General Motors (NYSE:GM) is taking an aggressive, multi-front approach to its electric vehicle future, combining tactical short-term measures with long-term transformational bets. The automaker is importing lithium-iron-phosphate battery packs from China’s CATL—despite steep tariffs—to bridge supply gaps for its next-gen Chevrolet Bolt arriving in 2026, while deepening its partnership with Hyundai to co-develop hybrid and EV models for global markets. At the same time, GM is fast-tracking U.S.-based cell production through its Ultium Cells ventures with LG Energy Solution and expanding software-driven services like Super Cruise and OnStar to boost differentiation. A $4 billion expansion in U.S. assembly capacity aims to add 300,000 flexible ICE/EV units by 2026, while nationwide high-speed charging networks are being rolled out to support adoption. This blend of alliances, supply chain maneuvers, product innovation, and infrastructure investment forms the backbone of GM’s EV strategy—anchored by the following key growth drivers shaping its path forward.

Coalition Catalysts

GM’s electrification blueprint hinges on a tapestry of alliances that accelerate innovation, share costs, and broaden market reach. Its August 2025 agreement to import LFP battery modules from CATL—despite triggering an estimated 80 percent tariff—reflects a willingness to incur short-term costs for long-term gain, leveraging LFP’s roughly 35 percent lower production expense versus nickel-cobalt chemistries. This two-year stopgap supplies the next-gen Bolt EV until GM and LG Energy Solution’s Ultium Cells joint ventures in Tennessee and Indiana ramp U.S.-made LFP and advanced lithium-manganese-rich cells in 2027. Simultaneously, GM’s renewed partnership with Hyundai encompasses co-development of five vehicles—an all-electric commercial van and four ICE/hybrid SUVs and pickups for Latin America—targeting combined annual sales north of 800,000 units by 2028. This collaboration optimizes common vehicle architectures, shared R&D, and platform economies to keep unit costs in check while penetrating price-sensitive markets where entry-level models start near $13,000. Beyond batteries and vehicles, GM has inked partnerships with charging-network operators and recycling firms—bringing 350-kW and 400-kW fast chargers to key corridors and repurposing second-life modules through Redwood Materials. Collectively, these strategic collaborations forge a resilient ecosystem that positions GM to flex capacity, control costs, and deliver diverse EV offerings across segments and geographies.

Procurement Power Play

To mitigate tariff exposure and secure a cost-efficient, vertically integrated supply chain, GM is executing a broad domestic expansion and supplier optimization strategy. In July 2025, GM announced a $4 billion investment to augment U.S. assembly capacity by 300,000 high-margin pickup, SUV, and crossover units—enabling flexible shifts between ICE and EV output across Fairfax (Kansas), Spring Hill (Tennessee), and Orion (Michigan). This footprint growth is designed to alleviate a projected $4–5 billion annual tariff headwind by late 2026, following the 80 percent duties that contributed to a $1.1 billion Q2 drag. On the cell-production front, Ultium Cells’ Indiana plant nears completion of prismatic-cell lines while the Spring Hill facility will add LFP in late 2027 alongside high-nickel pouch and novel LMR chemistries—each qualifying for federal advanced-manufacturing tax credits. GM’s procurement teams are onshoring critical battery and semiconductor components, intensifying supplier quality programs to address warranty trends, and deepening partnerships with materials providers to secure lithium, nickel, and cobalt at scale. Concurrently, GM Energy has deployed nearly 200 350-kW chargers on I-75 and other regional corridors, with IONNA’s 400-kW stations live in seven states—preparing for over 65,000 fast-charging bays by year-end and 100,000 by 2027. By knitting together plant investments, cell JV expansions, supplier consolidation, and charging infrastructure, GM aims to reduce unit costs, improve margins, and deliver a seamless EV ownership experience.

