Intel (NASDAQ:INTC), once the undisputed titan of the semiconductor industry, now finds itself at the crossroads of policy, geopolitics, and national security. In August 2025, after weeks of scrutiny over CEO Lip-Bu Tan’s alleged ties to China, the Trump administration reversed its stance. A private meeting at the White House led to public support for Tan and the initiation of talks about a potential U.S. government equity stake. The stock jumped over 7%—its best weekly gain in two decades. Within days, Japan’s SoftBank Group Corp. announced a surprise $2 billion investment at $23 per share. That dual validation—domestic and international—has repositioned Intel as more than just a struggling chipmaker. These developments reflect a strategic pivot: from reactive subsidies to direct ownership aimed at anchoring the U.S.'s semiconductor sovereignty. But what is the rationale? And what lies ahead for Intel?

A National Imperative: Intel As America's Last Advanced Foundry

Intel’s true strategic value lies in its fabrication capabilities. With Taiwan’s TSMC and South Korea’s Samsung dominating advanced-node manufacturing, the U.S. faces a national security risk from over-reliance on foreign foundries. Intel remains the only U.S.-based firm pursuing 18A and 14A process technologies domestically. These nodes are critical for defense, AI inference, and next-generation cloud compute. Under CEO Lip-Bu Tan, Intel has halted large-scale expansions in Europe and refocused capital toward Arizona and Southeast Asia. Its Arizona fab already produces wafers for the Panther Lake platform and collaborates with government agencies on secure test chips, IP libraries, and packaging development kits (PDKs). The U.S. Department of Defense and intelligence community are expected to leverage Intel’s secure packaging and enclave manufacturing for mission-critical applications. Equity ownership would grant Washington direct oversight of capacity planning and strategic alignment, reducing exposure to geopolitical disruptions. Compared to one-time grants under the CHIPS Act, equity would embed public interest into Intel’s long-term strategy—aligning the company with sovereign manufacturing goals and signaling a global commitment to onshore resilience.

Strategic AI Compute & Full-Stack Integration

While Nvidia leads in AI training and AMD in high-performance compute, Intel brings holistic integration to the table. As one of the few firms capable of delivering silicon-to-software solutions, Intel’s roadmap spans AI-optimized CPUs (Panther Lake, Nova Lake), data center accelerators (Xeon 6, Gaudi 3), and supporting frameworks like oneAPI and OpenVINO. These tools position Intel well for AI inference, which is gaining importance in edge computing, federal systems, and secure enterprise deployments. With agentic AI expanding across defense, healthcare, and energy, there is increasing demand for localized, secure compute environments—Intel’s sweet spot. Government equity would enable prioritization of Intel hardware in public sector AI builds, while also incentivizing investment in next-gen areas like silicon photonics and secure memory architectures. SoftBank’s $2 billion stake underscores Intel’s strategic value globally, especially as Japan aligns with U.S. chip policy. The infusion provides not just capital but credibility, expanding Intel’s geopolitical network at a time when AI sovereignty has become a strategic imperative for both nations.

Political Power & Industrial Policy Signaling

A direct U.S. stake in Intel would mark a significant shift in how Washington engages with private industry. The past two years have seen the federal government move from subsidy provider to strategic shareholder—negotiating revenue-sharing with Nvidia and AMD, enforcing national security clauses in foreign acquisitions, and redefining the CHIPS Act into a policy instrument. Intel is uniquely suited to this model. Though it retains relevance, it has clearly lost leadership and suffers execution challenges. A stake allows the administration to secure governance rights, influence R&D prioritization, and embed national interest within corporate planning. Politically, it addresses criticism from hawks like Senators Tom Cotton and Bernie Moreno, who question Intel’s leadership and strategic discipline. SoftBank’s parallel investment amplifies the signaling effect. Founder Masayoshi Son’s acknowledgment of Intel’s 50-year legacy frames the company as a linchpin in the AI future. While some critics argue the deal may have political overtones, its real impact lies in linking Tokyo’s industrial policy with Washington’s strategic tech goals—making Intel a bilateral anchor in the West’s semiconductor strategy.

Execution Risk & Financial Fragility

Despite its strategic importance, Intel’s operating performance remains troubled. In Q2 2025, Intel reported a $2.9 billion net loss and negative adjusted free cash flow of $1.1 billion. Fab utilization rates are below target, pressuring margins already hit by cost absorption and packaging inefficiencies. Intel Foundry Services posted a $3.2 billion loss, raising doubts about its competitiveness in a market dominated by TSMC. Gains in PC and select server revenue have failed to translate into operating leverage. Valuation metrics reflect market skepticism: Intel trades at 15.37x LTM TEV/EBITDA, 1.97x Price/Sales, and a negative P/E of -5.04x. Forward estimates show little relief, with P/E above 100x and free cash flow yield at -6.9%. This profile typically deters private capital. Yet Intel is not an ordinary firm—it is a systemic asset. Without intervention, capital constraints may derail its turnaround before benefits from 18A nodes or foundry traction materialize. SoftBank’s equity injection and possible U.S. government stake provide runway, but operational fixes—cost discipline, execution, and customer trust—remain essential. Strategic capital may buy time, but sustainable value depends on operational delivery.

Final Thoughts

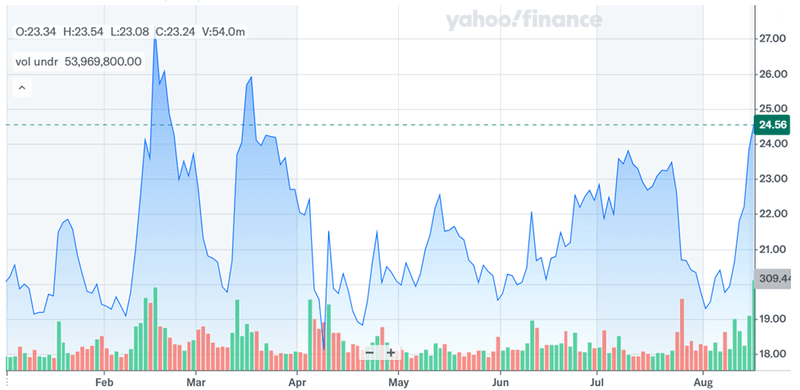

Source: Yahoo Finance

Intel’s stock price has been extremely volatile in the past few months, reflecting the general uncertainty around the company. The Trump administration’s evolving posture—from condemnation to collaboration—signals a recognition that Intel’s role in AI, defense, and chip sovereignty cannot be replicated. At the same time, LTM metrics—15.37x TEV/EBITDA, 1.97x Price/Sales, and a negative P/E—underscore deep-rooted inefficiencies and margin risks. SoftBank’s $2 billion investment adds credibility but also heightens expectations. A U.S. government stake, if executed with defined oversight and aligned incentives, could stabilize Intel’s position as America’s chip anchor. However, such support is not a cure-all. The real test lies ahead: regaining process leadership, scaling foundry services, and rebuilding relevance in a reshaped global tech landscape. The government can bolster—but not substitute—Intel’s execution.