Staar Surgical’s $28 Buyout Premium—Is Alcon Getting A Bargain?

Staar Surgical (NASDAQ:STAA) has moved into the spotlight following the announcement of a proposed all-cash merger with Alcon at $28 per share, representing a 51% premium to its pre-deal stock price. The company, best known for its EVO implantable Collamer lenses (ICLs), has faced a difficult operating environment marked by a steep decline in China revenues, restructuring costs, and tariff headwinds. The deal, backed by Staar’s second-largest shareholder Soleus Capital, is being framed as a way to provide shareholders with certainty and liquidity at a time when the standalone outlook is clouded by volatility. For Alcon, however, the appeal goes deeper than just opportunistic timing. We believe that there are some important strategic drivers that could explain why Alcon sees value in pursuing this small-cap ophthalmic player:

Strengthening Position In Refractive Vision Correction

One of the most compelling reasons for Alcon’s interest in acquiring Staar Surgical lies in the structural growth of the refractive vision correction market and Staar’s leadership in the premium ICL segment. While global procedure volumes for traditional laser vision correction such as LASIK and PRK are declining, demand for lens-based options is increasing, particularly in Asia-Pacific markets like Japan, China, and South Korea. Staar’s proprietary EVO ICL technology is positioned as an additive, reversible solution that avoids permanent changes to the cornea and has demonstrated high patient satisfaction rates above 99%. This differentiation has allowed Staar to build strong surgeon adoption, especially in markets where consumer awareness of non-laser alternatives is higher. For Alcon, which already has a substantial presence in cataract and intraocular lenses, acquiring Staar would complement its existing portfolio and allow it to expand into a fast-growing niche that aligns with shifting patient preferences. The combination would enable Alcon to leverage its global distribution, training, and surgeon education infrastructure to accelerate EVO adoption beyond Asia into Western markets where penetration remains relatively low. Moreover, the broader secular tailwind of rising myopia prevalence—affecting nearly 2.7 billion people globally, with 1.1 billion in Staar’s core 21–45 age group—provides a long-term growth pool that Alcon could more fully tap with Staar’s proprietary technology. The strategic fit is clear: Alcon gains a differentiated growth vector at a time when ophthalmology is converging toward lens-based solutions, while Staar gains the scale and marketing muscle necessary to expand its total addressable market.

Mitigating Geopolitical & Manufacturing Risk Through Scale

Another major factor motivating Staar Surgical’s potential merger is the opportunity for Alcon to help stabilize and diversify its production and supply chain, which has been strained by tariffs, channel inventory challenges, and geographic concentration. In 2025, retaliatory tariffs imposed by China forced Staar to deploy consignment inventory to mitigate near-term risk while ramping up new Swiss-based manufacturing capacity. Although management has positioned this as a viable long-term solution, the transition has resulted in higher per-unit costs, depressed gross margins, and significant restructuring expenses. For a small-cap firm like Staar, navigating such volatility while simultaneously funding global growth is a challenging balancing act. Alcon, by contrast, has the financial resources, regulatory expertise, and diversified global manufacturing footprint to absorb these shocks more effectively. Integration into Alcon’s broader supply chain would provide cost synergies through procurement leverage, manufacturing efficiencies, and logistics optimization. It would also reduce dependence on any single facility or region, lowering the risks of geopolitical tariffs or disruptions to distribution in key markets like China. Furthermore, Alcon’s ability to scale up production more quickly could address one of Staar’s core bottlenecks: ensuring consistent supply at a time of rising procedure demand. By combining forces, Alcon could unlock operating leverage that Staar cannot achieve alone, potentially restoring gross margins back toward historical 75–80% levels sooner. The result would be not only cost stabilization but also enhanced strategic resilience, a factor increasingly valued in medical device supply chains.

