9.2% Dividend Yield With Earnings Growth From Granite Point Merits A Closer Look – Granite Point Mortgage Trust (NYSE:GPMT)

[ad_1]

Granite Point Mortgage Trust (GPMT) has been on our radar because the IPO. It was our largest place for giant components of 2018. However, our ranking is now impartial. The Q3 2018 earnings name was a big think about our resolution to decrease the ranking. We offered an entire breakdown of Granite Point’s Q3 2018 presentation. For the following week that article might be accessible to all readers (no subscription required).

Notes from Granite Point Mortgage Trust Q3 2018 Earnings Call

Note: The earnings name occurred on the morning of November sixth, 2018. This was printed to subscribers in actual-time. We will embody an up to date worth chart on the finish.

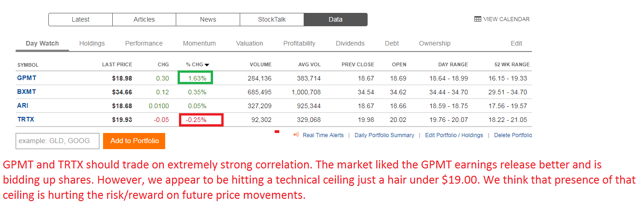

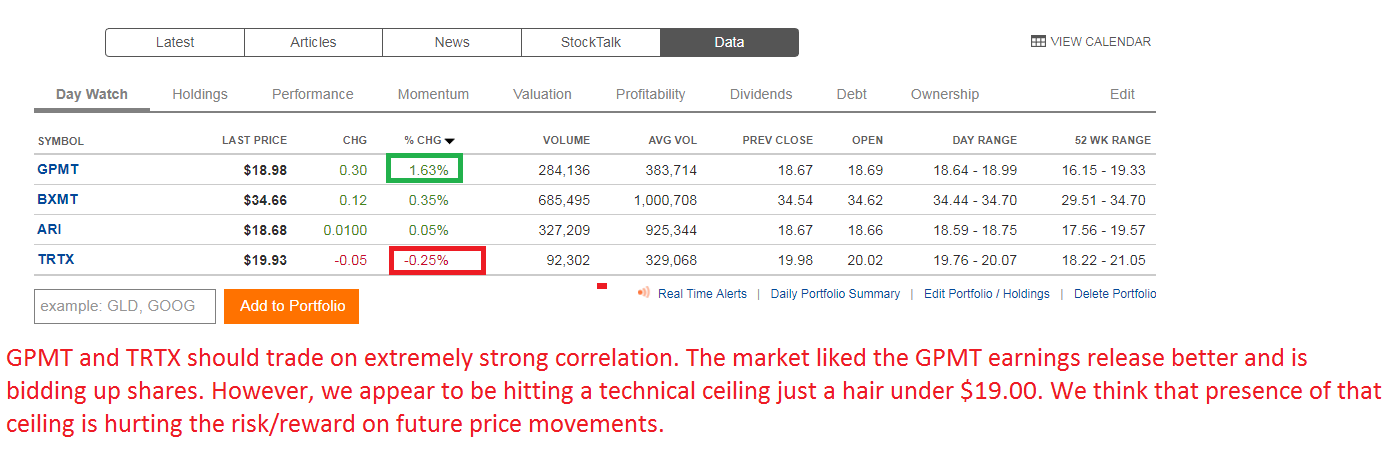

The Granite Point Mortgage Trust earnings name was usually acquired properly. It mixed with their earnings launch to drive GPMT greater on the day relative to their sector friends:

GPMT is the very best performer by a big margin, which leads us to suppose this is likely to be an affordable place to cut back our ranking. Sometimes these traits will proceed, however it’s extra widespread to see them revert.

This article goes to deal a bit with technical elements and a bit with elementary elements. The fundamentals had been a vital a part of the evaluation, however the technicals helped us to choose the exact level.

