The Fed’s Triple-Handed Ambiguity: When A Forecast Is A Target And An Indicator

[ad_1]

Having seen the mischief that his miscommunication has wrought up to now, Fed Chairman Powell should be trying ahead to the fact that he may have the microphone in his palms after each FOMC assembly in 2019, with combined emotions. President Trump, Chairman Powell’s colleagues and Mr Market could also be much less passionate about this prospect.

President Truman needed a one-handed economist. The Volcker Fed had a one-handed Chairman. President Trump allegedly needs to dismember the present Fed Chairman. Chairman Powell could seem to have just one hand, however the Federal Reserve really has three-handed economists in follow! Chairman Powell’s shaky hand continues to level within the path of a “gradual” normalization on auto-pilot. Mr Market nonetheless not too long ago instructed Chairman Powell that he wants extra palms on deck asap. It’s due to this fact time for a delicate change of palms women and gents.

Mr Market has not but famous that the Fed the truth is has three palms. Three palms and two mandates make for much more mischief than Mr Market might have imagined is feasible. If the Fed has received it improper on its present auto pilot setting, then greater than only a recession would be the consequence. Fed independence is now in danger greater than it has ever been. Voter-friendly Congressmen, with a watch to the subsequent Presidential election, will throw the Fed below the bus for faithfully following its twin mandate with consummate ease, if the economic system goes south from right here.

The Fed has didn’t name any of the final recessions aside from the one Chairman Volcker intentionally created. Neither has a Fed Chairman been fired for getting it improper. With no danger of punishment, there isn’t any incentive to get it proper. Unless Chairman Powell sees the identical scenario creating as Volcker did, which should be a great distance off even whether it is coming, the present disconnect solely serves to affirm and strengthen Mr Market’s convictions, and thereby undermine the credibility of Powell. Indeed Powell has already discounted the Volcker consequence, along with his intuitive assertion that globalization has structurally depressed inflation.

Maybe in equity, Chairman Powell’s present hang-up is that the present breakdown of the worldwide buying and selling system will reignite the previous Volcker period’s inflation dynamics. If that is so, nonetheless, the present efficiency of power and commodity costs ought to persuade Powell that this danger will not be elevating however is the truth is falling. More doubtless, Powell like all his colleagues is solely scared by the dimensions of the Fed’s stability sheet; and within the absence of a disaster lacks the context and motivation for sustaining it. Creating a disaster is due to this fact his raison d’etre, which he denies with phrases however does along with his actions knowingly or in any other case.

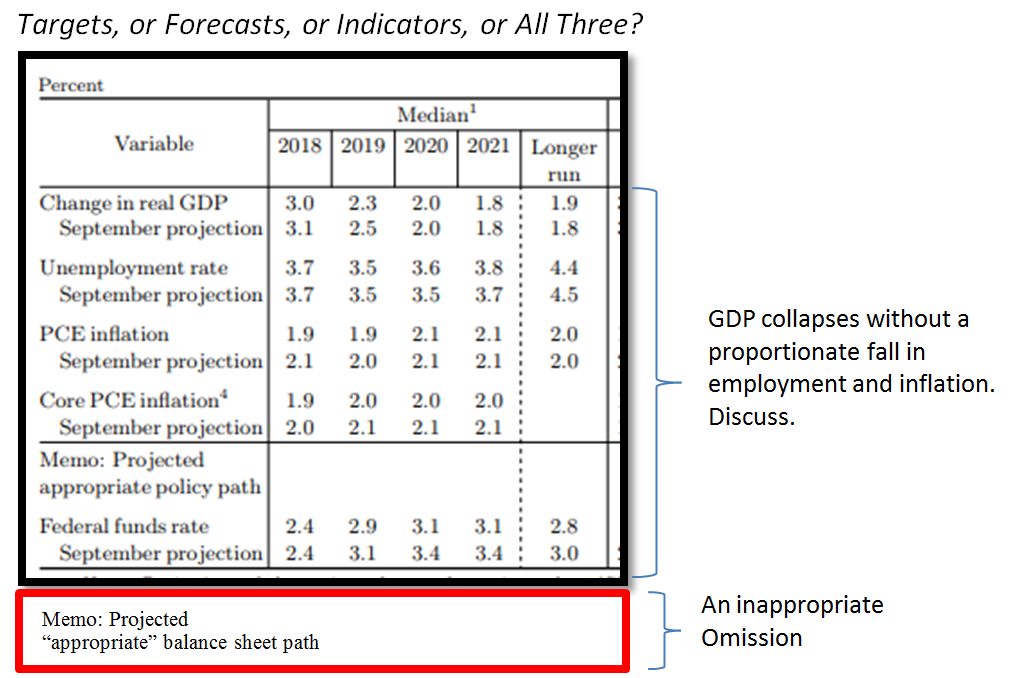

(Source: Federal Reserve Board Staff Forecasts)

