[ad_1]

There is not any Santa. Investors who believed he would experience to the rescue in his sled have been sorely disenchanted this December. Nowhere else has this been as obvious as within the case of AltaGas (OTCPK:ATGFF).

ALA information by YCharts

We had earlier within the 12 months made the robust case for a dividend reduce, and said:

So the reply on the dividend is that if AltaGas can promote belongings at 12X multiples, the dividend is presumably secure till the following recession. If AltaGas realizes that it could actually solely common 10X or much less EBITDA multiples at the moment, the dividend is secure until this Christmas or Thanksgiving, whichever comes first.

AltaGas did make it previous Thanksgiving (each the US and the Canadian ones), however lastly bit the bullet on December 13. We take a look at the brand new plan and inform you whether or not it could actually work.

The plan

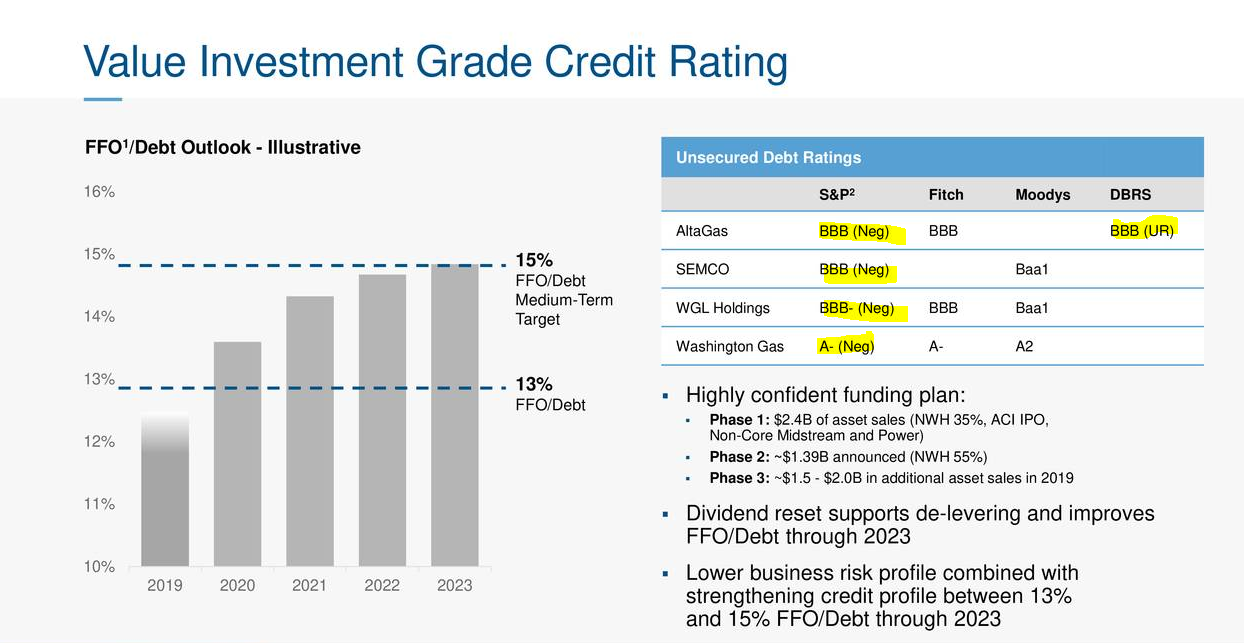

AltaGas had taken a whole lot of time to acknowledge that an organization tottering with 7X debt to EBITDA couldn’t maintain paying 70% of their funds from operations (FFO) in dividends whereas spending one other 200% for development. Any analyst may have instructed them that, however the firm took its candy time acknowledging this. The reduce that did occur was accompanied by three key items of knowledge.