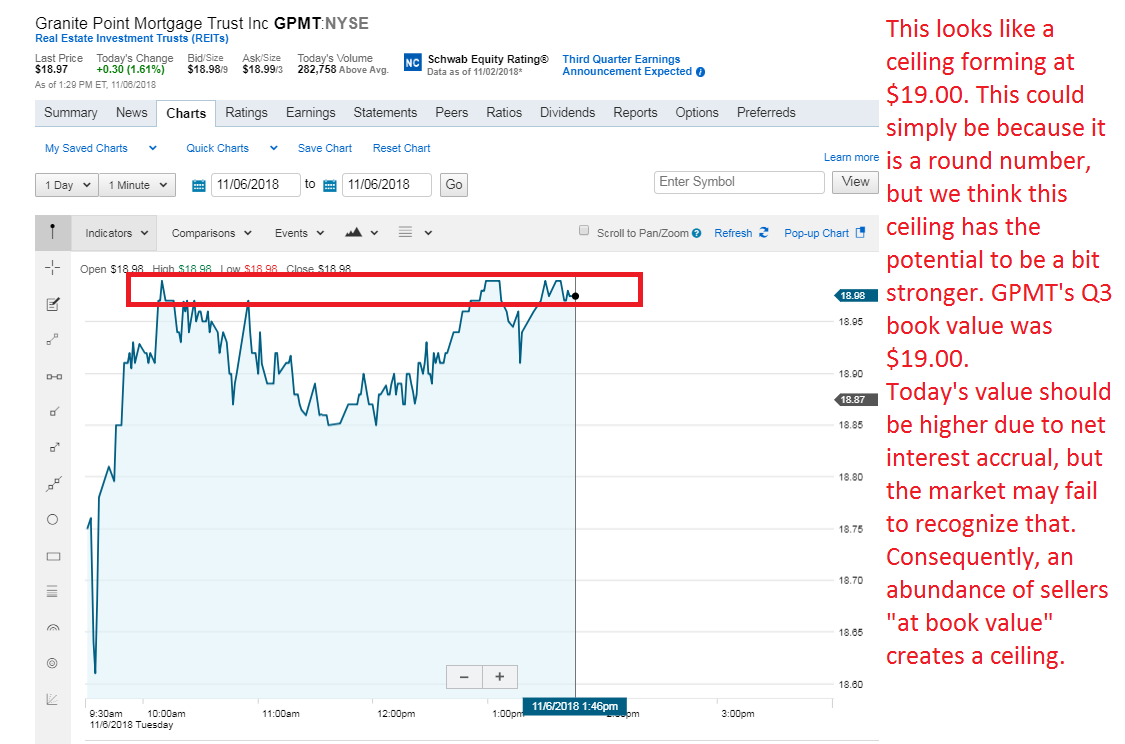

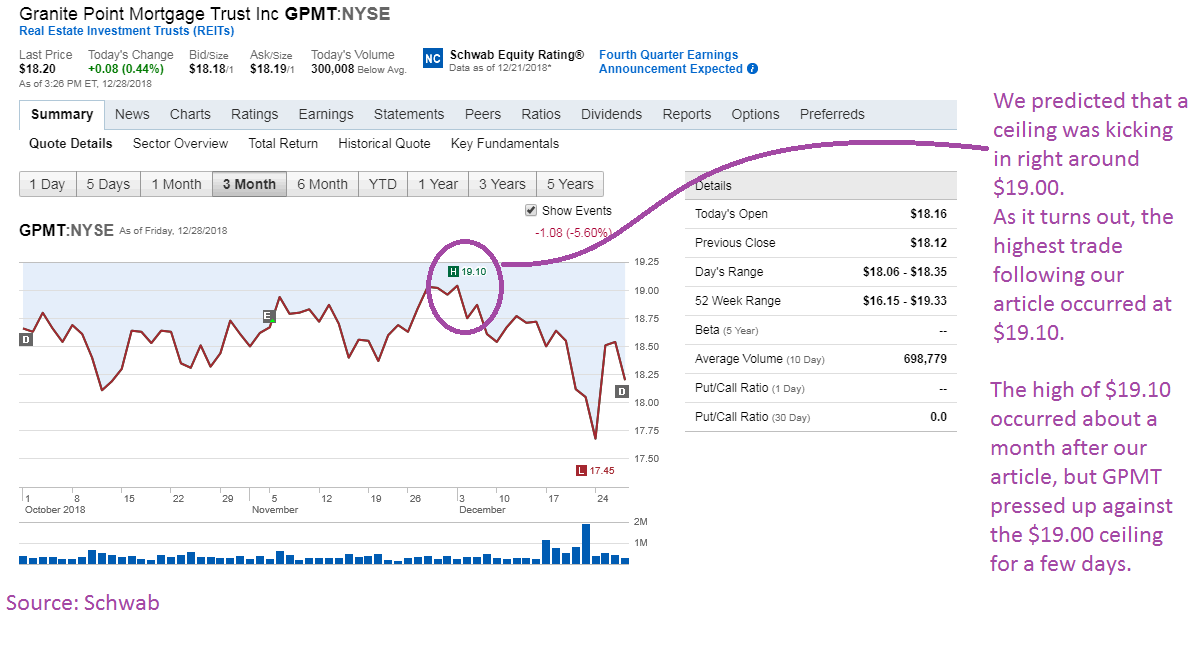

This chart reveals the place the ceiling seems to be forming for GPMT:

When we take a look at a 3-month chart, we discover an analogous pattern:

It seems that’s typically a vendor displaying up every day prepared to promote round $19.00, which makes it more durable for additional positive factors in share worth to happen.

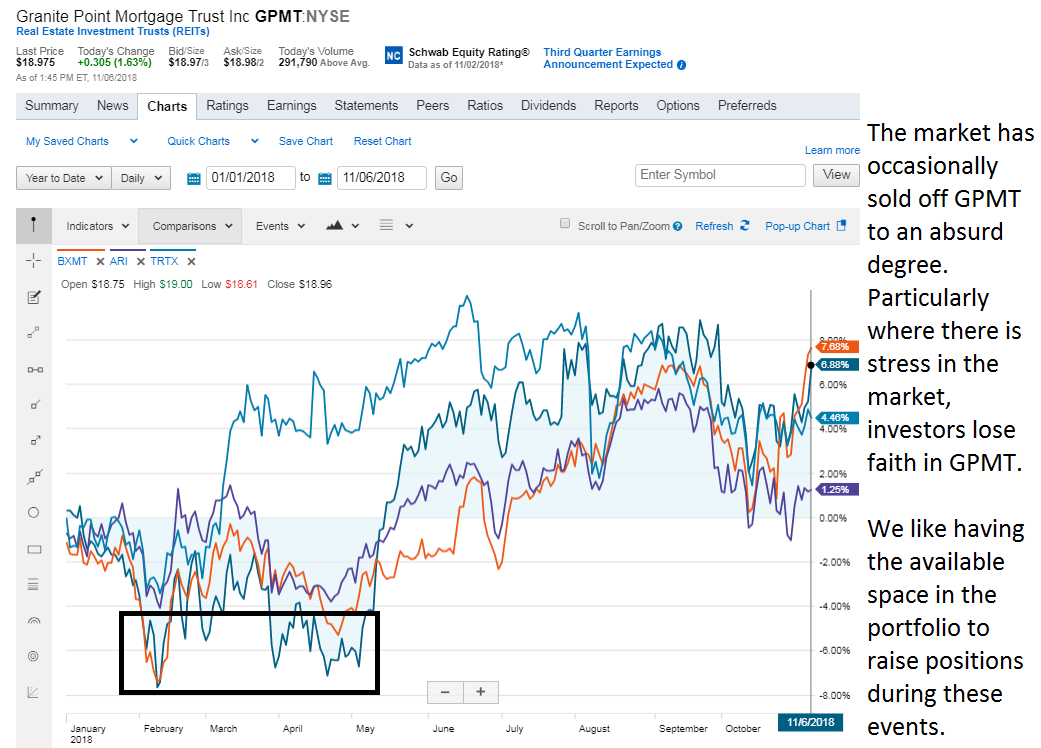

The remaining issue we’re contemplating is that in earlier circumstances the place the market grew to become extra involved in regards to the section or the financial system, we’ve seen GPMT punished to an absurd diploma:

Remember that these 4 REITs maintain very comparable property. We’ve appreciated GPMT as a result of they’ve traded at a cheaper price-to-ebook ratio and since their incentive price kicked in at the next degree of 8% in comparison with the usual 7%.

