Have you heard the buzz around Ondas Holdings (NASDAQ:ONDS) lately? The small-cap wireless tech company is stirring things up with talks of a possible acquisition of Sentry Cellular Systems, a player that specializes in secure cellular tech for the military. After its Q2 2025 earnings update, Ondas confirmed it is deep in discussions with Sentry—no deal yet, but it’s getting serious. What’s the big deal? Well, Ondas wants to move beyond just railroads and industrial systems. By bringing Sentry into the fold, it could fast-track its entry into military-grade communications, especially with the Department of Defense looking for next-gen, secure, private 5G networks. It is a bold step that could open new doors and give Ondas some powerful tech to play with. Let us break down why this potential match-up could be a game-changer and what each side brings to the table.

Integration Of SDR & Tactical Cellular Solutions Could Accelerate Government Adoption

One of the most tangible synergies Ondas could derive from acquiring Sentry CS lies in the complementary nature of both companies’ technology stacks. Ondas Networks is known for its FullMAX software-defined radio (SDR) platform, which has historically been applied to rail and industrial applications. However, over the last year, the company has increasingly pivoted toward defense use cases. Sentry CS, on the other hand, brings a cellular architecture tailored for defense-grade private LTE and 5G solutions. This positions the combined company to deliver hybrid communications systems that integrate SDR's flexibility with 3GPP-compliant mobile connectivity. Such dual-mode platforms could serve emerging Department of Defense (DoD) requirements for spectrum agility, secure edge connectivity, and battlefield redundancy. Additionally, Sentry’s modular infrastructure could be adapted to Ondas' existing airborne and drone-based networks, enabling new end-to-end solutions for warfighter communications, ISR (intelligence, surveillance, reconnaissance), and unmanned systems control. The ability to combine FullMAX’s sub-GHz long-range capacity with Sentry’s in-field, high-throughput cellular nodes creates a competitive differentiation against pureplay SDR or mobile network players. With federal R&D dollars increasingly flowing toward hybrid mesh networks and the Pentagon emphasizing "network-of-networks" architectures, this convergence could expedite procurement traction. Moreover, Ondas may gain leverage to participate in prime defense contracts, benefiting from Sentry’s pre-existing relationships and its alignment with National Defense Authorization Act (NDAA) compliance frameworks. For a small-cap like Ondas, such an integrated offering could unlock doors to large, multi-year defense communications programs where its standalone SDR offerings might have previously lacked the breadth to compete.

Cross-Selling Opportunities Across Established Customer Bases

Another strategic benefit of the potential Sentry CS acquisition is the cross-pollination of existing customers across Ondas’ and Sentry’s respective portfolios. While Ondas Networks has traditionally served Class I railroads like BNSF and commercial industrials, its defense exposure is still relatively nascent. Sentry, however, has built inroads into DoD ecosystems through its secure LTE/5G deployments for military applications, particularly in tactical and expeditionary environments. A combined company could unlock immediate cross-selling synergies by introducing Ondas’ FullMAX-enabled systems into Sentry’s defense customer base and vice versa. For example, there may be latent demand for private cellular overlays among Ondas' rail and critical infrastructure clients seeking secure broadband solutions, especially in the context of drone monitoring or automated inspection. Conversely, Sentry's military-grade solutions could be cross-sold into Ondas' existing relationships with infrastructure players looking to expand into tactical communications. This bi-directional sales opportunity is further amplified by the fact that both companies have highly customizable platforms, which can be adapted to diverse use cases without significant redesign. From a channel strategy standpoint, the acquisition could enable Ondas to broaden its federal go-to-market efforts by leveraging Sentry’s defense integrator network, while simultaneously allowing Sentry’s technologies to be positioned as an add-on to Ondas’ existing industrial SDR deployments. The addressable market for mission-critical connectivity continues to expand beyond traditional defense confines, into smart infrastructure and homeland security—domains where the combined entity could carve out differentiated niche offerings.