Source: AltaGas presentation

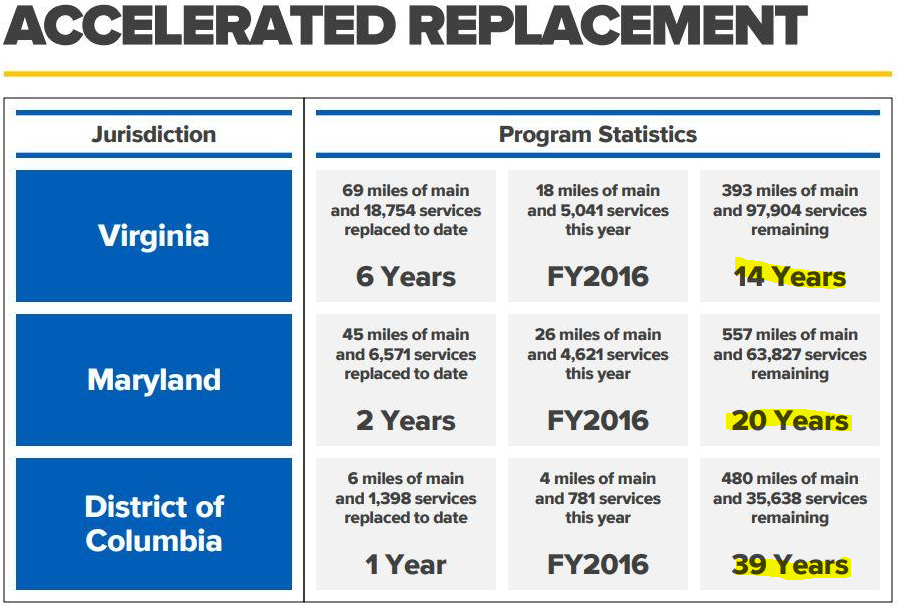

We had maintained that the WGL acquisition would include such a boatload of capex that AltaGas will literally sell every last Canadian asset making an attempt to repair pure fuel pipes in WGL jurisdictions. We can see this within the outdated WGL presentation which has since been taken down.

Source: WGL presentation (link now not obtainable)

The promoting of Northwest Hydro’s remaining stake was one thing we had been fairly certain would occur. AltaGas acquired $1.39 billion for the remaining 55% stake promote. The first 35% sale was for $922 million and extrapolating that valuation will get us $1.45 billion. The decrease worth obtained possible was because of the market turmoil and/or AltaGas’ comparatively determined place. This was just about the one asset left within the AltaGas portfolio that will get very excessive EBITDA multiples so we knew it needed to go to quickly give them respiration room.

AltaGas is focusing on an extra $1.5-$2.0 billion of gross sales in 2019. Those if executed would put whole gross sales at near $6 billion. They paid $9.3 billion for WGL. So our name that they’d promote a cumulative $9.3 billion in belongings over time, doesn’t look so foolish in spite of everything. In hindsight, AltaGas might need carried out a lot better to advise its shareholders to simply promote AltaGas shares and purchase WGL shares as a substitute of going by costly portfolio restructuring.

