Kaltura (NASDAQ:KLTR), a small-cap SaaS player best known for its video platform solutions, has just made a bold move that could redefine its business model. On November 10, 2025, the company announced a definitive agreement to acquire eSelf.ai, an emerging deep tech lab developing real-time, photorealistic AI avatars and conversational agent technology. The deal, valued at approximately $27 million, includes $7.5 million in upfront cash, $12.5 million in earn-outs over three years, and 4.69 million shares (about 3% of Kaltura’s outstanding stock) tied to retention provisions. The transaction is aligned with Kaltura's strategy to evolve from a traditional video content company into a rich media-powered, AI-infused customer and employee experience (CX & EX) platform. As we dive deeper into this deal, we see that Kaltura sees eSelf as more than just an acquisition—it looks more like a gateway to the next generation of immersive video and AI.

Enhanced CX & EX Through Real-Time Conversational Agents

The biggest synergy Kaltura stands to gain from acquiring eSelf is the integration of immersive, real-time conversational virtual agents into its existing video platform. These aren't just static AI chatbots—we're talking about avatars that see, hear, and speak, capable of understanding screen content and interacting in over 30 languages. By embedding these agents into Kaltura’s suite of products, such as video portals, LMS and CMS extensions, virtual classrooms, and TV streaming apps, Kaltura can significantly elevate the quality of user interaction. The potential use cases are wide-ranging: onboarding, customer care, sales, training, and even virtual teaching. The company envisions these avatars replacing or supplementing roles traditionally handled by humans, streamlining operations, improving engagement, and potentially reducing costs for clients. These agents could be off-the-shelf solutions or customized via Kaltura's development tools. The ability to integrate with third-party platforms such as CRMs and learning systems further boosts their utility. While implementation will take a few quarters, the synergy between eSelf's avatar interface and Kaltura’s video infrastructure could make them a competitive force in the evolving digital experience landscape.

Boosted Product-Led Growth & New Market Penetration

Another synergy lies in how this acquisition may supercharge Kaltura's product-led growth (PLG) strategy. The company plans to offer eSelf's avatar-powered agents as stand-alone, embeddable tools that small and mid-sized businesses (SMBs) can deploy without enterprise-level integration. This self-service capability breaks from Kaltura's traditional large-enterprise focus and opens up a vast new segment. With SMBs increasingly adopting SaaS tools for CX and EX, Kaltura could tap into growing demand with minimal sales overhead. Additionally, the avatar agents can serve as entry points to Kaltura's broader ecosystem, increasing upsell opportunities. Imagine a small business starting with a self-serve AI sales agent and eventually upgrading to Kaltura’s full video content management suite. This low-friction adoption model could accelerate customer acquisition while diversifying the company’s revenue streams. It also shortens the sales cycle—a critical advantage in today’s fast-moving SaaS environment. By leveraging eSelf to scale into the SMB space, Kaltura stands to significantly expand its total addressable market (TAM) with relatively low incremental costs.

Deeper AI Integration Into Video Lifecycle & Content Creation

Kaltura has already rolled out AI-driven products like Genie (an AI content assistant) and Content Lab (for repurposing video into clips, quizzes, and metadata). With eSelf's technology, these tools could gain a serious upgrade. Think video creation on-demand using AI avatars, automated narration, real-time translation, and scene generation tailored to user context. eSelf’s multimodal AI could be the missing link that transforms Kaltura's backend into a fully automated content production studio. This integration positions Kaltura as more than a video hosting platform—it becomes a content intelligence engine. Educational institutions could use this for scalable online learning; enterprises could build customized training videos in minutes. These AI enhancements would also boost content discoverability, engagement, and compliance through enriched metadata and automated workflows. While initial revenue impact from eSelf may be limited until late 2026, the technological synergy significantly raises the value proposition of Kaltura’s product suite.

Strengthened Competitive Position With Unique Differentiators

In a crowded video-tech and AI market, differentiation matters. Kaltura is betting that eSelf gives it unique capabilities not easily replicated by competitors. Unlike point-solution avatar startups, Kaltura offers a vertically integrated video experience platform with established enterprise relationships, extensive data from past content, and scalable infrastructure. When combined with eSelf’s photorealistic avatars and conversational logic, the company creates a defensible moat. Competitors like Synthesia or Hour One are typically focused on video-on-demand avatars, while Kaltura plans to go beyond with live conversational agents embedded across the user journey. Moreover, eSelf agents will be natively integrated into Kaltura's existing products and offer off-the-shelf solutions for industry-specific use cases. This allows Kaltura to hit the ground running with use cases in sectors like telecom, education, healthcare, and enterprise tech. Plus, as the only public company (at the time of writing) making a serious bet on immersive virtual agents, Kaltura may benefit from early-mover advantage in the public markets.

Final Thoughts

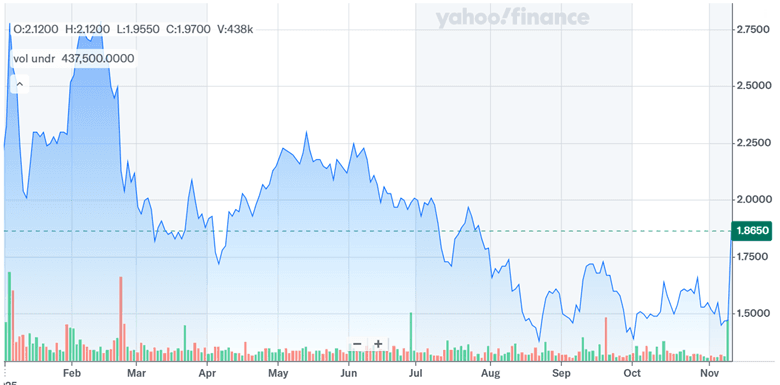

Source: Yahoo Finance

Kaltura's acquisition of eSelf haas been perceived positively by the market and resulted in a sharp jump in its stock price as well as volumes. Kaltura’s forward valuation multiples (as of November 10, 2025) suggest the market is cautiously optimistic—trading at 1.03x NTM EV/Revenue and 8.89x NTM EV/EBITDA, which are on the low end for a SaaS firm making an AI-driven pivot. Its LTM multiples, particularly the negative EV/EBITDA of -65.76x, underscore lingering concerns around historical profitability. However, this latest acquisition represents a bold bet that could pay off with significant strategic benefits, especially in product innovation, market expansion, and operational efficiency. The synergy potential is tangible: enhanced CX & EX, expanded PLG motion, deeper AI integration, and a stronger competitive moat. For investors and stakeholders, the eSelf acquisition is a strategic swing that could redefine Kaltura's trajectory—but it's not without its share of hurdles. Whether this transformation proves accretive or just aspirational will depend on how well Kaltura executes in the quarters ahead.