Mr Market has seemed on the newest Hawkish FOMC statement with accompanying staff projections and assumed that the Fed will the truth is create a recession circa Presidential election time. It’s a good assumption as we will see.

Missing from the employees projections is a forecast of the Fed’s stability sheet over the forecast interval. The complete forecast web page blissfully omits the very actual proven fact that the Fed is shrinking its stability sheet, or maybe it’s factored into the opposite knowledge on the web page (unlikely). If included, it will present the stability sheet on auto pilot, shrinking at $50 Billion a month. That’s $600 billion a 12 months and $1.2 Trillion between now and 2021, hardly chump change even earlier than one understands that it has been leveraged up a number of occasions because it was first QE injected. It took roughly ten years to get the stability sheet as much as round $4 Trillion. It will take lower than half of that point to unwind it on the present fee of decay in an economic system that’s already decelerating. This asymmetry is far more necessary than the Fed’s alleged symmetrical inflation goal.

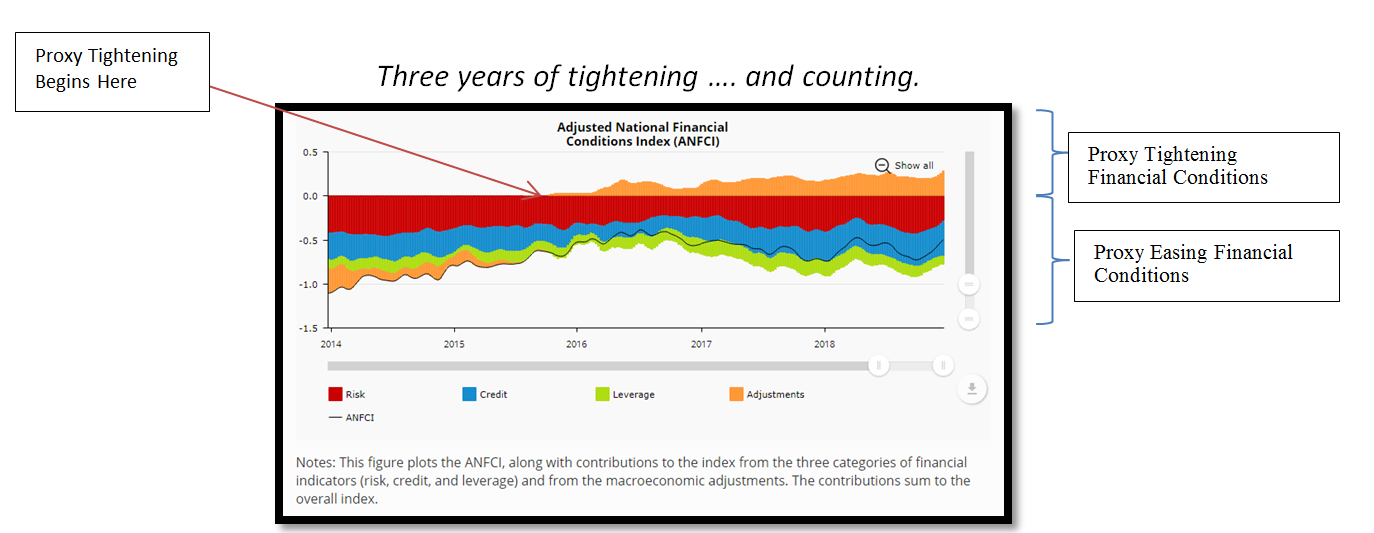

(Source: Chicago Fed)

The Chicago Fed’s Adjusted National Financial Conditions Index (ANFCI) neatly illustrates how financial situations have been getting tighter since late 2015. It additionally reveals how issues are getting even tighter of late. It is helpful to make use of the “Adjustments” space of the ANFCI because the proxy for the diploma of economic situations tightening. Using this proxy it may be proven that monetary situations have tightened because the Fed initially started elevating rates of interest, reducing reserves and latterly beginning to shrink its stability sheet.