Roadmap Revamp

GM’s refreshed product lineup balances mass-market affordability with premium differentiation and cutting-edge software. In Q2 2025, GM ranked #2 in U.S. EV sales with over 46,000 units—driven by the Blazer EV and Equinox EV, which deliver competitive range, performance, and pricing in the mid-SUV segment. At the luxury apex, Cadillac’s Escalade IQ and LYRIQ have propelled conquest rates above 75 percent, cementing Cadillac as the #5 EV brand and the luxury segment leader. Going beyond hardware, GM is embedding Super Cruise across 23 models with more than 600,000 paid subscribers, and bundling OnStar services into vehicle pricing to drive record deferred software revenue of $4 billion. The forthcoming rollout of over 80 new OTA update functions aims to slash infotainment-related warranty spend by 25 percent year-over-year. Looking ahead, GM’s R&D pipeline features lighter, more aerodynamic platforms enabling smaller-battery packaging, standardized electric motors for scale, and applied AI for predictive diagnostics and personalized customer experiences. The company’s bold lineup—from an all-electric commercial van to the GMC Hummer EV super-truck—underscores its ambition to serve every market niche while harnessing scale and brand credibility to underpin profitable EV growth.

Pitfalls and Prospects

Despite its ambitious EV agenda, GM faces execution and market risks that could temper returns. Tariff negotiations with Canada, Mexico, and Korea could lower the projected $4–5 billion annual duty burden, but any delay or partial rollback risks prolonging cost drag. The two-year CATL battery stopgap exposes GM to margin volatility should raw-material costs or tariff levels spike. On the demand side, U.S. EV sales dipped 6 percent in Q2 2025 and the $7,500 federal tax credit expires on September 1, potentially dampening affordability for entry-level models. Yet GM’s diversified approach—integrating hybrids, ICE, and EVs—provides hedges against uneven regional adoption curves. Technology integration presents both upside and risk: Super Cruise and OnStar promise recurring revenues but hinge on consumer acceptance and regulatory approval, while OTA updates can reduce warranties yet demand robust cybersecurity. Supply-chain investments in LMR and LFP cells hold cost-cutting promise but depend on JV execution and material availability. Financially, GM’s trailing LTM multiples remain conservative—0.90× EV/Revenue, 16.20× EV/EBIT, and 8.49× P/E as of August 7, 2025—reflecting investor caution amid cyclical auto demand and EV execution uncertainty. These valuations imply upside if GM meets its production and profitability milestones, but also highlight the market’s skepticism around shifting consumer preferences and policy headwinds.

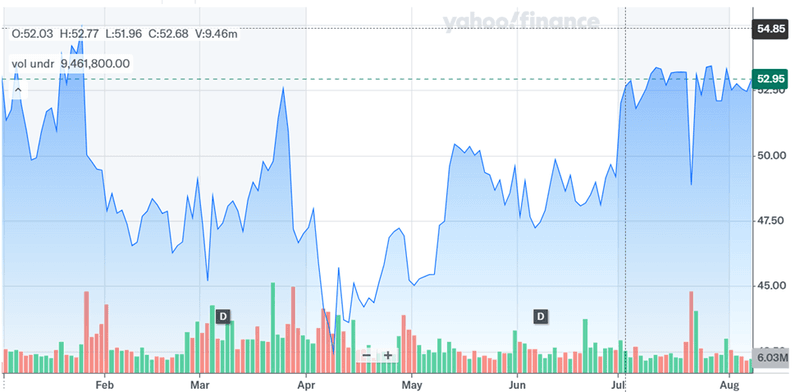

Final Thoughts

Source: Yahoo Finance

GM’s stock price has been extremely volatile in the past few months and the company is trading at modest LTM multiples (0.90× EV/Revenue; 16.20× EV/EBIT; 8.49× P/E). It is evident that the market is pricing in both the execution challenges and the potential for GM’s diversified roadmap to yield sustainable profitability. GM’s new electrification strategy marries tactical stopgaps—like CATL battery imports and tariff-hedging capacity shifts—with transformative investments in domestic cell plants, software services, and flexible manufacturing. Its revitalized EV portfolio spans affordable crossovers to premium luxury trucks, augmented by Super Cruise autonomy and OnStar connectivity. Yet execution complexity, tariff volatility, and evolving EV adoption trends pose material risks to margin improvement. We believe that as GM calibrates its scale, cost structure, and technology stack, its ability to deliver on these interlocking initiatives will determine whether it can convert ambition into enduring shareholder value.