Operational Leverage From Combined Engineering & Manufacturing Capabilities

Merging with Sentry CS could allow Ondas to achieve greater operating leverage by unifying engineering, R&D, and manufacturing functions. Ondas has been investing in consolidating its production and testing operations for its Airborne and Networks divisions, seeking to cut costs and improve time-to-market. Sentry, which has developed compact, ruggedized 5G base stations and small cell technology, has complementary hardware expertise that could be embedded into Ondas’ core design teams. From a product development standpoint, the combination enables a faster innovation cycle, with potential co-development of integrated SDR-cellular hardware platforms optimized for SWaP (size, weight, and power) constraints. Moreover, Sentry's compact enclosures and high-throughput architectures could be modularized and scaled through Ondas’ emerging airborne platforms, such as those used by American Robotics. On the operations front, shared back-end systems and logistics infrastructure could streamline procurement, reduce BOM (bill of materials) costs, and standardize testing protocols across product lines. Notably, Sentry's focus on standards-based LTE/5G complements Ondas’ proprietary FullMAX waveform, potentially enabling the creation of hybrid chipsets and reducing reliance on expensive, single-source components. This integration could improve gross margins over time, which is critical for Ondas, whose LTM enterprise value-to-gross profit multiple sits at an elevated 357.91x. Any uplift in unit-level profitability from this merger could help rationalize such multiples, particularly as the company faces continued scrutiny over cash burn and negative EBITDA. In addition, combining R&D roadmaps could create a unified product vision that aligns with longer-cycle defense procurement needs, allowing Ondas to better manage investor expectations around delayed revenue recognition typical in government contracts.

Pathway To Recurring Revenue Via Secure Infrastructure Services

Perhaps the most transformative synergy from a potential Sentry CS acquisition would be its contribution toward Ondas' pivot to a more recurring-revenue model. Sentry’s offerings are not limited to hardware—they include managed cellular infrastructure tailored for military use, including private 5G network-as-a-service (NaaS) offerings and long-term operational support agreements. This model introduces stickier revenue streams as agencies often enter multi-year service and maintenance contracts to ensure continuity and compliance. Ondas, which has historically relied on sporadic hardware shipments and milestone-driven defense R&D contracts, could benefit significantly from incorporating Sentry’s infrastructure-as-a-service model into its own revenue structure. This shift could dampen quarter-to-quarter volatility and improve revenue visibility—an important consideration for a small-cap company like Ondas. By bundling Sentry’s secure mobile core management and spectrum services with Ondas’ drone and network hardware, the combined entity could offer turnkey solutions with embedded SaaS or managed service elements. Such hybrid offerings would also improve Ondas’ value proposition in competitive government RFPs (Requests for Proposals), where total lifecycle support is often weighted more heavily than upfront capital expenditures. Additionally, the combined capabilities could open avenues for classified programs where ongoing infrastructure control is essential, further cementing customer lock-in. While the transition toward recurring revenue could take several quarters to manifest, the strategic alignment is already evident in Ondas' recent commentary around diversifying its revenue base and reducing its dependency on lumpy development contracts.

Final Thoughts

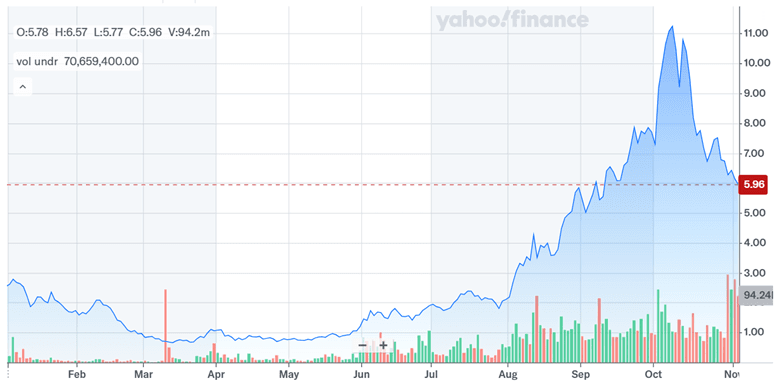

Source: Yahoo Finance

Ondas’ stock performance has been volatile and lately, its stock has been on the downslide after a massive runup until early October 2025. One reason for the much needed correction is the company’s LTM enterprise value-to-sales multiple of 127.61x and EV/gross profit multiple of 357.91x which is unbelievably high. The company continues to operate at negative EBITDA and levered free cash flow levels which poses an additional risk for shareholders. All these factors prove how important the potential acquisition of Sentry CS is, for Ondas, in the coming months. Ultimately, whether or not the Sentry CS deal closes, the discussions highlight a clear strategic intent from Ondas to evolve beyond its current scope—but the path to sustainable value creation remains uncertain and fraught with challenges.