Lowe’s Companies (NYSE: LOW) is accelerating its pivot toward professional contractors with an $8.8 billion agreement to acquire Foundation Building Materials (FBM), a major North American distributor of drywall, ceilings, and framing supplies. This move, following its $1.33 billion acquisition of Artisan Design Group in April, reinforces Lowe’s broader strategy to capture a larger share of the $250 billion Pro market—a segment that now outpaces DIY in both growth and resilience. The shift comes amid softening consumer demand and rising competition from Home Depot, which recently agreed to buy GMS for $4.3 billion to expand its own Pro distribution footprint. With FBM’s 370+ locations and 40,000+ contractor accounts, Lowe’s is positioning itself to compete more directly in the commercial construction supply chain. Let us analyze this most recent deal and evaluate the strategic synergies Lowe’s could unlock through this acquisition.

National Jobsite Logistics Network Built For Pro Demand

The most significant synergy Lowe’s stands to gain from FBM is a purpose-built national logistics platform optimized for serving professional contractors. Unlike the in-store, cart-based fulfillment model typical of Lowe’s retail operations, FBM’s business is structured around just-in-time jobsite delivery of heavy, volumetric materials like wallboard, ceiling systems, and framing. Its more than 370 locations across the U.S. and Canada are designed for scale, proximity to construction zones, and efficiency in handling contractor-sized orders. This infrastructure is not merely additive—it solves a core limitation that has long plagued big-box retailers attempting to serve the Pro segment: the inability to meet the demanding fulfillment schedules and large-order requirements of commercial construction workflows. Lowe’s can immediately absorb FBM’s regional delivery hubs and leverage its contractor-trained sales force and logistics expertise to build a parallel distribution network serving multifamily, institutional, and light-commercial construction. By integrating FBM’s fleet operations and jobsite routing systems, Lowe’s can unlock route optimization efficiencies and reduce cost-per-drop metrics that are critical in the Pro business. This deeper operational capability also supports a more sophisticated omnichannel model, enabling contractors to research and price online but schedule large material drops on tight construction timelines. Moreover, FBM’s scale complements Artisan Design Group’s installation-focused footprint, creating a vertically integrated supply and service model that supports the full project lifecycle—from base construction materials to finished interior design packages. Together, they equip Lowe’s with a cohesive Pro ecosystem that was previously impossible to build organically without years of capex and ground-up logistics planning.

Procurement Synergies & Margin Leverage

A major financial upside from acquiring FBM lies in procurement consolidation and supply chain optimization. Lowe’s already benefits from scale economics in its retail operations, but FBM adds another layer of direct manufacturer relationships, especially in niche Pro categories like insulation, ceiling tiles, and commercial-grade framing. These relationships can be rationalized and expanded across Lowe’s broader supplier base, creating opportunities for volume discounts, SKU harmonization, and more efficient inbound logistics. Importantly, FBM’s buying power is concentrated in a more fragmented vendor landscape compared to consumer hardware, which gives Lowe’s more room to negotiate favorable pricing on Pro-exclusive materials. Additionally, FBM’s contract-focused pricing models and negotiated terms with large contractors offer lessons that Lowe’s can adapt across its Pro desk and salesforce. Integrating ERP systems and inventory planning tools between the two companies will enable more precise demand forecasting, lower safety stock requirements, and better inventory turns—key factors in freeing up working capital and boosting return on invested capital (ROIC). Furthermore, Lowe’s could leverage FBM’s in-market warehousing to execute more cross-dock shipments, reducing inventory dwell time and improving in-stock rates for high-demand Pro materials. Combined with the operating leverage from FBM’s existing footprint, these supply chain efficiencies could contribute directly to margin expansion. The deal also introduces synergies in vendor rebates and trade program alignment. With the scale of both Artisan and FBM under its roof, Lowe’s can explore private-label penetration in categories where branding matters less than price and availability—further enhancing gross margins while remaining competitive in cost-sensitive bids.

