Rick Rieder and Russ Brownback argue that slowing development, peaking inflation, and tightening monetary situations mix to make a robust case for a Fed coverage price mountaineering pause in early 2019.

If you’ve got ever endeavored to furnish a brand new dwelling, chances are high you’ve got confronted the daunting process of putting in a big wall fixture, maybe a mirror or portray. The dreaded course of entails in depth choreography with multidimensional measurements, entry to the requisite instruments, and a willingness to embrace the fact of quite a few unsuccessful makes an attempt and unpleasant holes in your lounge wall. Eventually, after wrestling your fixture onto its hook, that you must step again from the wall for a greater perspective – a pause in your course of to make sure that your laborious endeavor has achieved an optimum end result. To us, the Federal Reserve’s ongoing efforts to hunt coverage neutrality are a equally painstaking and imprecise exercise, and that latest market tumult, alongside a deceleration in development and inflation, offers enough causes for the Fed to step again and ponder their efforts up to now earlier than appearing additional.

The evolution in international liquidity

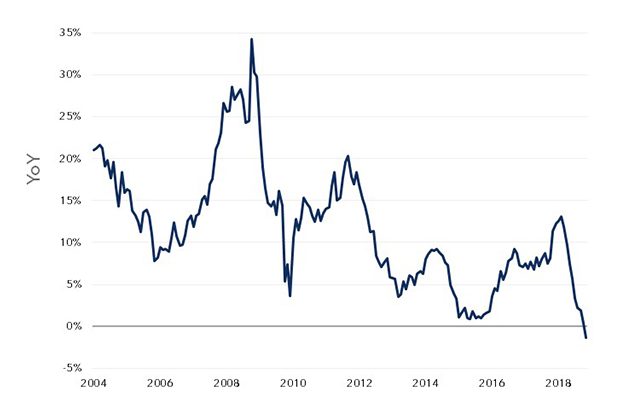

Conventional knowledge says that 2018’s market contagion is unjustified relative to the de minimis absolute degree of cyclical coverage tightening relative to historical past. To us, it isn’t absolutely the degree of tightening that is inflicting consternation, however the stark distinction of at the moment’s combination coverage posture versus this time final yr. In the fourth quarter of 2017, international liquidity was rising at its quickest tempo ever: developed market actual coverage charges have been destructive, China was having fun with the tail-end of a multi-year credit score explosion, and the U.S. was set to unleash highly effective fiscal stimulus, a worldwide coverage cocktail that was maybe amongst essentially the most supportive postures of latest years for danger property (see graph).

Sources: Bloomberg, JP Morgan, BlackRock; information as of December 10, 2018

Today, international liquidity is in regular decline, U.S. actual coverage charges are the best ranges in nearly a decade, China is endeavoring to deleverage, and U.S. fiscal stimulus is ready to abate. Moreover, U.S. Treasury provide has doubled from final yr. This sudden coverage U-turn is making a two-fold systemic shock to the monetary financial system: the newfound availability of optimistic real-yielding risk-free securities, together with the considerably greater low cost charges that have to be utilized to dangerous money flows, are crowding traders out of dangerous property.

Many monetary prognosticators stubbornly adhere to a forecast of great extra coverage tightening, regardless that markets are more and more loath to cost in that hawkish path. At this level, no less than, we agree steadfastly with the markets and maintain the view that we’re on the doorstep of coverage neutrality and a Fed pivot towards a extra symmetric, and data-dependent, ahead coverage path is at hand.

Decelerating international development is already obvious in each high-frequency macro information and messaging from globally uncovered companies, as evidenced by sharply decelerating income, contracting margins and slower money circulate development. More importantly, U.S. inflation has struggled to realize the Fed’s desired goal, as secular inflationary headwinds stay firmly entrenched. For occasion, ubiquitous technological innovation is enabling profound manufacturing efficiencies throughout each sector of the financial system, from vitality to retail. Further, the persevering with evolution of cloud computing and information storage is driving a shift out of conventional company capital expenditure and into analysis and improvement, as firms race to construct out machine learning and synthetic intelligence capabilities, or danger being left behind by simpler and decrease value opponents. We are nonetheless within the early phases of those generational deflationary traits.

Are rising wages a spur to greater costs?

Meanwhile, considerable ongoing debate exists in regards to the diploma to which accelerating wage development will catalyze inflation because it typically has traditionally – a relationship we predict has damaged down. Counter to historic precedent, rising wages are in actual fact paradoxically disinflationary at the moment. The relentless assault on company pricing energy by info symmetry (assume Amazon and consumer opinions) is forcing companies to soak up rising wages by means of narrower profit margins, as an alternative of pursuing greater costs. As money flows are squeezed, animal spirits are dampened and economy-wide exercise slows. Further, at the moment’s wage earners have a demonstrable proclivity to avoid wasting their rising wage windfall reasonably than divert it to incremental consumption. In whole, rising wages are a virtuous societal phenomenon reasonably than a harbinger of inflation; a supply of stabilization for an actual financial system that’s flirting with systemic capability constraints. Therefore, wage positive aspects must be embraced by coverage makers at the moment reasonably than extinguished.

Further, the connection between dangerous property and inflation (or real rates) is neither linear nor exponential, however parabolic. Risky asset valuations get damage when inflation and actual charges are both too low or too excessive. At the apex of that parabola is an optimum situation the place danger valuations flourish – and our demographic fashions of potential development and inflation recommend that that apex is shifting to the left (in different phrases, danger property flourish now at a decrease degree of inflation and actual charges than in many years previous). Most probably, the optimum risk-free price has already been achieved, as evidenced by danger property’ struggles throughout 2018’s “year of adjustment,” and incremental will increase from listed here are unwarranted. Thus, with the cyclical enhance in charges now accomplished, portfolio steadiness might be restored anew and length can as soon as once more be employed as an efficient hedge for danger, making “risk less risky.”

Investment implications

This new equilibrium price plateau is way greater than something skilled in the course of the post-crisis period. As a consequence, one in all our favourite regime identification instruments is now flashing a extra cautious sign. For a number of years the persistence of ultra-low charges meant that discounting companies’ free money circulate utilizing their value of financing revealed inherent cheapness down the capital stack. Today’s greater charges and spreads have brought about a lot of that “value” down the capital stack to evaporate, and we’re duly adjusting our portfolios.

In 2018, lengthy Treasuries posted a destructive return, inflicting balanced portfolios of shares and bonds to expertise their solely yr of under-performance versus money in no less than half a century, outdoors of outright recessionary durations. The regime shift in dangerous versus risk-free correlation that we anticipate in 2019 can’t be understated: it means a portfolio of high-quality European and Japanese property swapped again to U.S. {dollars}, Agency mortgage-backed securities and modest allocations to pick EM and credit score, might work effectively within the yr forward, if generously hedged with U.S. length.

This post initially appeared on the BlackRock Blog