Kennedy Wilson (NYSE:KW), a small-cap real estate investment company focused heavily on rental housing, recently announced a transformative acquisition: a $347 million deal to acquire Toll Brothers’ Apartment Living platform. This platform, the multifamily division of luxury homebuilder Toll Brothers (NYSE:TOL), includes a seasoned development team, 18 existing properties worth $2.2 billion in AUM, and a pipeline of 29 development sites with a capitalization potential of $3.6 billion. The deal also grants Kennedy Wilson management rights over 20 more properties, adding another $3 billion in AUM, while Toll Brothers gradually exits the multifamily business. But what are the key synergies, and how might this acquisition fit within Kennedy Wilson’s broader small-cap strategy? Let us find out!

Immediate Scale & Asset Synergies In Rental Housing

Kennedy Wilson’s strategic realignment toward rental housing over the past few years has been both deliberate and data-driven. The company has rapidly transitioned its portfolio composition, with rental housing and industrial assets now accounting for 70% of its NOI, up from 58% just three years ago. The Toll Brothers Apartment Living acquisition would further consolidate Kennedy Wilson’s position in this sector, adding 18 properties with $2.2 billion in AUM and a 29-project development pipeline estimated to reach $3.6 billion in capitalization. This influx of high-quality multifamily assets boosts the company's total AUM—which already reached a record $30 billion in Q2 2025—while deepening its exposure to institutional-grade rental product. Strategically, the timing is apt: the multifamily construction wave from 2023 is largely absorbed, and new starts have plummeted, setting the stage for strong rental growth. This acquisition aligns with Kennedy Wilson’s goal of pushing rental housing to 80% of its AUM within two years. Given the company’s significant development experience and infrastructure—across both the U.S. and European markets—it can immediately leverage Toll Brothers’ under-development projects and operational platform without needing to build internally. The assets being acquired are spread across premium markets, giving KW geographic diversification while enhancing scale in regions where it already has operating leverage. Moreover, Toll Brothers’ withdrawal from multifamily opens the door for Kennedy Wilson to become a top-tier player in multifamily development, bridging equity and credit solutions across a single investment management platform. For a small-cap firm looking to scale its fee income while reducing exposure to volatile asset classes like office, this is a strategic coup.

Fee-Bearing AUM Growth & Enhanced Investment Management Economics

Kennedy Wilson’s investment management platform is entering a period of significant inflection, and the acquisition of Toll Brothers’ multifamily arm serves as a powerful accelerator. In Q2 2025, the firm reported record fee-bearing capital of $9.2 billion, with investment management fees growing 39% year-over-year to a quarterly high of $36 million. By acquiring not just assets but also management rights for an additional 20 properties worth $3 billion in AUM, Kennedy Wilson increases both its scale and its recurring fee income. This is critical for a company that is aiming to shift toward a capital-light, fee-driven model—an evolution that aligns with broader private equity trends. The firm already manages $13 billion in co-investment portfolio assets and has proven its ability to monetize fee streams through both equity and credit platforms. The addition of an entire development team from Toll Brothers ensures continuity and operational efficiency, minimizing onboarding friction while positioning KW to generate promote income and development fees from the $3.6 billion pipeline. The combination of recurring fees, development upside, and enhanced third-party capital relationships significantly improves the firm’s return on equity without requiring material balance sheet exposure. As more institutional investors seek access to stable multifamily returns without taking on operating risk, Kennedy Wilson stands to become an increasingly attractive sponsor. For a small-cap stock seeking valuation re-rating, building visible, growing, and recurring earnings streams via fee income could be a differentiator—especially as the company seeks to improve its low multiple profile relative to real estate peers.

