Zymeworks (NASDAQ:ZYME) just had the kind of week every small-cap biotech dreams about — the kind that can completely change how people see a company. After years of being viewed as a “promising but early-stage” drug developer, Zymeworks suddenly found itself in the spotlight thanks to the strong Phase 3 results of Ziihera, a cancer drug it originally created and later partnered with Jazz Pharmaceuticals to advance. These results showed that Ziihera, when paired with standard chemotherapy, helped patients with gastroesophageal adenocarcinoma live longer without their disease getting worse. That’s a big deal in a cancer type known for tough odds. Investors noticed immediately: Zymeworks’ stock surged 34% in a single day — the biggest jump in its history. And while Jazz’s team ran the late-stage trial, Zymeworks’ science is what made the drug possible in the first place. This turning point has reshaped not just how investors talk about Zymeworks, but how the company now talks about its own future.

Strengthened Scientific Credibility & Expanded Long-Term Value

The Ziihera milestone has fundamentally shifted how the market values Zymeworks’ scientific platform. Historically seen as a small-cap company with potential but little proof, Zymeworks now enters a different echelon—one associated with successful late-stage development. The Phase 3 data presented alongside Jazz Pharmaceuticals marked a breakthrough in clinical efficacy, showing statistically significant improvements in progression-free survival for patients with locally advanced or metastatic gastroesophageal adenocarcinoma. This validation did not occur in isolation. It followed years of platform work, including preclinical design and early-stage human trials spearheaded by Zymeworks before licensing the asset to Jazz in 2022. Importantly, Ziihera’s success does more than validate one asset—it casts a positive halo across Zymeworks’ entire antibody-drug conjugate (ADC) pipeline. The company’s ability to discover, engineer, and deliver biologics that can show real-world benefit enhances the credibility of all future product candidates. Moreover, it creates optionality for new partnerships or even outright acquisitions. For long-term investors, this evolution introduces a narrative of value that extends beyond royalties or milestone payments. While still early, the foundation of scientific legitimacy provides a much-needed counterweight to the historically speculative nature of Zymeworks’ stock. With stronger evidence that its platform can generate not just assets, but drugs that work, Zymeworks is increasingly seen as a validated player in oncology—one with upside tied not just to pipeline announcements, but to clinical results and commercialization potential.

Reframed Narrative Around Execution & Innovation

One of the most dramatic shifts following the Ziihera announcement has been the reframing of Zymeworks’ narrative—from a company grappling with executional delays and management turnover to a developer capable of driving innovation with tangible outcomes. Over the past few years, investor skepticism has centered around strategic shifts, pipeline reprioritization, and leadership transitions that created uncertainty around the company's ability to execute. However, the success of Ziihera has forced a reassessment. Zymeworks’ early-stage development work, formulation chemistry, and clinical design frameworks laid the groundwork for what is now a potentially practice-changing cancer therapy. Although Jazz Pharmaceuticals carried out the Phase 3 trial and will lead commercialization, Zymeworks' fingerprints are embedded in the drug’s biology. This clarity of contribution alters perceptions about the company's ability to deliver innovation—not just in the lab but through real-world impact. Additionally, Zymeworks has already received and expects further milestone payments tied to the success of Ziihera, offering a visible stream of non-dilutive capital to reinvest in internal R&D. Combined with its current portfolio of HER2-targeting ADCs and multispecific antibodies, this financial and scientific success positions Zymeworks as more than a licensing shop—it’s now being recognized for upstream innovation that translates into late-stage wins. Investors are now evaluating Zymeworks in terms of executional maturity, not just scientific promise. The company is gaining credibility not by pivoting its model, but by proving that its model—built on differentiated protein engineering and precision targeting—can generate best-in-class oncology therapeutics.