Price-to-ebook for TPG RE Finance Trust (TRTX) and GPMT is now extraordinarily comparable. Apollo Commercial Real Estate Finance (ARI) and Blackstone Mortgage Trust (BXMT) nonetheless commerce at substantial premiums, however we’re not predicting a healthy premium to ebook as a possible state of affairs because of a slight weakening in fundamentals for future outcomes.

Fundamentals

The earnings name gave us some added perception into fundamentals. Analysts general appear fairly happy with the outcomes, given the outperformance within the share worth. However, we heard a few issues that involved us.

Minor Drag for This autumn 2018 Earnings

The first was administration indicating that their most up-to-date debt issuance will create a drag on fourth-quarter earnings outcomes. This is just the anticipated end result for one quarter, however it nonetheless suggests we may even see damaging revisions to analyst forecasts for This autumn earnings. That might put somewhat damaging stress on the worth within the quick time period. At the least, it could make it harder to create a sustained transfer previous $19.00.

Weakening yield obtainable on Assets Designed for CLOs

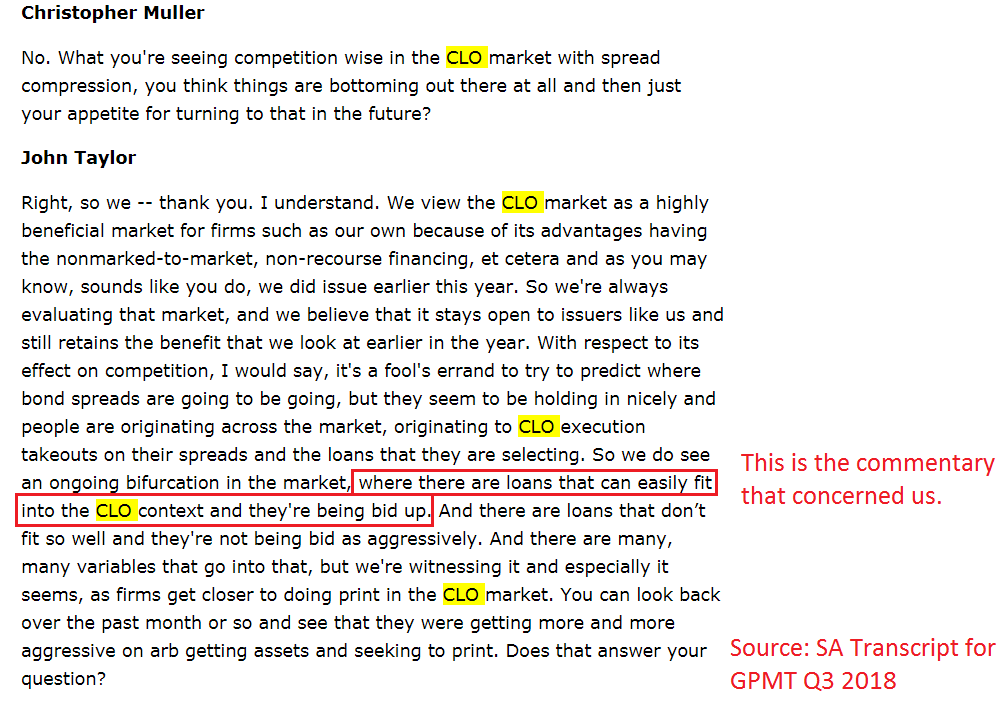

The subsequent problem was probably the most vital one. In our assessment of the earnings launch, we highlighted that we wished to see GPMT shifting to provide further CLO’s to lock within the credit score unfold. The CLO property and liabilities each carry floating charges, however presently, the credit score unfold on CLO’s has been very enticing.

Management addressed that particularly on the earnings name. They indicated that in mortgage origination there was considerably extra competitors for loans that may match properly into the CLO construction. Essentially, different lenders had been specializing in writing loans that may match right into a CLO and consequently the yield on these property was weakening materially.

