[ad_1]

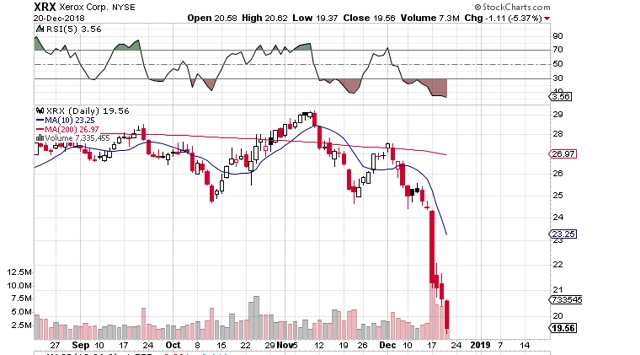

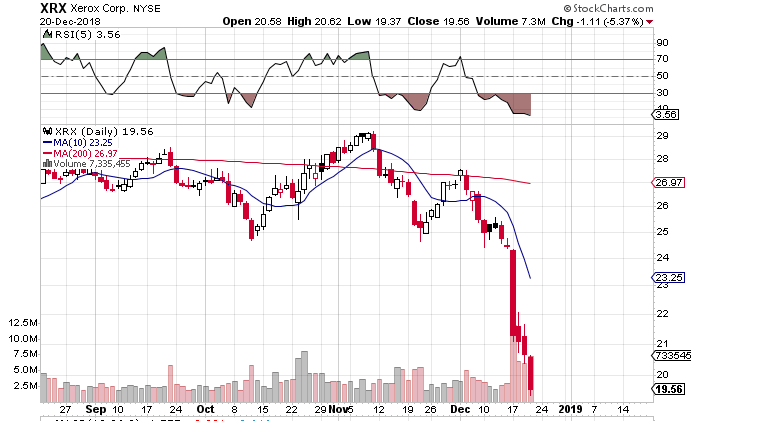

Xerox Corporation (XRX) has all of the hallmarks of a pretty worth play at present. The firm is buying and selling beneath its book value and has a ahead earnings a number of of solely 5.8. Furthermore, the firm’s money stream a number of is 6.0 and its gross sales a number of is 0.5. The firm pays out a 5.1% dividend yield which equates to $1 per share when taken over a 12-month interval. Furthermore, and most critically, Xerox’s present working income are available at $883 million over a trailing 12-month common.

All of the valuation metrics above (except money stream) are nicely behind what the trade usually is buying and selling at. The dividend is greater than double what the trade is buying and selling at which once more is engaging from a price perspective. The debt to fairness ratio is 0.93.

However, there’s a lot extra to worth investing than low cost earnings or a low e book a number of. This stock is reasonable for a motive. Our job is to seek out out if it might get better or not. We like to observe the traits in different ratios additionally resembling the present ratio and the return on capital metric. The steadiness sheet is at all times vital and extra analysis is required there additionally regardless of the attractiveness of the said debt to fairness ratio of 0.93. Is the dividend protected? If not, this may present one other concern for driving the value decrease. Let’s dig in.

When researching shares which have been completely crushed down, liquidity is the in all probability an important metric one ought to have a look at. No matter how good an organization’s fundamentals are or how engaging its valuation is, if a firm cannot entry capital when it wants it, this normally spells hazard. This why the present ratio is so essential. At present, it is available in at 1.82 which together with final yr (1.91) are the best numbers we now have seen since 2009. We normally search for a present ratio over 2. However, they’re fairly shut and trending in the appropriate route. Current property have been remaining regular across the $5 billion mark, however present liabilities are actually down to shut to $2.7 billion. This provides healthy working capital of over $2.2 billion as its exhibits strength from a liquidity perspective.

If we transfer onto the lengthy-time period financials of the corporate, we now have already said that the firm’s internet debt to fairness ratio is available in at 0.93. What we invariably look right here to see is how correct this quantity is, how inventories are trending and the worth of the goodwill. In our opinion, inventories are remaining stubbornly excessive at $958 million. This quantity is on a par with 2016 stock numbers when the corporate was turning over nearly $2 billion extra. Goodwill within the newest quarter got here in at $3.9 billion. This quantity appears to be like excessive when one compares this quantity to the quantity of property Xerox has on its steadiness sheet. In reality, it makes up 25% of the property of the corporate. Remember this line merchandise represents unlocked potential worth.

Over the previous 4 quarters, the corporate has paid out $272 million out of a free money stream kitty of $778 million. This provides us a money stream ratio of 35% which is engaging. The annualized payout is $1, and because the firm’s curiosity protection ratio presently is available in at 7.01, we do not see any present danger to the dividend.

In abstract, Xerox has all of the hallmarks of a possible worth play. Its robust dividend, low valuation and robust liquidity will certainly appeal to potential worth gamers. The potential concern can be as follows. Although the steadiness sheet could have loads of fairness at present, we really feel the firm should spend closely within the years to return. Whether that is via acquisitions or R&D, Xerox’s print enterprise is more likely to stay underneath stress. This is the issue with investing in an organization the place its core trade is in decline. Managed print providers will assist, however re-invention and transformation should happen. What is encouraging is how earnings estimated have been rising for each this yr and subsequent. We could get lengthy right here as soon as fairness markers backside in unison.

Disclosure: I/we now have no positions in any shares talked about, however could provoke an extended place in XRX over the following 72 hours. I wrote this text myself, and it expresses my very own opinions. I’m not receiving compensation for it (aside from from Seeking Alpha). I’ve no enterprise relationship with any firm whose stock is talked about on this article.

[ad_2]