Operational Leverage & Platform Efficiencies Through Integration

Another critical synergy from the acquisition lies in the operational domain. Kennedy Wilson is not just acquiring assets and people—it is integrating a proven platform into its existing U.S. rental housing business, which includes 40,000 apartment units and another 30,000 units financed through its real estate credit vertical. The Toll Brothers Apartment Living team comes with development expertise, relationships with local governments, zoning experience, and vendor connections—all of which Kennedy Wilson can scale across its broader multifamily strategy. This allows the company to reduce per-unit development costs, accelerate permitting and entitlement processes, and improve absorption rates through proven operational models. Moreover, Kennedy Wilson’s real estate credit platform—bolstered by a $4.1 billion construction loan portfolio acquired from PacWest—can now be leveraged alongside the development pipeline from Toll Brothers to offer integrated equity and credit packages to investors and joint venture partners. The company has already demonstrated that this hybrid model can drive a 27% IRR on repaid loans, with most of its loans underwritten at conservative 55–65% loan-to-cost ratios. Combining that financing engine with Toll Brothers’ pipeline creates a full-stack capability: from land acquisition and development to stabilization, fee generation, and eventual asset recycling. This internal integration leads to margin expansion, tighter control over execution, and reduced dependency on volatile external partners or third-party managers. Additionally, by concentrating efforts in multifamily—a less cyclical, high-demand segment due to housing shortages—the company positions itself for more stable operating cash flow, even in turbulent macro environments.

Accelerated Strategic Shift Amid Favourable Housing Fundamentals

The Toll Brothers acquisition is more than a tactical deal—it is a strategic accelerant for Kennedy Wilson’s ongoing pivot toward rental housing. CEO Bill McMorrow has publicly stated the firm’s target of increasing multifamily exposure to 80% of AUM, and the acquisition allows KW to leapfrog years of organic development. This shift comes as fundamentals in the multifamily space remain structurally sound: affordability pressures in the single-family housing market continue to push households toward rentals, while the U.S. remains undersupplied by millions of units. Kennedy Wilson has taken advantage of this imbalance by originating $6 billion in rental housing construction loans since forming its credit team, and now complements this vertical with equity investments at scale. From a macro standpoint, the slowdown in new apartment starts after 2023 means that supply is thinning, setting up the market for stronger rental growth in 2026 and beyond. In this context, Kennedy Wilson's acquisition appears well-timed, particularly as its Pacific Northwest and Mountain West portfolios—regions where affordability and job growth trends remain strong—saw NOI growth of over 5% in Q2. Furthermore, Toll Brothers' exit from multifamily gives Kennedy Wilson exclusive access to a turnkey development pipeline that could be difficult to replicate organically. For a small-cap firm competing with larger REITs and institutional sponsors, the deal provides a fast-track toward becoming a more dominant player in a defensible asset class.

Final Thoughts

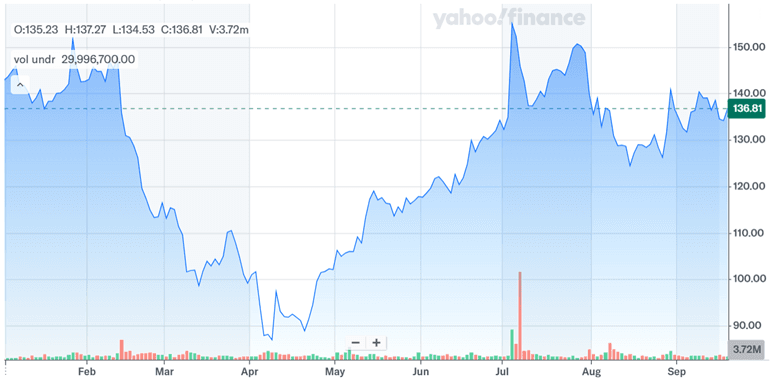

Source: Yahoo Finance

As we can see in the above chart, Kennedy Wilson’s stock price has remained more or less flat ever since the announcement of the acquisition of Toll Brothers’ Apartment Living platform. The transaction, expected to close in October 2025, is positioned to significantly boost Kennedy Wilson’s scale, particularly in the rental housing sector where the company already has a dominant footprint of 70,000 units either owned or financed. However, the market does not see a strong upside for now which is what explains the limited impact on the stock price. From a valuation standpoint, Kennedy Wilson trades at an LTM EV/EBITDA multiple of 27.92x and LTM P/S of 2.26x. Its trailing LTM P/E remains deeply negative (-13.26x), and its levered free cash flow yield sits at -23.1%. While these metrics may eventually improve with scale and fee growth, they also underscore the market’s skepticism about earnings quality and consistency. To sum up, we believe that whether the Toll Brothers deal creates long-term value or not will depend on Kennedy Wilson’s integration efficiency, capital allocation discipline, and the resilience of multifamily fundamentals in an evolving macroeconomic environment.