Targa Resources Corp. (NYSE:TRGP) has recently been in the spotlight following reports of rebuffing an informal takeover interest from larger rival Williams Companies. Although Williams denied extending an official offer, the rumors underscore a possible demand for consolidation in the pipeline industry. Targa, with its $32 billion market capitalization, operates primarily in the midstream energy sector, focusing on natural gas gathering, processing, and transportation. The company has proven to be a solid player in a space where larger rivals are constantly seeking opportunities for growth. Let us take a closer look at Targa Resources and explore the key growth drivers that make Targa Resources an appealing target for strategic acquirers in the ever-consolidating midstream energy industry.

Expansive Infrastructure and Integrated Services

One of the primary reasons why Targa Resources is an attractive acquisition target is its expansive infrastructure network and integrated services across the natural gas value chain. Targa owns and operates natural gas gathering and processing facilities, fractionation plants, and pipelines that transport natural gas and natural gas liquids (NGLs) to end markets. The company has strategically located assets in prolific energy basins, including the Permian Basin, which is the most productive oil and gas region in the U.S. By offering integrated services that cover the entire spectrum from wellhead to market, Targa provides significant value to upstream oil and gas producers. This integrated service model allows Targa to capture more margin from each unit of gas it processes, enhancing its profitability. For a strategic acquirer, this infrastructure and the services it provides would be highly complementary to their existing operations, enabling synergies such as improved transportation efficiency, expanded customer bases, and enhanced bargaining power in pricing contracts. Moreover, the capital-intensive nature of Targa’s operations and the high barriers to entry in building new pipelines make it an appealing asset for larger players looking to grow through acquisitions rather than developing new infrastructure from scratch. The company’s ability to secure long-term contracts with customers further solidifies its revenue base, providing stability and predictability in cash flows, which are highly desirable in the volatile energy market.

Strategic Presence in High-Growth Areas

Targa’s strategic presence in high-growth energy basins, particularly the Permian Basin, is a crucial factor that makes it an attractive acquisition target. The Permian Basin is the most prolific oil-producing region in the U.S., and its natural gas production is also on the rise. Targa has significant infrastructure in place to gather, process, and transport natural gas from this region, making it a key player in the midstream segment of the energy supply chain. The company’s ability to handle increasing production volumes from the Permian Basin positions it well to benefit from future growth in U.S. natural gas output. Furthermore, Targa has made strategic acquisitions in recent years, such as the purchase of Lucid Energy in the Delaware Basin, further strengthening its presence in high-activity areas. These acquisitions have not only expanded Targa’s asset base but also diversified its revenue streams by increasing its customer base and exposure to different segments of the energy market. For a strategic acquirer, Targa’s strong foothold in the Permian and Delaware Basins represents a valuable opportunity to gain access to high-growth areas without having to invest in building new infrastructure from the ground up. Moreover, Targa’s ability to efficiently scale its operations in response to rising production volumes offers potential synergies for a larger company looking to expand its midstream capabilities. The company’s proximity to major production zones also provides it with a competitive advantage in securing long-term contracts with producers, ensuring a stable and growing revenue base.

Strong Capital Return Program and Financial Stability

Targa’s robust capital return program is another factor that makes it an appealing acquisition target. The company has consistently demonstrated its commitment to returning capital to shareholders through both dividend payouts and share buybacks. This capital return strategy not only reflects Targa’s strong cash flow generation capabilities but also signals to potential acquirers that the company is financially stable and well-managed. A significant aspect of Targa's capital return program is its substantial share repurchase authorization, which highlights management’s confidence in the company’s future growth prospects. This financial strength is further bolstered by Targa’s disciplined approach to debt management, with a focus on maintaining a healthy balance sheet. The company’s leverage ratio remains within acceptable industry standards, and its strong free cash flow allows it to fund both capital expenditures for growth projects and shareholder returns. For an acquirer, Targa’s ability to generate consistent cash flow even in periods of market volatility provides a measure of security. Additionally, the ongoing capital return program could be seen as an opportunity to optimize capital allocation post-acquisition, either by continuing to reward shareholders or by reallocating funds towards new growth initiatives. Overall, Targa’s financial stability and shareholder-friendly capital return program enhance its appeal to strategic acquirers who prioritize both growth and financial prudence.

Conclusion

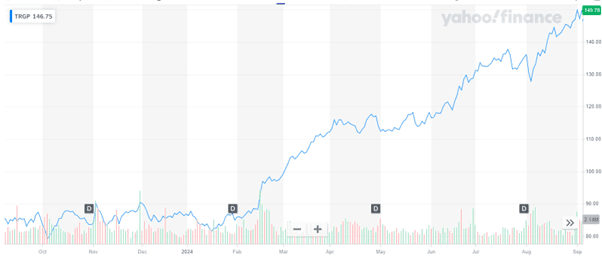

Source: Yahoo Finance

As a stock, Targa Resources, has performed formidably in the past year, nearly doubling in value and also providing timely quarterly dividends. After this runup, its stock is trading at an LTM EV/ Revenue multiple of 2.92x and an LTM EV/ EBIT multiple of 19.74x which still appears fair. We believe that Targa Resources presents a compelling case as an acquisition target for strategic acquirers in the midstream energy sector. Its expansive infrastructure network, strong capital return program, and strategic presence in high-growth areas make it a valuable asset for any company looking to expand its footprint in the natural gas market. However, potential acquirers must also weigh the challenges that come with owning and operating large-scale pipeline infrastructure, including regulatory hurdles, environmental risks, and the ongoing need for capital investment. While the company's strong financial performance and strategic positioning make it an attractive target, whether an actual acquisition will go through or not is the question as there are no major rumors of acquirers circling the company after Williams’ denial of bidding for Targa. Whether an acquisition target or not, we believe that Targa Resources is a fundamentally solid midstream player and could be a good investment for oil & gas investors.