Momentum Driven By Validation Rather Than Speculation

Unlike many biotech rallies driven by preclinical hype or Phase 1 trial headlines, the recent surge in Zymeworks’ stock is rooted in validation—not speculation. The 34% jump in share price came on the back of hard, late-stage clinical data that was independently reported and externally corroborated by Jazz Pharmaceuticals. This is a critical distinction for investors, particularly those who had previously viewed Zymeworks as a high-risk, pre-revenue biotech dependent on theoretical upside. The Ziihera outcome shifted sentiment from “maybe someday” to “it works today,” and that fundamental pivot has led to greater credibility in analyst models, fund allocation strategies, and institutional holdings. Notably, the nature of the data—showing clear progression-free survival benefit in a high-mortality cancer—adds therapeutic gravity to the results. It’s not a marginal benefit in a rare disease; it’s a measurable improvement in a high-unmet-need area. That kind of validation is rare in small-cap biotech and carries asymmetric upside for companies like Zymeworks that are built around repeatable technology platforms. Moreover, this isn’t a one-off win. The structure of Zymeworks’ pipeline is such that additional ADC programs, including HER2-targeting and other multispecific antibody candidates, now benefit from this tailwind. Investors aren’t just betting on the hope of discovery—they’re recognizing a new pattern of performance that aligns with marketable drug development. This shift from speculative to validated plays makes Zymeworks more attractive to long-only biotech investors and even crossover funds that previously required later-stage exposure to initiate positions.

Visibility Boost & Platform Opportunities Ahead

The commercial success potential of Ziihera and its clinical validation have elevated Zymeworks’ profile not just within oncology circles, but across the biotech investment landscape. Prior to this announcement, Zymeworks’ name rarely appeared in conversations dominated by large-cap ADC developers or high-profile immunotherapy startups. Now, the company is being mentioned alongside firms with billion-dollar market caps and multiple late-stage assets. That visibility matters. It opens doors to additional partnerships, potentially derisks licensing discussions, and may even attract acquisition interest from larger players looking to enter or expand their ADC capabilities. The company’s modular platform is capable of producing bispecific and multispecific antibodies, with applications extending beyond oncology and into autoimmune and inflammatory diseases. What’s more, Zymeworks has shown a willingness to partner early but strategically, allowing it to monetize innovation while maintaining focus on core R&D strengths. In the wake of Ziihera, the market is now more willing to value the entire platform, not just single-asset NPV calculations. With enhanced visibility comes increased scrutiny, but also more flexibility. Future capital raises could be conducted at higher multiples, strategic collaborations might now include better economics, and internal programs may receive more attention from both Wall Street and the medical community. In short, Zymeworks has gone from being a low-visibility science story to a validated platform story, giving it a broader runway to scale its technology across indications and modalities.

Final Thoughts

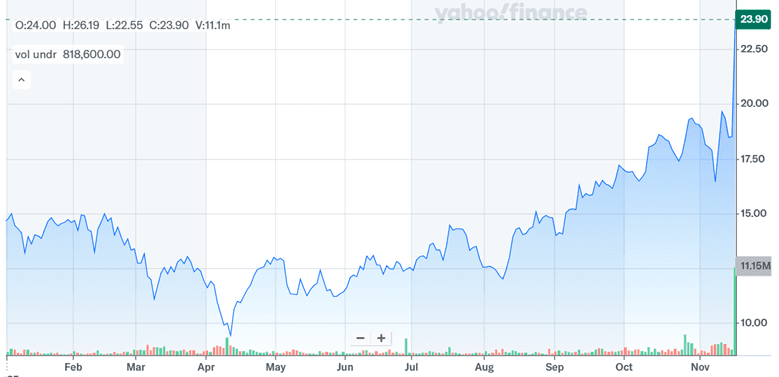

Source: Yahoo Finance

Early shareholders of Zymeworks have been jumping with joy as the stock price has more than doubled since April 2025 as the strong Phase 3 results have changed the way people view the company. Instead of being seen as a small-cap biotech still trying to prove itself, Zymeworks now comes across as an innovator with real clinical success to point to. That shift brings a lot of benefits: more confidence in the science, more interest from investors, and more opportunities for partnerships. But it’s also important to keep the bigger picture in mind. Zymeworks still relies on its partners for the later stages of drug development, and its future earnings from Ziihera will be shaped by the terms of those deals. The company is not yet profitable, and it will still need to carefully manage spending and development risk. You can see this balance reflected in the stock’s valuation. As of November 17, 2025, Zymeworks trades at high revenue multiples — an NTM P/S of 19.9x and an LTM EV/Sales of 11.21x — while its earnings-based ratios remain negative because it’s still investing heavily in its pipeline. So while the Ziihera news gives the company a meaningful boost, it is critical to see how Zymeworks turns this moment into long-term financial strength without stretching itself too thin.