SiriusPoint’s (NYSE:SPNT) latest strategic move is turning heads on Wall Street. On September 29, 2025, the small-cap reinsurance player announced the sale of its wholly owned supplemental health insurance program manager, ArmadaCare, to Ambac Financial Group for $250 million. The transaction marks a significant milestone in SiriusPoint’s long-term strategy to focus on specialty underwriting and capital-light business lines. For small-cap Ambac, the move represents a potential pivot into high-growth health benefits, signaling a broader diversification play. The agreement—set to close in Q4 2025—values ArmadaCare at approximately 14x EBITDA and is expected to deliver a pre-tax gain of $220–$230 million. Let us dive deeper into this deal and evaluate the core drivers behind Ambac’s interest and the potential synergy it hopes to extract from SiriusPoint’s ArmadaCare.

Access To High-Margin Fee-Based Revenues In A&H

ArmadaCare operates in the Accident & Health (A&H) space—one of SiriusPoint’s most stable and profitable business lines. The company’s fully consolidated A&H MGAs generated 16% service revenue growth in Q2 2025 and 13% growth year-to-date, with a service margin of 23.6% and net service fee income of $28 million in the first half. This consistent margin profile offers small-cap Ambac a compelling entry into fee-based insurance services with low volatility and high predictability. For SiriusPoint, A&H remains a diversification tool, acting as a volatility buffer across underwriting cycles. For Ambac, acquiring ArmadaCare is not just about topline growth—it’s about securing high-margin recurring income with minimal capital at risk. Unlike traditional underwriting businesses that are exposed to cyclical losses or CAT events, the MGA model underpinning ArmadaCare is capital-light and operationally nimble. ArmadaCare’s short-tail risk exposure, which is typically resolved within 2-3 years, adds further attractiveness by minimizing long-tail reserving risks—a feature that would be particularly useful to Ambac as it scales. Furthermore, in the current yield environment, fixed income investments may not offer the same margin expansion potential. ArmadaCare’s operating profile provides Ambac an opportunity to improve its return on equity through non-interest-sensitive earnings. Lastly, given that SiriusPoint has a track record of being prudent with reserving and has shown 17 consecutive quarters of favorable reserve development, the quality of ArmadaCare’s underwriting processes likely meets rigorous standards—another incentive for Ambac seeking to bolster earnings quality.

Diversification From Ambac's Structured Finance & Legacy Portfolio

Ambac Financial Group has traditionally operated within the structured finance and legacy financial guarantee sectors. While these segments provide steady but limited upside, ArmadaCare opens the door for strategic diversification into a growing healthcare insurance segment that operates largely outside the traditional financial markets. This diversification is not merely additive; it's transformative. ArmadaCare’s supplemental insurance offerings are tailored to executive benefits and employer-sponsored plans, sectors that continue to grow irrespective of broader macroeconomic cycles. The opportunity here is particularly enticing for Ambac’s small-cap investor base, which has long sought growth avenues beyond the legacy bond insurance portfolio. ArmadaCare helps Ambac sidestep the cyclicality and reputational baggage tied to municipal and structured product exposures. Furthermore, by acquiring a player with established distribution via Managing General Agents (MGAs), Ambac can leapfrog into an ecosystem already vetted by SiriusPoint's underwriting standards. This provides instant scale and legitimacy, avoiding the lengthy licensing, compliance, and staffing processes of a greenfield insurance build-out. Lastly, because ArmadaCare has maintained a capacity relationship with SiriusPoint through 2030, Ambac would gain not just a portfolio of clients and infrastructure but also underwriting support and guidance—critical for a company entering a new vertical.

Strategic Capital Allocation & Low-Capex Growth

SiriusPoint’s decision to offload ArmadaCare for $250 million—realizing a $220–$230 million pre-tax gain—highlights the capital efficiency embedded in the MGA model. For Ambac, the acquisition represents an opportunity to deploy excess capital toward low-capex growth. In contrast to traditional insurance carriers that require substantial regulatory capital to expand underwriting, ArmadaCare’s business model scales through service fee income rather than balance-sheet risk. From Ambac’s standpoint, this means greater operational leverage: a small increase in top-line business can generate disproportionately high margins with limited capital outlay. This kind of asset-light model is particularly attractive at a time when capital costs remain elevated and regulatory constraints are tightening. Moreover, as SiriusPoint has shown in its quarterly performance—with an 89.5% combined ratio in Q2 and 11 straight quarters of underwriting profitability—disciplined growth from specialty lines can deliver strong returns without compromising solvency or risk appetite. The deal structure also reduces integration friction. Since SiriusPoint retains underwriting capacity with ArmadaCare through 2030, Ambac can defer major capital injections while continuing to reap the benefits of embedded underwriting economics. This is an appealing value proposition, particularly when viewed in contrast to the potential ROEs from Ambac’s traditional businesses. Furthermore, the acquisition strengthens Ambac’s ability to optimize its enterprise value-to-EBITDA multiple, especially as SiriusPoint’s ArmadaCare was valued at 14x EBITDA—well above the small-cap average, yet justified by its fee-heavy model and stable margins.