Balance sheet withdrawal has a negatively leveraged financial impression when it comes to each time and worth, simply because it gave a leveraged increase on the way in which in. That was the entire level of it within the first place or so we have been instructed by Chairman Bernanke on the time. The Fed has very audibly and transparently pre-committed to tighten financial coverage, by nature of auto-pilot stability sheet discount. As Chairman Powell reminded on the final FOMC : “I think that the runoff of the balance sheet has been smooth and has served its purpose,” and “I don’t see us changing that.” This steering is on auto-pilot and has been fired and forgotten by the Chairman, though its impacts are clearly being felt in home and world capital markets.

The Fed’s little stability sheet omission critically removes some crucial context for the entire forecast. If this have been to be included, it will present that financial coverage has been tightening and can proceed to take action because the stability sheet shrinks. Combining this with the rate of interest enhance projections proven within the Fed forecast is a considerably larger financial coverage tightening than preliminary impressions understand. No surprise then that forecast GDP collapses from 2018 to 2019! In actuality, GDP could collapse much more below the leveraged impression of stability sheet withdrawal magnified with larger rates of interest. It’s exhausting to see why inflation and employment wouldn’t additionally collapse with this tightening of financial coverage though the Fed forecast them to stay unchanged.

Chairman Powell, alternatively, believes that he’s projecting and dealing in direction of a traditional American economic system in time for the subsequent Presidential election. He is even on report for promising to ship an prolonged enterprise cycle with no inflation all the way in which to the subsequent election. Thus far, he has delivered his promise within the type of the most recent FOMC forecasts. Nothing in need of a recession, within the type of rising unemployment and falling inflation exterior the boundaries of the most recent Fed forecasts, between now and 2020 would allegedly change his conviction. If Chairman Powell thinks that he can deflate danger asset costs in such a brief area of time between now and 2021 with out triggering a monetary disaster, he’s overly optimistic at finest and delusional at worst.

It took about ten years of QE to create this case. It ought to due to this fact be unwound over a time frame no shorter in length and ideally of a similar-to-much-longer length since financial progress and inflation are subdued. At the outset, it was not clear how lengthy it will take to get into this case, so it’s definitely not clear how lengthy it can take to unwind, therefore the necessity for the additional warning which is at the moment missing.

Chairman Powell will not be being “gradual” in any respect; he’s being dangerously “swift”. Firing after which forgetting about an untested program to shrink an unprecedentedly enormous stability sheet is a priority. It demonstrates both a lack of knowledge of the financial circumstances or a refusal to take duty for the result. Looked at positively, it might present that moderately than take dangers along with his poor judgement, the Chairman has determined to enter auto-pilot mode with a lot much less dramatic penalties. Raising rates of interest is the ultimate incremental straw because the harm is already carried out however completely in step with this profile that seeks automated moderately customized options and insurance policies.

If 2019 is a rerun of 2018, the optimistic US rate of interest differential will once more suck-in world capital, thereby weakening the worldwide economic system additional and offering a tailwind to the home US economic system. The Fed apparently doesn’t assume this, nonetheless, because it has forecast an enormous fall in GDP in 2019, which curiously seems to haven’t any proportionate impression on both inflation or employment. This little anomaly and its important implications might be defined shortly.

Chairman Powell, true to his Congressional mandates, is thus doing his job on the expense of the worldwide economic system. Whilst the Fed pays lip-service to the worldwide economic system and its headwinds, in follow it has not factored them in. Why ought to it when world commerce is barely about 12% of US GDP? The present deal with the rampant US shopper, who’s 70% of GDP, is clearly the precedence.

The purpose to deal with the worldwide economic system is one in every of monetary stability danger. If the worldwide economic system implodes as a result of it’s starved of US Dollars, then international monetary establishments with Dollar property and liabilities will fail. The danger to the US economic system then comes by its publicity to those world establishments. Balance sheet discount alone, is ravenous the worldwide economic system of US Dollars. Attracting what Dollars are left again to America, with larger rates of interest, is simply the ultimate nail within the coffin for the worldwide economic system. A full blown commerce warfare would simply make the scenario even worse.