Where does this go away us

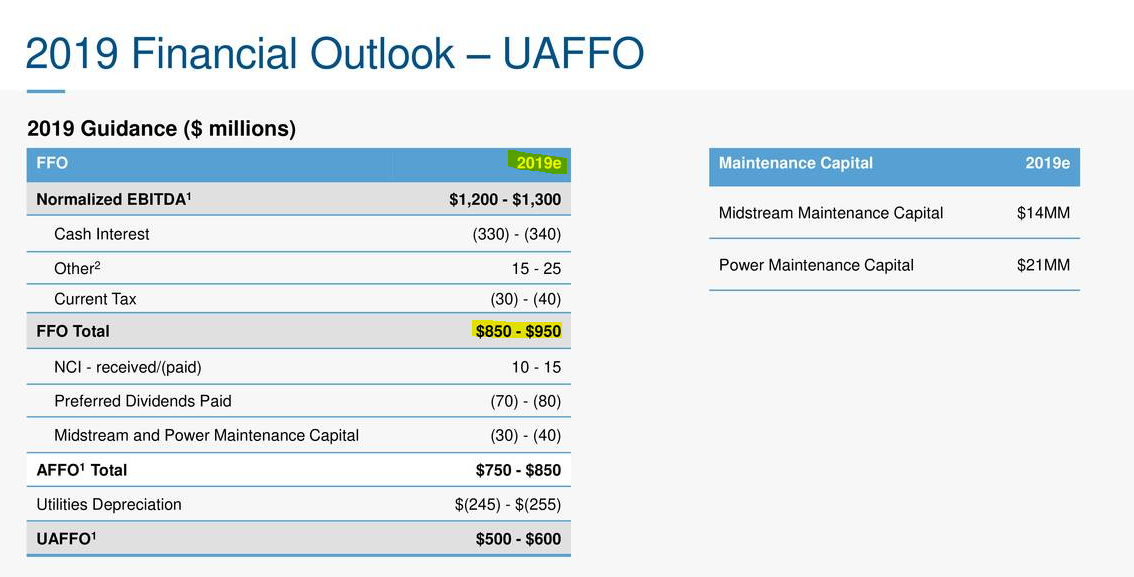

The steerage for 2019 got here in at roughly $900 million for FFO.

Source: AltaGas presentation

We in contrast this to our personal outlook just a few weeks again.

Source: Author estimates from earlier article

Our FFO estimate was fairly good at $875 million. Both our EBITDA and curiosity bills had been larger as we had not accounted for the additional asset gross sales. We had additionally modeled the dividend being maintained, exactly to indicate why it couldn’t be maintained. The reduce clearly frees up some inside capital and reduces debt.

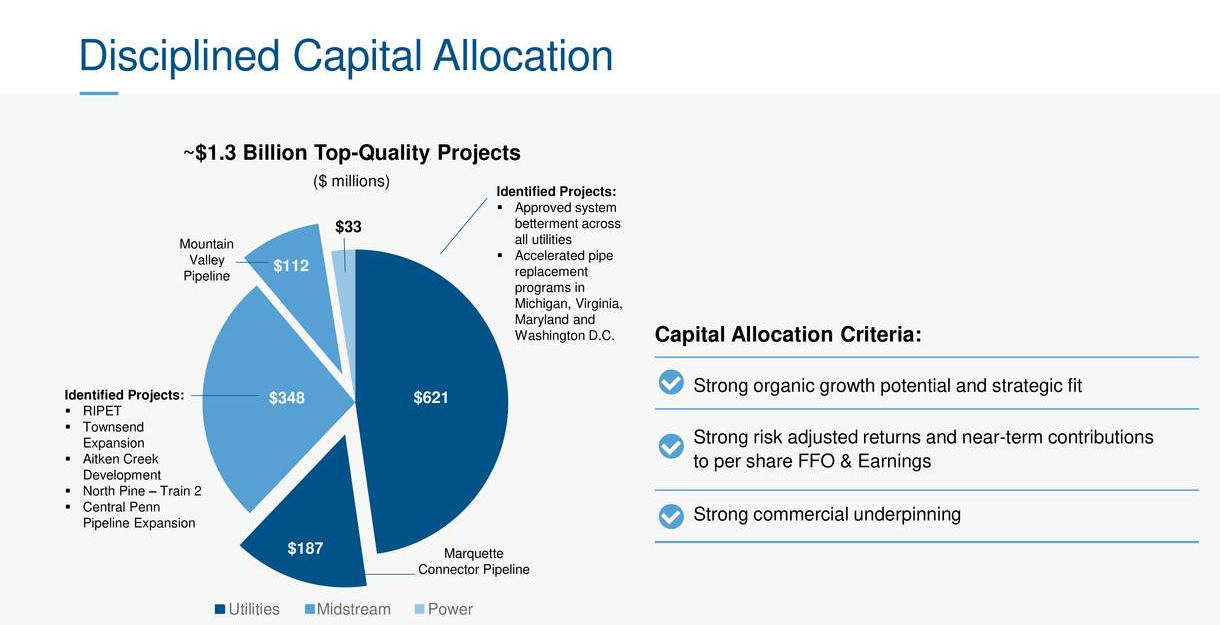

The capital expenditures did are available decrease than anticipated as effectively, as AltaGas was in a position to chop $150 million off this quantity.