Reputation Transfer & Program Ecosystem Access

One of the more intangible yet highly valuable assets in this deal is SiriusPoint’s reputation in the MGA and program business space. Winning "Program Insurer of the Year" in 2025, SiriusPoint has cultivated a reputation as a partner of choice for MGAs, rejecting over 80% of partnership opportunities to maintain underwriting discipline. ArmadaCare benefits from this halo effect and carries with it the credibility of being part of SiriusPoint’s high-bar selection process. For Ambac, acquiring ArmadaCare is a fast track into this ecosystem—an ecosystem that not only facilitates access to new MGA partnerships but also comes with a built-in reputational premium. In Q2 2025, SiriusPoint added four new MGA partnerships, three of which were expansions with existing long-term partners. This showcases a strong pipeline and partner retention—a critical marker of sustainability in a competitive insurance landscape. With MGAs accounting for a significant share of specialty insurance distribution, especially in lines like Accident & Health, Environmental, and Surety, Ambac would be stepping into a pre-vetted and functioning growth platform. Additionally, ArmadaCare’s integration into SiriusPoint’s broader insurance ecosystem has allowed for both operational and risk alignment, meaning the due diligence burden on Ambac is potentially lower, and the transition risk is mitigated. Even the ongoing partnership with SiriusPoint until 2030 offers Ambac a backstop, reducing underwriting volatility during the initial years post-acquisition. In essence, Ambac wouldn’t just be acquiring a book of business—it would be acquiring a growth conduit with built-in governance, market access, and brand equity.

Final Thoughts

Source: Yahoo Finance

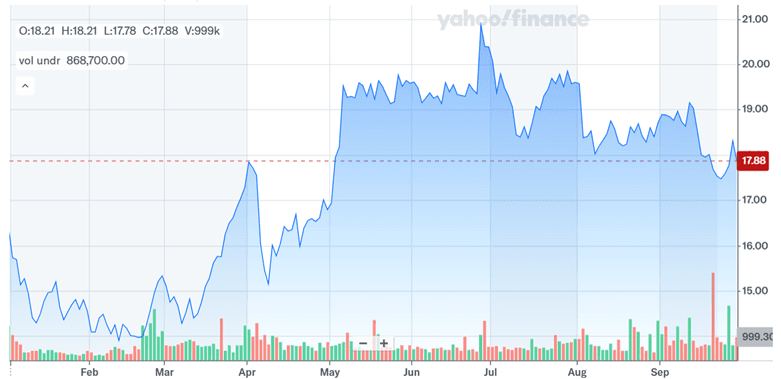

SiriusPoint’s stock price has been more or less flat over the past few months and has been hovering between the range of $17-$19. While we perceive the sale of ArmadaCare to Ambac Financial Group to be a positive move offering both financial and strategic upside, the market clearly does not seem to have factored it in. A pre-tax gain of $220–$230 million on a $250 million deal implies ArmadaCare had been significantly accretive to SiriusPoint's financials—especially considering that the transaction values it at 14x EBITDA, markedly higher than SiriusPoint’s own trailing valuation multiples. As of September 29, 2025, SiriusPoint trades at a modest 0.75x LTM price/sales and 5.94x LTM EV/EBITDA, signaling undervaluation relative to its asset quality and consistent underwriting results. However, the transaction is not without its caveats. While the MGA model promises capital efficiency, it also requires diligent oversight and deep actuarial insight—something Ambac has yet to demonstrate at scale. Additionally, questions remain about how much of ArmadaCare’s success has been tied to SiriusPoint’s governance and support, and whether that can be replicated under new ownership. As both parties head toward closing the transaction in Q4 2025, the deal offers a lens into shifting industry dynamics where asset-light, fee-heavy platforms are becoming increasingly valuable—even in the small-cap insurance space.