Enhanced Revenue Mix & Customer Stickiness

Shifting revenue exposure toward professional customers is a deliberate strategy to diversify away from the more volatile, interest-rate-sensitive DIY segment. Professional contractors place recurring, large-scale orders driven by project timelines, not consumer sentiment, providing Lowe’s with a more predictable top-line profile. The FBM acquisition helps rebalance this revenue mix by immediately adding a business that derives nearly all of its sales from commercial clients, many of whom operate under long-term agreements or high-frequency project cycles. These relationships not only deliver higher order volumes per customer but also create stickier engagement through service expectations, pricing consistency, and fulfillment reliability. The Pro customer, unlike the weekend renovator, is not easily swayed by price alone—loyalty is built around logistical dependability and technical support. Lowe’s can leverage FBM’s inside sales capabilities, order tracking software, and relationship-driven sales model to introduce deeper client account management and create bundling opportunities across its entire portfolio—from structural products to finishing materials and installation services. Moreover, the business cadence of Pro clients opens the door to service monetization opportunities: equipment rentals, fleet financing, rebate programs, and project-specific consulting services. With FBM under its umbrella, Lowe’s is better equipped to support a full B2B client lifecycle, which may improve retention and wallet share. It also facilitates a tiered engagement model, where high-value clients receive differentiated service levels—a practice already common in the building materials distribution industry but not yet fully optimized within Lowe’s current operations. In the long term, a better-aligned mix between retail and Pro could reduce earnings volatility, provide better forecasting precision, and unlock higher margin potential.

Competitive Counterplay In A Consolidating Industry

The timing of Lowe’s move to acquire FBM is no coincidence. In June 2025, Home Depot disclosed its $4.3 billion acquisition of GMS, another Pro distribution platform with substantial scale and reach. As the two home improvement giants race to dominate the Pro contractor market, acquisition-driven expansion has become the fastest route to relevance. Home Depot has historically led in Pro sales, and the GMS deal only widened the gap. By acquiring FBM, Lowe’s is making a definitive counter-move that gives it immediate parity in interior building materials and brings a higher level of vertical integration when combined with Artisan Design Group. Both deals position Lowe’s to compete not just in traditional hardware categories, but across an expanded range of project-critical inputs. However, this aggressive pace of consolidation introduces material execution risk. Integrating FBM’s highly specialized, relationship-based distribution business into a retail-centric organization like Lowe’s is a complex cultural and operational challenge. The success of this strategy hinges on Lowe’s ability to preserve FBM’s contractor-centric DNA—localized decision-making, experienced sales teams, and jobsite support—while extracting back-end efficiencies and enforcing cost discipline. Furthermore, as the Pro landscape consolidates, margin pressure from rival distributors, increased customer expectations, and ongoing price competition will test Lowe’s ability to retain share without eroding profitability. The acquisition arms race may also trigger further M&A activity from smaller regional players or international entrants, changing the dynamics of what has traditionally been a fragmented distribution market. While FBM offers immediate strategic benefits, it also forces Lowe’s deeper into a competitive trench where scale, speed, and specialization will dictate who wins.

Final Thoughts

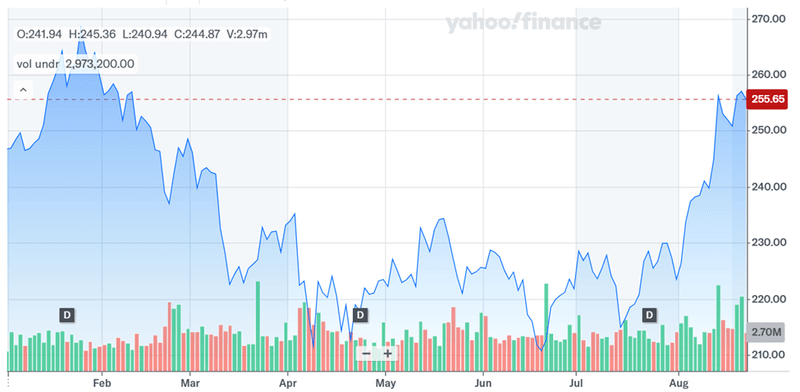

Source: Yahoo Finance

Lowe’s stock price zoomed up after its positive set of results coupled with the $8.8 billion acquisition of Foundation Building Materials. The move is a bold step in Lowe’s ongoing strategic shift toward the Pro segment, and it follows a clear pattern of industry-wide consolidation aimed at capturing more resilient, margin-accretive revenue streams. The deal introduces compelling synergies across logistics, procurement, customer engagement, and competitive positioning, particularly when combined with the recent Artisan Design Group acquisition. At current LTM valuation multiples—EV/EBITDA of 14.19x, EV/EBIT of 16.93x, and a P/E of 21.01x—Lowe’s stock trades at a premium that implies market confidence in flawless execution. If integration falters or synergy capture lags, this valuation could face downward pressure. Whether or not the transaction closes, Lowe’s strategic intent is clear: the battle for the Pro contractor is just beginning, and scale alone won’t guarantee success.