Crown Castle’s $8.5 Billion Shake-Up: CEO Fired Amid Strategic Overhaul – What Investors Must Know Now!

Crown Castle (NYSE:CCI) has entered a critical transition phase, marked by the abrupt termination of CEO Steven Moskowitz and a major restructuring of its business model. The telecom infrastructure giant is now preparing to offload its fiber and small-cell segments in a sweeping $8.5 billion transaction with EQT and Zayo, aiming to become a pure-play U.S. tower company. Dan Schlanger, the company’s outgoing CFO, has taken the reins as interim CEO while Crown Castle searches for permanent leadership. This leadership change follows growing shareholder pressure and a comprehensive strategic review initiated in response to underperformance and conflicting operating models across business units. While Crown Castle emphasized that the CEO’s dismissal was not due to ethical or financial misconduct, the timing highlights deeper structural challenges within the organization. With the fiber sale set to close by the first half of 2026 and the business entering a leaner operational model, Crown Castle’s strategic pivot and its execution will be crucial in shaping future shareholder value.

Leadership Instability Raises Strategic Execution Risks

Crown Castle’s termination of CEO Steven Moskowitz — less than a year after the previous CEO Jay Brown’s departure — has underscored a period of intense leadership instability. The company has now cycled through two CEOs in under 18 months, driven largely by shareholder activism, notably from Elliott Investment Management and former CEO Ted Miller. These stakeholders publicly criticized Crown Castle’s approach to its fiber strategy, calling for a breakup of the business and new board leadership. The Board’s appointment of outgoing CFO Dan Schlanger as interim CEO, followed by the announcement that Sunit Patel will assume CFO responsibilities in April 2025, has introduced operational uncertainty at a time when Crown Castle is navigating one of the largest divestitures in its history. The executive vacuum may challenge continuity in execution, particularly during the fiber and small-cell transaction process, the shift to a pure-play tower model, and the transition of key corporate functions. Additionally, Schlanger is expected to assume a new role as Chief Transformation Officer after a permanent CEO is hired, signaling further internal reorganization. The leadership transition comes at a critical time, as the company attempts to reorient its operational focus toward free cash flow generation and tighter capital allocation. While the board emphasized that the CEO's firing was not related to any performance or ethical issues, the persistent leadership churn may undermine investor confidence in the company's ability to deliver on its newly defined objectives and manage relationships with carriers and regulators during the transition.

Strategic Divestiture Of Fiber & Small Cells Reflects Operational Misalignment

The sale of Crown Castle’s fiber and small-cell segments to EQT and Zayo reflects a strategic realignment following an in-depth operational and financial review of the company’s asset base. The fiber segment, with over 90,000 route miles of high-strand count fiber, had long been seen as a mismatch with the company’s traditional tower-focused operations due to its distinct business model, customer base, and operating requirements. Although small cells share overlapping market drivers with towers, Crown Castle determined that the differences in operational capabilities outweighed potential synergies. The $8.5 billion deal — expected to close in the first half of 2026 — concludes a review process that began in late 2023 and will see Crown Castle become the only public U.S. tower pure-play. Management emphasized that this structure would enhance shareholder value by sharpening operational focus, repaying debt, and executing share repurchases. However, the sale comes at a cost. A $5 billion goodwill impairment was recognized in 2024, stemming from deferred small cell expansion plans and higher capital costs, leaving no remaining goodwill on the fiber reporting segment. While the company expects the fiber business to generate around $250 million in free cash flow in 2025 as a discontinued operation, this transition could affect Crown Castle’s short-term financial disclosures and comparability. Furthermore, given the anticipated 12–15 month regulatory review process, there remains considerable execution risk in transferring state-level agreements and ensuring seamless business continuity during the handover to EQT and Zayo.