(Source: Seeking Alpha)

The July report on this sequence famous that Chairman Powell and his group confirmed the inertial bias in direction of inflation combating, regardless of their protestations to be pursuing a symmetrical inflation goal. The Fed talks a great sport on letting inflation overshoot, but its actions present a horror of this ever occurring. The FOMC seems to have had a horror on the Trump fiscal stimulus and its tailwind in 2017. This grew to become a self-reinforcing conviction as labor markets tightened to new lows and headline inflation started to tick up in mid-2018. Despite the FOMC’s horror, nonetheless, this by no means actually kicked in to the Dot Plots and different forecasts. The inconsistency of habits and steering is a attribute of the Fed that more and more is undermining its credibility of dedication. As we will see, this inconsistency is a systemic design of the Fed. It thus undermines itself by design!

(Source: Euronomist)

This bias might be considered because the Fed’s failure to persistently distinguish between inflation as an financial indicator on one hand, a forecast on the opposite after which a mandated goal on the Fed’s mysterious invisible third hand. This is the truth is the essence of Fed steering.

Furthermore, in reacting to the habits of Mr Market, the Fed clearly switches between these three distinctions and palms. The identical inconsistency precept might be utilized to the complete employment mandate, though that is clearly a lesser precedence for the Fed proper now. The mixture of possible situations from two mandates and three palms might be fairly complicated (intentionally so) for Mr Market and fairly helpful to the Fed.

This failure to persistently interpret the twin mandates is a critical institutional failing of the Fed that Congress needs to be made conscious of and may examine. The very first thing to do needs to be to get the twin mandate right from first rules, if reform of the Fed’s financial coverage framework is to achieve success in 2019 below Powell.

A fast have a look at the most recent Fed “forecasts” (see above) will present how unemployment and inflation knowledge are literally getting used as targets while being offered as forecasts. A fast have a look at the latest speech from John Williams will present how they’re getting used as indicators.

(Source: Seeking Alpha)

The Fed’s anti-inflation bias was earlier recognized within the May report on this sequence, as a consequence of the Fed’s institutional failure to totally embrace its inflation goal as a symmetrical one. Fed audio system like John Williams talked the discuss of inflation overshooting, however they’ve by no means sincerely walked the discuss. At that point it was additionally famous that the Fed’s home inertial financial optimism would run into the miserable world headwinds earlier than it had reached its goal for the impartial fee. This bias stays sturdy based mostly on the Chairman’s efficiency on the newest FOMC. This bias was considered as inappropriate again then though oil was on a tear and dragging inflation upwards with it. If it was inappropriate again in May and July, it’s egregious now on condition that oil is falling and the worldwide economic system is imploding.

New York Fed President John Williams was the first-responder to the carnage created by Chairman Powell’s one hand. As the Fed’s actual market interface, the New York Fed has this unlucky default place. Trying to not solid aspersions on Chairman Powell’s skill, Williams did his finest (and failed) to slender the disconnect between Mr Market’s expectations curve and the Fed’s.

How it will play out in follow is by the Fed instantly altering its “target” (see above “forecast”) for GDP falling massively from 3% in 2018 to an “indicator” of 2.3% in some unspecified time in the future 2019. Said “indicator” will then be defined as being beneath “target”, thus permitting the Fed to pause and even take into account easing. A new larger “target” will then be offered to justify the brand new pause/ease coverage. For this little mixing of metaphors to achieve success, the Fed requires inflation to stay subdued. Right now this seems to be a great guess, because the Fed has been doing its finest to crush it of late.

Mr Market has nonetheless already begun discounting this large actual slowdown within the economic system into asset costs. Some nonchalant steering from Fed audio system in 2019 will then attempt to make the transition from “target” to “indicator” as imperceptible as doable. The Fed hopes that by then, Mr Market might be so busy discounting the pause and potential ease that he is not going to name it out for its noble lies.

Williams made the error of failing to notice that since Mr Market is ahead trying and the Fed at the moment stays historic knowledge dependent, this divergence of opinion and its detrimental penalties for the true economic system can persist till the Fed turns into ahead trying. The two observers will thus start the New Year persevering with to learn and act from completely different pages. Also talking post-FOMC assembly, Cleveland Fed President Loretta Mester confirmed this web page divergence with her explanation that “perhaps they (markets) are inferring something about the economy, we are not seeing in the data.”

