment

Denny’s has increasingly leaned into off-premise dining—now comprising 21% of total sales—and that strategy is paying off. The company has invested heavily in digital channels, which helped boost conversion rates and engagement on both proprietary and third-party platforms. These initiatives contributed a 1.5% uplift in same-restaurant sales during Q2 2025, even as dine-in performance remained volatile. The upcoming launch of a points-based loyalty program, designed to collect first-party data and drive personalized marketing, adds a compelling digital layer to the brand’s evolving strategy. This CRM platform is expected to boost traffic by 50 to 100 basis points over time, and guests in the digital loyalty funnel tend to visit 2x more frequently. For a private equity player like TriArtisan, which already has restaurant brands in its portfolio, these digital and off-premise capabilities can be replicated across other chains to reduce customer acquisition costs and enhance average check sizes. The integration of Denny’s scalable digital infrastructure into a larger restaurant platform would allow for shared technology investments, coordinated promotional campaigns, and unified customer data strategies—helping accelerate returns across the portfolio. Additionally, cross-brand promotions or bundled loyalty programs could emerge, leveraging TriArtisan’s existing restaurants like TGI Fridays and P.F. Chang’s, creating a network effect in a sector that increasingly values omnichannel engagement.

Operational Rehabilitation & Portfolio Rationalization Provides Expansion Blueprint

Denny’s has been executing a targeted strategy of operational improvement by closing underperforming stores, refranchising selectively, and rehabilitating struggling restaurants through focused training and oversight. This initiative—launched in 2023 and expected to complete by end-2025—has already generated visible financial improvements. Franchise Average Unit Volumes (AUVs) rose by approximately 5%, or nearly $100,000, indicating healthier unit economics across the portfolio. Quintile 5 (lowest-performing) restaurants, once the drag on system-wide performance, now outperform franchise average same-store sales by 120 basis points thanks to intensified support. The company is also identifying up to 200 basis points in margin improvement through smart sourcing, waste reduction, and recipe enhancements. For TriArtisan, a platform investor with a playbook in restaurant operations, this signals an opportunity to apply similar cost optimization and rehabilitation strategies across its existing brands or new additions. Moreover, the disciplined asset-light refranchising strategy, such as recent sales of Keke’s cafes in Northern Florida, aligns with private equity goals of minimizing capital intensity. The groundwork laid by Denny’s management in right-sizing its footprint can now be scaled, accelerated, and monetized under TriArtisan’s ownership—either through future refinancing events or eventual portfolio exits.

Strong Brand Equity & Value Positioning In A Defensive Category

Denny’s remains one of the most recognizable names in the American family dining segment. Even in a “choppy consumer environment,” the brand has managed to outperform key category benchmarks in core markets like California for six consecutive quarters. The company’s focus on value-centric promotions—like the buy-one-get-one Slam for $1 and “4 Slams Under $10”—have resonated with its core demographic in the $50,000–$70,000 income bracket, driving both new and returning traffic. These limited-time offerings and revamped value menus are engineered to be margin-accretive while sustaining guest frequency. In addition, Denny’s brand has proven resilience during inflationary periods due to its affordability positioning, making it a relatively defensive asset during downturns. TriArtisan’s acquisition could unlock more brand value by exploring brand extensions (e.g., frozen meals, merchandise), global franchising (particularly in emerging markets), and loyalty ecosystems. This would enable the firm to monetize Denny’s legacy while steering its evolution into a modern, multi-channel foodservice provider. The steady demand for budget-friendly dining, paired with Denny’s historical consistency, makes it an attractive bolt-on for a private equity firm seeking a low-risk yield with brand resilience.

Potential Synergies With TriArtisan’s Restaurant Portfolio Through Shared Infrastructure

TriArtisan Capital Advisors already owns established restaurant chains like TGI Fridays and P.F. Chang’s, both of which operate in overlapping dayparts and share comparable operational models with Denny’s. An acquisition offers the potential to streamline back-office functions, consolidate supply chain operations, and harmonize technology stacks across its restaurant brands. For instance, procurement synergies—particularly in proteins, beverages, and packaging—could be extracted through volume discounts, improving margin leverage. There’s also scope to unify labor training systems, food safety protocols, and IT infrastructure, reducing overhead duplication. Denny’s server tablet adoption and digital order channel learnings could be shared across the TriArtisan restaurant ecosystem. Beyond operations, marketing efficiencies can be realized through shared media buying, social media strategy, and even cross-brand loyalty incentives. TriArtisan could also explore cross-utilization of real estate, with Denny’s locations serving as pilot hubs for new concepts or virtual brands. There’s precedent for such synergies; Denny’s itself piloted a Nathan’s Famous virtual hotdog brand in over 70% of company-owned locations, improving sales by 50 basis points. With a centralized private ownership structure, TriArtisan gains the ability to optimize for long-term strategy rather than quarterly earnings optics. This strategic flexibility allows for experimentation and redeployment of best practices across the entire restaurant portfolio, enhancing long-term enterprise value.

Final Thoughts

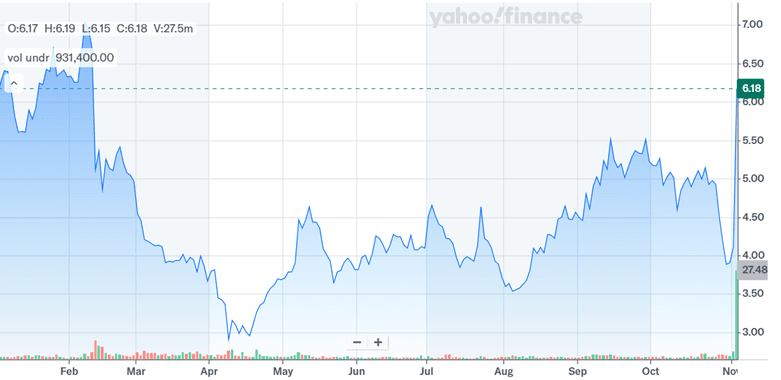

Source: Yahoo Finance

As we can see in the above chart, Denny’s stock price zoomed close to the $6.25 acquisition price levels and is hardly 7 cents shy of those levels today. From a valuation standpoint, it has been acquired at roughly 12.48x LTM EV/EBITDA and 17.60x EV/EBIT, which places it at the upper end of small-cap dining peer averages. While forward multiples (such as 9.26x NTM EV/EBITDA and 15.90x P/E) suggest modest upside, execution risks remain. It is important to note that the casual dining sector continues to face macroeconomic headwinds and intensifying competition from fast casual formats. Despite operational improvements, Denny’s same-store sales have remained negative in recent quarters, and core markets such as Los Angeles and Phoenix have shown softness. Ultimately, the $620 million bid signals confidence in Denny’s long-term viability and potential for turnaround within a structured, private ownership model. Whether TriArtisan can translate its acquisition thesis into meaningful returns remains to be seen.