Enhancing Global Commercial Reach & Market Access

A third rationale for Staar Surgical’s potential merger is the chance to expand the commercial reach of EVO ICL by leveraging Alcon’s established distribution network and payer relationships. Staar’s Q1 2025 results highlighted a stark contrast: while China revenues collapsed to just $389,000 due to distributor destocking, sales in other markets grew 9% year-over-year, driven by strength in Japan, South Korea, India, and Europe. This illustrates both the demand potential and the executional limits of Staar as a standalone small-cap. Marketing EVO ICL requires intensive physician training, patient education, and regulatory navigation across multiple geographies—areas where Alcon already has entrenched capabilities. By embedding EVO within Alcon’s sales channels, particularly in underpenetrated Western markets like the United States, Canada, and Europe, the adoption curve could steepen significantly. Alcon also has stronger payer relationships and reimbursement negotiation expertise, which could lower patient cost barriers and improve accessibility. Beyond refractive correction, Alcon could integrate EVO into bundled ophthalmic offerings, cross-selling alongside cataract lenses or surgical systems to enhance value per customer. This bundling strategy is common in medtech and could create meaningful revenue synergies by positioning Alcon as a full-spectrum vision correction provider. Additionally, Alcon’s scale in digital marketing and direct-to-consumer campaigns could raise awareness of EVO as an alternative to glasses and contacts, addressing one of the major adoption hurdles identified by Staar management. With 2.2 billion people worldwide eligible for lens-based correction but not yet seeking surgical solutions, awareness and distribution are key barriers that Alcon is well placed to overcome.

Leveraging Financial Scale To Unlock Innovation & Pipeline Expansion

The fourth driver of potential interest is the innovation runway that Staar brings, which could be better capitalized under Alcon’s ownership. Staar has consistently highlighted its proprietary biocompatible polymer, which forms the backbone of its ICL technology and offers opportunities for expansion into other ophthalmic therapeutic areas. The upcoming EVO+ (V5) lens, set for approval in China later in 2025, exemplifies this potential by offering larger optical zones and improved patient outcomes. However, as a small-cap company with limited cash flow generation—Staar posted a Q1 adjusted EBITDA loss of $26.4 million—funding both operational turnaround and new R&D initiatives simultaneously stretches resources thin. Alcon, with its substantially stronger balance sheet, could accelerate product development and clinical trials, bringing new iterations of EVO and adjacent technologies to market faster. This financial backing would also mitigate the cyclical nature of Staar’s current spending patterns, which are heavily influenced by tariff mitigation and restructuring costs. Importantly, integration with Alcon’s innovation ecosystem could create synergies in preclinical testing, regulatory filings, and physician training, expediting time-to-market for next-generation lenses. For Alcon, acquiring Staar would not only secure an immediate growth asset but also a platform for long-term innovation in refractive correction, further entrenching its leadership in ophthalmology. This dual benefit—harvesting near-term synergies while expanding optionality in lens-based vision correction—makes Staar an attractive pipeline-enhancing acquisition.

Final Thoughts

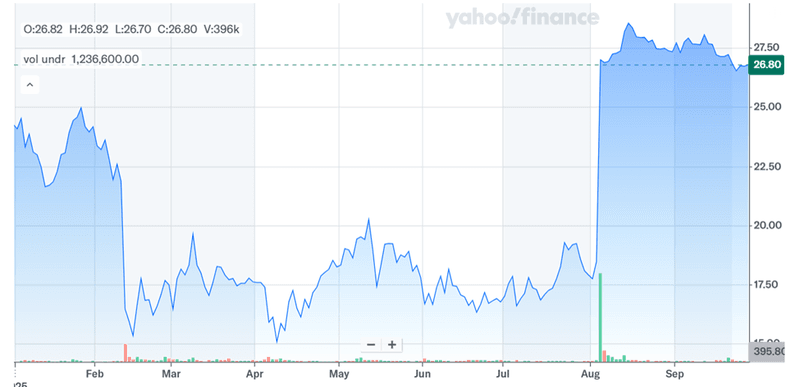

Source: Yahoo Finance

Staar Surgical’s stock price has surged close to the proposed $28 per share merger price leaving very little room for M&A arbitrageurs. From a valuation standpoint, Staar trades at elevated multiples compared to broader medtech peers, with LTM Price-to-Sales at 5.89x and EV/Sales at 5.23x, while profitability multiples remain volatile, reflecting operating losses and margin compression. These high valuation levels relative to financial performance could be justified in a strategic acquisition where synergies and growth optionality are more highly valued. Ultimately, we believe that Staar represents both opportunity and risk: an innovative small-cap with long-term growth potential, but one that currently requires scale and operational stability to unlock its full market opportunity.