Source: AltaGas presentation

One continued difficulty for AltaGas is that the $621 million allotted for Utilities is fairly rigid and can proceed at that or a better fee just about ceaselessly.

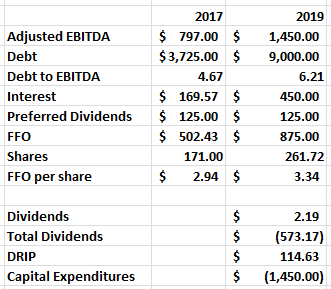

The dividend reset does avoid wasting vital money over time.

Source: AltaGas presentation

We nonetheless suppose that it’ll be very tight to deleverage this successfully as our equation of FFO minus dividends minus capex stays extraordinarily detrimental in 2019 and 2020. The ranking businesses, which previous to this choice had been able to downgrade AltaGas, will now need to assess the dangers of maintaining it as funding grade.

Source: AltaGas presentation

Key dangers for AltaGas

There are 3 key dangers for AltaGas, every with vital implications. The first is a broad primarily based market shutdown, which makes any asset sale at affordable valuation tough. This would make it very arduous to fund the latter a part of the 12 months.

The second is an throughout the board ranking downgrade into junk territory. That is extraordinarily unlikely, and the downgrade will most likely be one step down, maintaining AltaGas above funding grade.

Finally, the speed instances which can be pending will likely be key. Any denials of charges requested for, or a big discount within the last quantity as has happened in the past, could be very detrimental.

Conclusion

AltaGas’ plan can work out. Capital markets have to cooperate for that, although. Our base case is that the bull market is not over and this reset in sentiment is sweet for a much bigger transfer up. Should we be flawed on that, AltaGas must go to a zero dividend.

We didn’t cite the US greenback as a key danger for now, AltaGas’ FFO and capex within the US are about even. That could change down the road and we’ll reassess then. Ultimately, we expect issues will work out and AltaGas will ship nice returns from this level after tax-loss promoting is finished.

Cautious traders on the lookout for a excessive yield publicity to AltaGas, ought to take into account AltaGas’ most well-liked shares sequence E.

These at the moment yield over 8% at present worth based on the latest reset.

With respect to any Series E Shares that stay excellent after the Conversion Date, holders shall be entitled to obtain, as and when declared by the Board of Directors of AltaGas, fastened cumulative preferential money dividends, payable quarterly. The new annual dividend fee relevant to the Series E Shares for the 5-12 months interval commencing on and together with December 31, 2018 to, however excluding, December 31, 2023 will likely be 5.393 p.c, being equal to the sum of the 5-12 months Government of Canada bond yield decided as of at the moment plus 3.17 p.c.

For extra evaluation similar to this, please take into account subscribing to our market service, Wheel of Fortune.

The Wheel of FORTUNE is likely one of the most complete companies, overlaying all asset lessons: frequent’s, most well-liked’s, bonds, choices, currencies, commodities, CEFs, and so on.

Take benefit of our year-end special, which incorporates vital reductions ($924/year), mega poll with prizes, and a two-week free trial.

Check out our monthly review, the place all recommendations since launch seem.

TWoF is a “supermarket of ideas” with emphasis on danger administration and danger-adjusted returns. We stock the “store”’s cabinets, however you resolve what merchandise meet your style.

Take benefit of this rare offer, earlier than charges rise on (and alongside the way in which to) 1/2/2019.

Disclosure: I’m/we’re lengthy ATGFF. I wrote this text myself, and it expresses my very own opinions. I’m not receiving compensation for it (aside from from Seeking Alpha). I’ve no enterprise relationship with any firm whose stock is talked about on this article.

[ad_2]