This is a big problem as a result of we had been in search of GPMT to develop their spreads by this construction, however administration indicated that the competitors there has very not too long ago intensified. Consequently, we can’t fairly anticipate that to be the trail ahead.

Valuation

We’re dropping our worth-to-ebook targets for the robust-purchase and common-purchase scores by about 1% all through the industrial mortgage REITs to replicate this tightening of credit score spreads. The new threshold for GPMT is available in at $18.96.

As it stands GPMT is lower than 2% from their 52-week excessive. Adjusted for dividends, GPMT is setting a brand new 52-week excessive immediately (11/6/2018).

Original Conclusion

For traders who’re holding GPMT for the lengthy-time period, it is a non-problem. It merely implies that we’re not within the splendid shopping for vary. It could be splendid to place new capital to work after some worry works its approach into the market once more. The present dividend degree continues to be lined. We would possibly see development within the subsequent declaration, however it is extremely a lot a “might” scenario at this level. For purchase-and-maintain traders, we’ve entered the “hold” interval. We don’t see a lot cause to be the investor shopping for proper up towards the ceiling, despite the fact that it seems fairly arbitrary.

For traders who’re buying and selling GPMT, we predict it is a affordable time to take some earnings off the desk. We might see a transfer greater with share costs breaking $19.00, however the expectation for decrease This autumn projections makes us doubt that the unreal ceiling is about to interrupt in a sustainable approach. Meanwhile, we face the chance of share costs declining if the market begins to reveal any worry about industrial lending.

We wish to shut out the bulk (not all) of our place so we are able to have the capital obtainable. If GPMT out of the blue dives, we might use the capital to purchase these shares once more. Alternatively, we might hunt for another most well-liked shares or in a number of the different REIT sectors. Currently, our allocation to mortgage REITs is especially excessive as we additionally took positions not too long ago in Dynex Capital (DX), Capstead Mortgage (CMO), and MFA Financial (MFA). We’re seeing very good recoveries presently within the share costs for CMO and MFA main us to some stable unrealized positive factors.

Last evening we indicated that we had been hoping for a bounce within the worth. We referred to the outcomes as a “decent” quarter and didn’t anticipate that it was going to drive the bounce we wished. Despite our studying of the quarter as “decent” different analysts seem to have a extra favorable learn.

Update to Article

Update: Seeking Alpha printed the transcript. We’re displaying the query and reply under. The part in purple was crucial bit of knowledge on the decision:

Update to Article – 12/28/2018

For the general public launch, we’re including one other replace.

The very first thing to replace is the worth chart. This new chart runs by the present date and time:

We’ve positioned a number of trades since then additionally.

Since the preliminary launch, we harvested positive factors in CMO and GPMT. We stay lengthy in MFA and DX.

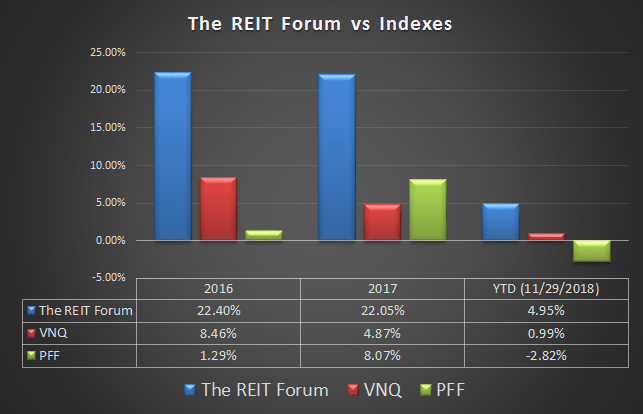

The REIT Forum focuses totally on defensive investments with excessive development potential. It is our goal to seek out high quality investments at a reduction, together with buying and selling alternatives for the extra lively traders. Most of our analysis is on firms which are wonderful investments over the long run.

Disclosure: I’m/we’re lengthy MFA, DX, MFA.PB, ARI.PC,CMO.PE. I wrote this text myself, and it expresses my very own opinions. I’m not receiving compensation for it (aside from from Seeking Alpha). I’ve no enterprise relationship with any firm whose stock is talked about on this article.

[ad_2]