Zevra Therapeutics (NASDAQ:ZVRA) shares surged after fresh takeover rumors reignited investor interest in the rare-disease biotech. According to a Betaville alert circulating among traders, Collegium Pharmaceuticals (NASDAQ:COLL) had considered acquiring Zevra but could not secure financing to proceed. The alert follows last month’s reports that Zevra may have drawn M&A interest from other parties as well. The timing of this speculation is notable: Zevra has just delivered a 26% quarter-over-quarter jump in net revenue for its flagship drug MIPLYFFA, completed the $150 million sale of a priority review voucher, and submitted a marketing authorization application for arimoclomol in Europe. With a $502 million market cap, $217.7 million in cash and investments, and a growing footprint in ultra-rare diseases, Zevra embodies a classic small-cap biotech with both commercial assets and pipeline optionality. Let us analyze this recent confluence of events and understand why the market has reacted so sharply to the unconfirmed takeover chatter.

Strong Market Reaction Signals M&A Optimism

The swift 7.5% stock price increase highlights the market’s sensitivity to M&A rumors, especially among mid-cap biotechs positioned in niche therapeutic areas. Zevra stands out because it already has a commercial-stage asset in MIPLYFFA for Niemann-Pick Type C (NPC), an ultra-rare and life-threatening lysosomal storage disorder. In Q2 2025, MIPLYFFA generated $21.5 million in revenue, a 26% increase from Q1, and the company reported that 129 patients—more than one-third of diagnosed NPC patients in the U.S.—were enrolled on therapy by quarter’s end. Beyond the U.S., Zevra is preparing for European entry with an MAA submission for arimoclomol and an expanded access program (EAP) now reaching 89 patients in select markets. These developments demonstrate both near-term revenue potential and long-term geographic expansion, making Zevra more than a single-asset story. At the same time, Zevra’s valuation multiples have compressed meaningfully, with its NTM EV/Revenue at 3.21x and LTM EV/Revenue at 6.58x as of September 26, 2025, down from double-digit multiples earlier in the year. This combination of commercial traction and discounted valuation helps explain why takeover chatter immediately boosted the stock, as investors began to price in the possibility of value realization through a strategic transaction.

Collegium’s Prior Interest Validates Strategic Value

Collegium’s reported exploration of an acquisition provides independent validation of Zevra’s strategic appeal. As a specialty pharmaceutical company, Collegium’s core competency lies in commercializing niche therapies—a profile well-suited to Zevra’s rare-disease pipeline. Its interest likely centered on MIPLYFFA, which is the only therapy shown to halt NPC progression over 12 months in a pivotal trial, and on Zevra’s ongoing Phase III trial of celiprolol for Vascular Ehlers-Danlos Syndrome (VEDS), another severe genetic condition. Zevra’s Q2 transcript highlights its ability to convert EAP patients to commercial therapy, achieve 52% payer coverage for MIPLYFFA, and sustain high retention rates—all key hurdles in rare-disease commercialization. These attributes align with the type of assets that can drive growth for a specialty pharma acquirer. Even though Collegium could not secure financing, its due diligence likely confirmed that Zevra has de-risked commercial and regulatory pathways, differentiating it from earlier-stage targets. The company’s $217.7 million cash balance, strengthened by the sale of its priority review voucher, also reduces the need for immediate capital infusions, making it an attractive bolt-on for a buyer with operational infrastructure already in place.

Continued Speculation & Buyer Optionality

Collegium’s retreat does not mean Zevra is off the M&A radar. On the contrary, its unique mix of commercial execution, regulatory milestones, and financial flexibility has kept speculation alive. Zevra posted $25.9 million in total Q2 revenue and a net income of $74.7 million driven by the one-time PRV sale, but even on an adjusted basis its net loss was only $3.2 million—showing tighter expense control as it scales. MIPLYFFA’s durability is underpinned by five years of clinical data published in peer-reviewed journals, broadening prescriber confidence and payer acceptance. The company’s European EAP and pending EMA decision signal untapped value outside the U.S. For potential acquirers, Zevra’s compressed valuation multiples are attractive: LTM Price/Sales now stands at 8.84x versus 15.42x a year ago. Its rare-disease focus also offers cross-selling and portfolio diversification opportunities for larger pharma or specialty players seeking non-commodity assets. In short, while Collegium’s financing setback may have delayed one transaction, it may also have created an opening for other strategic or financial sponsors to act, especially given Zevra’s cash-rich balance sheet and ongoing pipeline advancement.

Deal Execution & Financing Risk

The same factors that make Zevra attractive also underscore the execution risks facing any potential buyer. Collegium’s inability to secure financing reflects the current constrained environment for leveraged deals in biopharma, where rising interest rates and tighter credit standards complicate funding. Zevra’s own metrics show why caution may be warranted: its NTM EV/EBITDA multiple is deeply negative at -21.31x, and its LTM EV/EBITDA at -7.58x, indicating ongoing operating losses despite revenue growth. OLPRUVA, Zevra’s other commercial product for urea cycle disorders, has underperformed severely with just one new prescription enrollment in Q2 and a $58.7 million impairment charge recognized. The ultra-rare NPC market is inherently limited by small patient numbers, and while Zevra is working to expand diagnosis through awareness and genetic testing, the total addressable market remains constrained. Competitive dynamics, such as the emergence of AQNEURSA for NPC, further complicate long-term projections. Any acquirer must therefore weigh the upside of MIPLYFFA’s growth trajectory and European expansion against the financial and operational risks of integrating a business still in the early stages of commercialization.

Final Thoughts

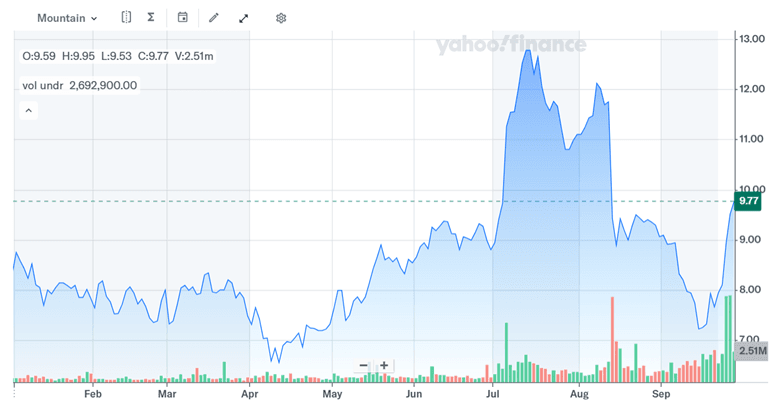

Source: Yahoo Finance

We can see how the renewed takeover chatter has skyrocketed Zevra Therapeutics’ stock while thrusting it into the spotlight. Collegium’s prior interest, though unfulfilled, signaled that Zevra’s rare-disease portfolio, commercial execution, and fortified balance sheet meet the criteria of a strategic acquisition target. Continued speculation suggests other buyers could emerge, especially as Zevra trades at lower valuation multiples than in previous quarters. Yet the company’s limited addressable markets, mixed portfolio performance, and negative EBITDA metrics present tangible risks to any would-be acquirer. As of late September 2025, Zevra’s LTM EV/Revenue of 6.58x and LTM P/S of 8.84x imply a valuation that incorporates optimism about MIPLYFFA but discounts OLPRUVA’s underperformance. Whether this sets the stage for an actual deal or simply reflects market enthusiasm remains uncertain, leaving Zevra at the intersection of strategic opportunity and execution risk.