Williams has additionally failed to notice that the detrimental halo impact from Chairman Powell’s mishandling of the final FOMC communication now touches and frames his personal steering. In order to vary perceptions of himself after which lengthen this optimistic halo to vary perceptions of Chairman Powell, it can take greater than Williams’ newest ritual admission of guilt. Going ahead, it is going to be attention-grabbing to see if and the way Fed audio system distance themselves from after which reframe Powell, ought to he keep his present inertia as the information vitiates towards his normalize on auto-pilot viewpoint.

(Source: Seeking Alpha)

Of extra curiosity than Williams and Mester’s putting of the fig leaf over Chairman Powell’s embarrassing publicity on the final FOMC was the Kansas City Fed’s inadvertent publicity of this identical object. A previous report has famous that it will be a big failing of Chairman Powell’s new monetary stability danger administration framework have been he to disregard the enter from what has been referred to as the Regional Fed. Kansas City Fed President Esther George will rotate into the voting chair in 2019, so this rising structural dilemma might be highlighted.

Said Regional Fed has been considerably extra Dovish than the Washington Fed of late, with the Beige Book now ostensibly calling for a pause within the fee hike course of. It now transpires that the Kansas City Regional Fed was against the most recent fee hike. It might be attention-grabbing to see if its President and famend Hawk Esther George goes with the information and enter from her personal group or if she follows the Washington Fed line sooner or later. The regional context for the warning on the Kansas Fed is well understood. With an economic system basically pushed by power and agriculture in its footprint, the worldwide headwinds are felt acutely there. Risks at the moment are finely balanced on this footprint, so the Kansas City Regional Fed wish to take a pause to evaluate the harm.

If President Trump has famous the “forecast” sudden deceleration in GDP in 2019, he’ll tactically blame the Fed for this, thereby forcing them to pause and even to think about easing. All the President’s Tweets recommend that blame is being conveniently hooked up to the Fed as he controls the narrative. If and when the Fed pauses, he’ll keep this management with an “I told you so” Tweet.

(Source: St Louis Fed)

As St Louis Fed President James Bullard rotates into the voting seat in 2019, it’s instructive to know what his analysis group have been offering him with intelligence on. The inverted yield curve seems to be one thing that he’s going to make use of with nice impact in 2019. A latest Blog report informs us that the inverted yield curve acts as an financial headwind by the banking sector for the next causes:

(Source: St Louis Fed)

- An inversion might trigger loans to be much less worthwhile relative to the financial institution’s value of funds.

- An inversion would trigger their banks to be much less danger tolerant.

- An inversion could sign a much less favorable or extra unsure financial outlook.

A cursory have a look at Japan will affirm these findings. If the US banking sector is due to this fact pulling its horns in, as a consequence of the inverted yield curve, the knowledge of placing it below additional stress by persevering with to withdraw disaster stimulus reserves is questionable.

The knowledge of tightening capital market liquidity by elevating rates of interest and reducing the Fed’s stability sheet again can be questionable below the identical circumstances. Banks will merely go lengthy Treasuries (as they’ve carried out) as rates of interest rise, as a result of they provide a extra engaging danger adjusted reward than riskier lending.

Where the BOJ scores extra extremely than the Fed is that it has held onto its JGB’s when the curve was inverting, thereby stopping the banks from stockpiling them. Unfortunately for the BOJ, crowding the banks out of the JGB market has not compelled them into the industrial lending market as a result of the yield curve is just too flat. The BOJ has thus not too long ago adopted Yield Curve Control with a view to stimulate financial institution lending out alongside the yield curve. The Fed ought to notice the BOJ’s travails intently, because the inverted US yield curve is creating an analogous drawback though US rates of interest are optimistic.