Sprint Churn & Flat Organic Growth Pressure Core Business

Crown Castle’s core tower business is navigating a challenging growth environment exacerbated by Sprint-related churn and limited upside in new leasing activity. In 2025, the company expects to deliver 4.5% organic growth in its tower segment, excluding Sprint cancellations. However, this growth will be offset by approximately $205 million in Sprint churn hitting in January, which will weigh heavily on site rental revenues. Even looking beyond 2025, Crown Castle anticipates residual Sprint churn of around $20 million annually between 2026 and 2034, which will continue to impact its financials. Excluding Sprint, the company expects less than 1% churn in 2025 and forecasts longer-term churn of 0.5% to 1.5%, indicating an overall deceleration in lease growth. Although carriers continue deploying C-band spectrum to support 5G rollouts, most of the activity consists of overlays rather than greenfield expansion, limiting revenue upside. The company’s $110 million in projected core leasing activity for 2025 mirrors 2024 levels, with few signs of acceleration. Crown Castle also noted that while application volumes have increased modestly, this has not materially shifted its growth outlook. The relatively flat growth profile, combined with a constrained leasing environment and pricing pressure from comprehensive master lease agreements, may limit the company's ability to quickly scale its AFFO. Moreover, Crown Castle is undertaking modest CapEx increases in 2025, particularly around securing land under its towers, a move aimed at long-term margin enhancement but unlikely to produce immediate financial gains. Overall, the organic growth trajectory remains pressured in the near term.

Capital Allocation Reset Amid Dividend Cut & Buyback Uncertainty

Following the fiber and small-cell divestiture, Crown Castle plans to overhaul its capital allocation strategy, prioritizing free cash flow generation, balance sheet repair, and targeted capital returns. The company has announced that it will reduce its annual dividend to approximately $4.25 per share in Q2 2025, aligning the payout with 75% to 80% of anticipated AFFO, excluding amortization of prepaid rent. This marks a significant departure from its historically generous dividend policy and signals a shift toward disciplined capital stewardship. Simultaneously, Crown Castle plans to repurchase up to $3 billion in shares post-closing, though management has emphasized that decisions regarding the scale and timing of buybacks will be evaluated quarterly through multiple layers of internal and board-level capital committees. The company also intends to use a substantial portion of the transaction proceeds — potentially around $6 billion — to reduce debt and maintain an investment-grade credit rating with a leverage target of 6.0x to 6.5x. However, there are risks associated with this framework. Key financial metrics like AFFO and EBITDA for 2025 exclude the fiber segment but do not yet reflect the full impact of post-sale cash deployment. Advisory costs tied to the strategic review and proxy battle already amounted to $40 million in 2024, and further execution costs may arise. Additionally, share repurchases are contingent on market conditions and board approval, while the reduced dividend could disappoint income-focused investors. With multiple moving parts, Crown Castle’s capital strategy remains fluid and potentially volatile until the fiber transaction closes and the business model fully resets.

Final Thoughts

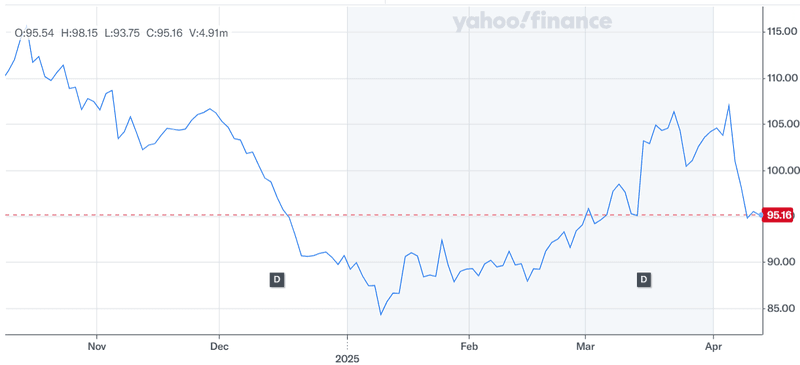

Source: Yahoo Finance

Crown Castle’s stock has been extremely volatile over the past 6 months as shown in the above chart. The management’s decision to sell its fiber and small-cell businesses and become a focused tower operator represents a pivotal shift in its strategic direction. While the company aims to streamline operations, improve margins, and deliver long-term shareholder value, this transformation comes with significant execution risk. The CEO transition, ongoing Sprint churn, flat leasing growth, and restructured capital allocation strategy all represent material uncertainties. Furthermore, with a large-scale divestiture still pending regulatory approval, near-term financial visibility is limited. As Crown Castle transitions into a pure-play tower company, it is difficult to determine the long-term potential of the streamlined business model especially against the transitional challenges and short-term disruptions likely to persist through 2026. Hence, we believe that Crown Castle’s stock is best avoided at current levels and bottom-fishers should stay far away from the company despite its current lows.