As the geopolitical fight for technological supremacy intensifies, Nvidia (NASDAQ:NVDA) stands at the epicenter—straddling U.S. national security imperatives and China’s ambition for AI dominance. The chipmaker, whose GPUs are foundational to modern AI systems, has had to redesign its product roadmap and revenue model to preserve access to China—one of its most critical but politically sensitive markets. In response to tightening U.S. export restrictions, Nvidia introduced the H20, a downgraded AI chip specifically designed for compliance. But even this compromise has come under fire. Beijing has discouraged purchases, citing national security risks and surveillance concerns, while demanding cybersecurity reviews and hinting at a broader pivot toward domestic champions like Huawei. In a highly unusual arrangement, Nvidia has also agreed to give the U.S. government a 15% cut of its China AI chip revenue in exchange for export licenses—an unprecedented intersection of commerce and diplomacy. Clearly, this appears to be a fragile equilibrium and it is worth analyzing the potential upsides and downsides of this arrangement.

Flexible Design Strategy Anchors Continued Relevance

Nvidia’s ability to sustain demand in China despite aggressive U.S. controls hinges on its modular design adaptability. Following the 2023 and 2024 export control rule updates, which banned the export of top-tier GPUs such as the A100 and H100, Nvidia responded with downgraded variants like the A800 and, more recently, the H20. These chips maintain compatibility with Nvidia’s CUDA software stack while operating below the performance thresholds that trigger export bans. The H20, built on the Hopper architecture, is optimized for inference rather than training—positioning it within a narrow legal window for Chinese use. After receiving temporary approval in July 2025, Nvidia was flooded with over 700,000 orders, signaling intense unmet demand. However, Beijing’s sudden directive halting purchases—citing security concerns and potential “kill switch” features—led Nvidia to suspend production and seek fresh licensing for a less powerful Blackwell-based chip. Despite these headwinds, Nvidia’s ability to quickly reconfigure chip designs and redeploy manufacturing lines at TSMC, Foxconn, and Samsung reflects operational dexterity. CEO Jensen Huang has made multiple diplomatic visits across Washington, Taipei, and Beijing to keep Nvidia’s footprint viable. Even when faced with shifting rules and skepticism, Nvidia’s engineering agility and production flexibility allow it to extract value from China without breaching U.S. policy lines—preserving its strategic relevance.

Monetizing Ecosystem Depth Through Licensing & Platforms

While chip sales dominate Nvidia’s topline, the firm’s long-term China strategy is increasingly driven by ecosystem monetization—leveraging its dominance in AI frameworks, inference platforms, and software tooling. CUDA remains an industry standard, making migration to domestic Chinese chipmakers difficult despite policy pressure. Nvidia is now pushing this moat further through its growing portfolio of NeMo microservices, the AI Enterprise suite, and enterprise inference containers. These tools allow Chinese enterprises to integrate Nvidia-developed models into custom workflows, even if training is outsourced to sanctioned local players. Furthermore, Nvidia’s licensing deals—which include revenue-sharing models like the 15% cut pledged to the U.S. government—open a new business model where value can be extracted through platform economics rather than hardware volumes. The company's Q1 FY2026 call highlighted traction in inference-heavy workloads, a segment less reliant on the highest-end silicon. Even as China’s push for domestic self-sufficiency intensifies, local firms continue relying on Nvidia’s ecosystem to meet quality, efficiency, and compatibility benchmarks. Crucially, this positions Nvidia as more than a chipmaker—it becomes a systems infrastructure layer underpinning the AI economy. By prioritizing software integration, cloud inference, and model delivery, Nvidia reduces its exposure to physical export risks while continuing to monetize the AI boom indirectly, even under tightening global scrutiny.