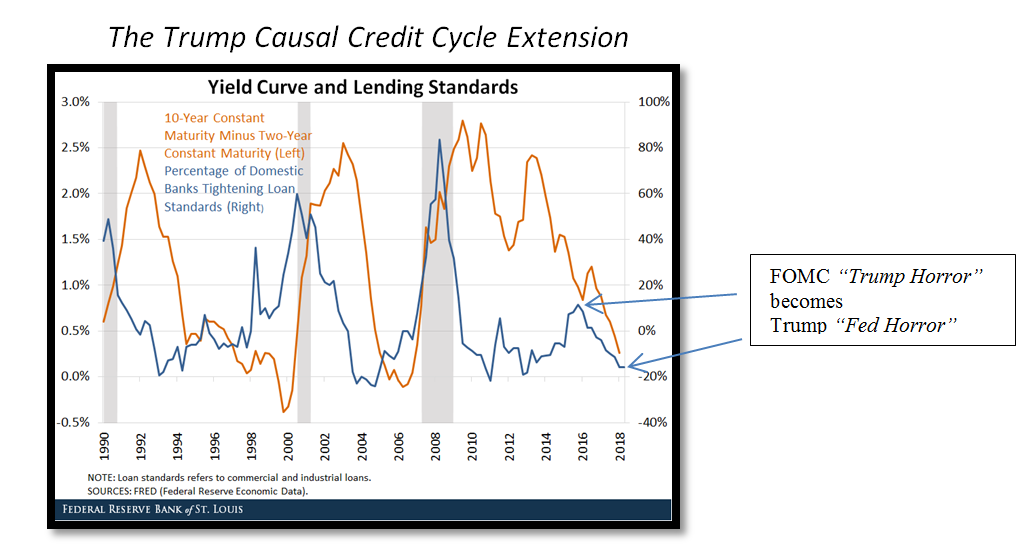

The St Louis Fed researchers have discovered and illustrated graphically that historically a curve inversion triggers banks to tighten lending requirements. This then causally creates recession situations in extremis. They have additionally proven that President Trump’s insurance policies to collocate a fiscal stimulus with an easing of banking requirements have extended the credit score cycle growth which had been historically rolling over simply earlier than he was elected. President Trump triggered an extension of the credit score and enterprise cycle. He additionally triggered some critical partisan response from the Fed. The Fed’s zealous persevering with to achieve for the brand new regular fee, in horror at Trump’s insurance policies, can be clearly evident within the St Louis Fed’s epigraphic findings.

This brings us to an approaching tipping level quickly at which the banks aggressively tighten credit score once more. The latest mass exodus from leveraged loans and normal riskoff sentiment appear to be very clear alerts that this level has simply been handed. Anecdotally, this tipping level flips the Fed’s horror at him to President Trump’s horror at it. In its response to President Trump, the Fed has acted politically though it may well legally declare that its reactions are in step with its twin mandate interpretation.

Bullard might be anticipated to advocate not just for a pause in rate of interest hikes but in addition a request for the Fed to revisit the method of stability sheet shrinkage and reserve discount.

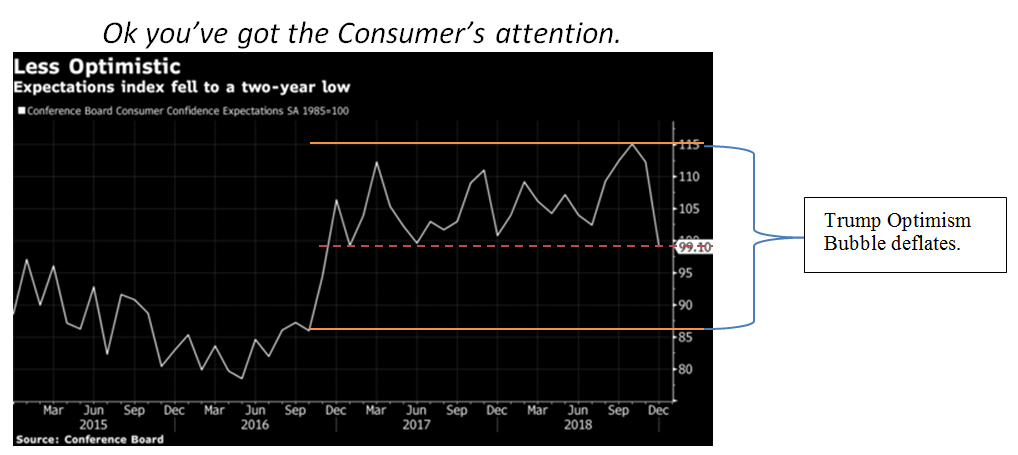

(Source: Bloomberg)

The newest consumer expectations knowledge means that the American shopper has lastly started to pay attention to what’s occurring globally and what’s occurring at residence politically and economically. An fairness market correction at all times heightens this consciousness. The fall in shopper expectations might be seen because the erosion of the boldness that President Trump had created when he was elected. Since it’s (or was) the buyer who’s (was) holding the economic system up, the financial slowdown foretold by Mr Market has now been foretold by the buyer’s expectations.

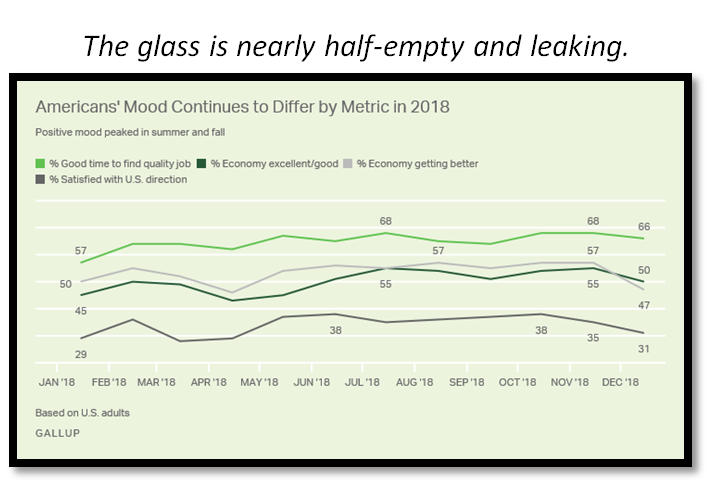

(Source: Gallup)

Underlining the sliding shopper confidence knowledge is the most recent Gallup mood poll. The temper of Americans is in transition from assured to one thing much less so, particularly in relation to the economic system.

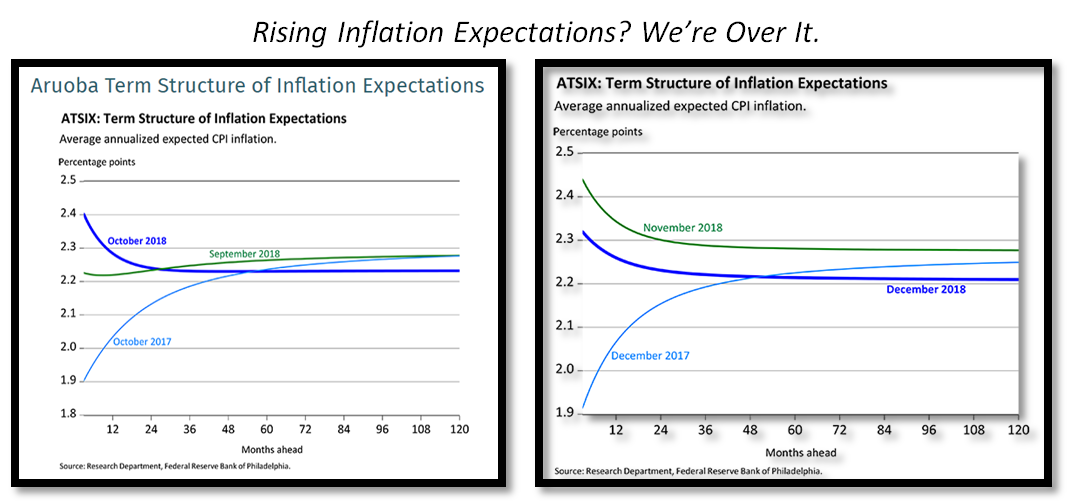

(Source: Philadelphia Fed)

Lingering worries over rising inflation expectations have abated since November if the Philly Fed’s Term Structure of Inflation Expectations might be trusted.

The Fed can pause, however it should additionally take notice that it’s now behind the curve after the most recent fee hike and can mechanically fall additional behind because it shrinks its stability sheet and cuts financial institution reserves on auto-pilot.

(Source: Seeking Alpha)

As the President suggested, higher to “take the victory” than be blamed for the slowdown.

Switching from auto-pilot to handbook would appear to be the correct factor to do, assuming that Chairman Powell has the boldness to take the controls.

Disclosure: I/we’ve got no positions in any shares talked about, and no plans to provoke any positions inside the subsequent 72 hours. I wrote this text myself, and it expresses my very own opinions. I’m not receiving compensation for it (aside from from Seeking Alpha). I’ve no enterprise relationship with any firm whose stock is talked about on this article.

[ad_2]