China Market Fracture As Trust Erodes & Substitutes Emerge

Despite demand strength, Nvidia’s position in China is deteriorating due to rising mistrust, policy retaliation, and the accelerating rise of domestic competitors. Beijing’s sudden reversal on H20 procurement—after pushing Nvidia to seek export licenses—exposed deep skepticism about U.S. intentions. Allegations that H20 chips contain “backdoors” or allow remote disabling have led to cybersecurity reviews and a government order instructing Alibaba, ByteDance, and others to halt purchases. At the same time, Huawei’s Ascend chips—though less efficient—have gained ground by offering political reliability and localized control. Chinese officials believe the reintroduction of Nvidia chips could undermine domestic chip development momentum, raising concerns about national dependency. Even performance compromises aren’t enough to ensure market acceptance if security narratives dominate. Meanwhile, Nvidia’s revenue-sharing arrangement with the U.S. has triggered fresh backlash in China, with critics labeling the deal a geopolitical Trojan horse. While Nvidia insists the H20 is not intended for military or government use, public perception may not align. This erosion of trust, combined with an increasingly fragmented regulatory and commercial landscape, threatens to turn Nvidia from a preferred partner into a problematic foreign dependency—capping long-term scalability in the region.

Systemic Exposure to Supply Chains & Export Policy Volatility

Beyond market perception, Nvidia faces systemic vulnerabilities stemming from its supply chain concentration and export dependency. Advanced chips like the H20 and Blackwell variants are manufactured almost entirely by Taiwan Semiconductor Manufacturing Company (TSMC), exposing Nvidia to regional geopolitical flashpoints, particularly in the Taiwan Strait. While Jensen Huang has publicly emphasized the importance of peace and economic interdependence, the concentration of manufacturing in a potential conflict zone creates undeniable delivery and pricing risk. Moreover, U.S. export policy remains fluid and increasingly politicized. In just two years, Nvidia has faced four rounds of regulation updates, forcing it to reengineer, delist, or redesign entire chip lines. This undermines planning visibility and product launch cadence. The 15% revenue-sharing arrangement with the U.S.—while a near-term workaround—sets a potentially dangerous precedent: future approvals may be tied not just to technical thresholds, but to fiscal concessions. Such arrangements could invite international scrutiny, antitrust questions, or retaliatory tariffs in other regions. In short, Nvidia’s business is not only vulnerable to geopolitical currents but also to evolving trade architecture where rules are rewritten mid-cycle. These disruptions compound the challenge of sustaining investor confidence in the durability of China-based revenues, particularly when political winds shift.

Final Thoughts

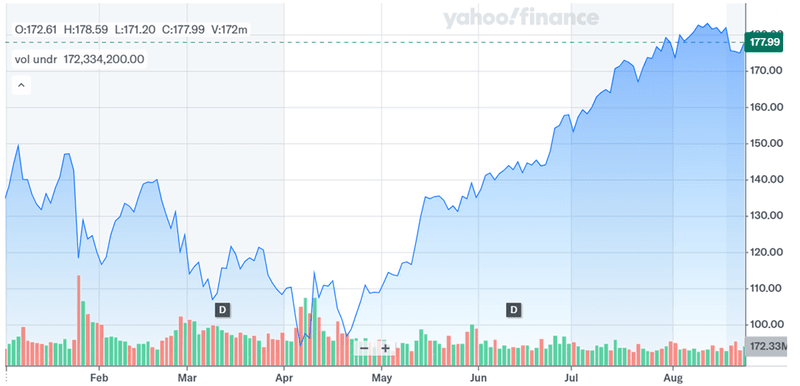

Source: Yahoo Finance

There is little that can slow down Nvidia’s stock price growth given its heavily monopolistic position in its domain, not just because its chips but also because of the overall software + hardware architecture that the company has built over the past few years. The company has shown it can adapt chip designs quickly, secure limited export approvals, and pivot toward software-based revenue streams when hardware access is compromised. Its CUDA ecosystem remains entrenched in China, and demand for AI compute—even at lower performance thresholds—has not abated. Yet the landscape is fragile. Security distrust in China, the emergence of domestic substitutes, supply chain exposure to Taiwan, and unpredictable U.S. export frameworks pose real and possibly intensifying threats. At an LTM EV/EBITDA of 48.72x and LTM P/E of 57.40x, the stock is priced for continued growth and dominance. This premium reflects faith in Nvidia’s ability to outmaneuver disruption. But with China’s AI market fragmenting and global tech decoupling accelerating, Nvidia’s position will likely require ever more delicate recalibration to preserve both access and autonomy.